EU CONSUMER CYCLICALS: Consumer & Transport: Week in Review

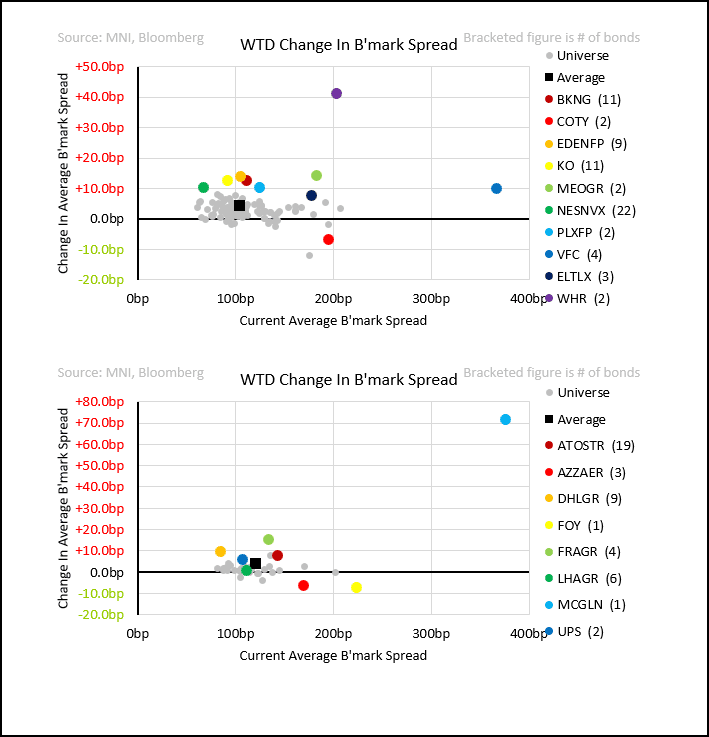

We are not sure we’ve ever seen Coca-Cola (KO) move more than VFC on risk-off - but that’s what played out this week. Technicals likely behind it: two large high-grade prints (Visa, Alphabet) soaking up demand. But it leaves questionable RV: can 16y Coca-Cola Europacific (the bottler) really trade -10bps inside partial owner Coca-Cola? Elsewhere, Whirlpool’s +40bp move on a junking is another friendly reminder that near-term ratings catalysts can matter more than earnings trajectory. Earnings slow down next week with Elis, Pandora, Flutter and IHG of note. But we still expect volatility from ratings, supply, and Mobico.

- Mobico reports FY results with the normal slew of one-off adjustments that leave earnings lacklustre and us still seeing only rating downside (at Fitch). Senior bonds finally reacted, as equities showed no signs of reversing a >40% drawdown. We flagged later in the week that the potential for an Event of Default is real – we see conditions met under the cessation of business clause, which could force par redemption on the £28s and €31s. Mobico, however, does not have enough cash to cover both and terms of the undrawn revolver (e.g. cross-default) are unclear.

- Kraft Heinz: sales still weak, but guidance calls for improvement. Ratings headroom may buy time, but we continue to see US-heavy F&B as uninteresting vs. broader staples.

- LVMH pays an 8bp NIC and continues the trend of steepening its curve on supply. In line with our view, only the 4y tightened while the 7y weakened further. It trades well wide of fundamentals – we see this ‘Arnault discount’ as warranted.

- Couche-Tard finally signs an NDA with 7&i, gaining access to financials. It may have agreed to tone down public pressure in return.

- Flutter closes on Snai. There is some beta to earnings next week given it has begun equity payouts and was holding leverage outside target. We are expecting supply, currency uncertain.

- Lufthansa opened airline earnings hiding continuing weakness on costs with positive macro backdrop. It says cost pressures will ease in 2H.

- Finnair faces more industrial action. It says some agreements have been struck, but impact on earnings still worsening. Risk skewed negative until fully resolved.

- DSV 1Q results are fine as it moves into the Schenker integration period. Management hints at more refi supply, but likely size is not of concern. Comments on balance sheet governance remain positive.

- Woolworths: earnings fine but more importantly the political catalyst looks favourable ahead of the weekend election. We again see value on the 28s and some on the new 32s.

- Primary (NIC in brackets): Carrefour 4yr (+4), LVMH 3.9yr (+8), 6.9yr (+8), Tesco 7y (0), Aeroporti di Roma 7.1y (+3)

- Whirlpool: Both S&P and Moody’s cut to junk. Moody’s holds a negative outlook. We’ve flagged concerns for a while.

- Altria: Moody’s lifts negative outlook and stabilises ratings.

- AB-InBev: Moody’s follows S&P and moves to positive outlook.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Senator McConnell To Vote Yes On Democratic Tariff Resolution - NBC

Senator Tim Kaine (D-VT) said that former Senate Republican Leader Mitch McConnell (R-KY) indicated that he will vote yes on a Democratic resolution that would "undo" President Donald Trump's tariffs on Canada by challenging the national security justification for their imposition, according to NBC News' Frank Thorpe on X. The resolution is seen as a message exercise as House Speaker Mike Johnson (R-LA) would kill the bill in the House, should it pass the Senate.

- For the resolution to pass, Democrats will need at least four Republican votes. Senator Rand Paul (R-KY) and moderate Senators Susan Collins (R-ME) and Thom Tillis (R-NC) have indicated they will vote yes.

- The vote, which will come later today after being punted from yesterday's schedule by Senator Corey Booker's (D-NJ) marathon speech, will put Republicans representing farm and manufacturing states in a challenging position, with polling suggesting that voters are sceptical of Trump's tariffs.

- Republican Senators may feel slightly more emboldened to oppose Trump's agenda after elections in Florida and Wisconsin yesterday provided warning signs that Independents and moderate Republicans are unconvinced by the early period of Trump's administration and the influence of advisor Elon Musk.

- Recognising that a significant Senate Republican rebellion could undermine his 'Liberation Day' announcement, Trump has issued two lengthy statements on Truth Social directly calling on Republicans to oppose the resolution.

TARIFFS: Deutsche Bank Expect Any Relief Rally Will be Short-Lived for Equities

- On today's market outcomes from the tariffs announcement, Deutsche Bank write that it is hard to see an outcome where we see material and sustained upside for equities.

- They write that even if tariffs are perceived to be on the lenient side, there remains a high degree of uncertainty over how various counties will respond and whether Trump will be more aggressive over time.

- Deutsche Bank see the broader USD reaction as likely to be led by equities and therefore see greater downside risks for the USD, led by the JPY and gold.

SWAPS: Long End ASWs Weaker Alongside Outright Bunds

Long end ASWs a little weaker on the day alongside the sell off in outright bonds detailed recently.

- Bund & Buxl ASWs have failed to push meaningfully above levels that prevailed ahead of the “whatever it takes” German fiscal moment, while Bund yields haven’t broken below the lows witnessed since the German fiscal loosening was table, pointing to new ranges being established as Germany moves to a new fiscal framework.