EM LATAM CREDIT: CFE Fibra E: Mandate Investor Calls

(FCFE: NR/BBB/BBB-)

“MANDATE: CFE Fibra E to Hold FI Investor Calls Monday” – Bbg

IPTs 7Y WAL: N/A

FV 7Y WAL: 6 - 6.25% Area

• The funding vehicle for Mexico government-owned vertically integrated electric utility CFE’s transmission business mandated investor calls ahead of the potential issuance of USD benchmark-sized 144a/REGS senior unsecured 15-year final, 7.2-year WAL amortizing notes.

• The vehicle is a Fibra (Mexican REIT-type structure) that is required to pay out 95% of fiscal income. CFE Fibra E is 75% owned by private investors, 25% owned by CFE Capital, which in turn is wholly owned by CFE.

• The trust owns rights to receive from the federal government electricity market regulator CENACE (through another trust called the PT (Promoted Trust) 6.78% of revenues, rising to 9.4% after this issuance, that has been generated by the transmission system, of which CFE has a monopolistic business position.

• As the vehicle is dependent on CFE’s transmission business and a Mexico government agency, we see these notes as a spread to CFE (CFELEC; Baa2/BBB/BBB-) debt. The trust currently doesn’t have operating assets and merely has the right to receive revenues from the transmission system.

• The convoluted structure and exposure to political and regulatory risk demands a premium as well as the risk of increasing leverage down the road as CFE expects to invest USD7+bn over the next 2-3 years to expand the transmission grid.

• CFELEC has 2031, 33 and 35 notes so we interpolate for a 7-year T+195bp, or 5.7% YTM. For another comp that caps in our view the upper end of the estimated premium for CFE Fibra E, Tierra Mojada (TIEMOD; Baa3/BBB/BBB-) 5.75% 2040 amortizer, a Mexico project deal, has a 15-year final, 7.7Y WAL at 6.35%, G-spread 252bp.

• TIEMOD has a similar cash flow structure with dependence on CFE as an offtake but with the difference that it is a senior secured infrastructure bond backed by one combined cycle thermal power plant. It also has more electricity market price risk as compared to CFE Fibra E which collects transmission fees from a monopoly provider.

• We estimate fair value for CFE Fibra E as somewhere in the middle of CFELEC and TIEMOD.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Limited Trade To Open Week, With Sonia Upside Faded Pre-Labour Data

Monday's Europe bond/rate options flow included:

- SFIH6 96.70 calls 3.5K given at 5

US OUTLOOK/OPINION: Analyst Expectations For Sequential Drivers In July CPI

Core CPI sequential drivers in July are expected to come from used cars increasing modestly after a weak run plus travel-related services with lodging away from home pausing after declining and airfares increasing after broadly pausing.

- Lodging away from home (+ve): Seen broadly unchanged on the month after a heavy -2.9% M/M in June that subtracted -0.05pps from core CPI.

- Used cars (+ve): There’s a reasonable range of estimates for used car prices in July, from -0.5% to +0.7% but they all are stronger than the -0.7 M/M seen in June. The average estimate is 0.24% M/M after four months averaging -0.6% M/M.

- Airfares* (+ve): Seen rising 1.5% M/M after -0.1% in June following a period of prolonged, large declines with an average -3.7% M/M through Feb-May. The range of views of -0.4% to 2.5% is one of the narrower in recent months.

- Apparel (neutral to small +ve): Median of 0.5%/average 0.44% having accelerated to 0.43% M/M in June from a surprisingly soft -0.4% M/M in May.

- Vehicle insurance* (neutral to small +ve): Once again only three estimates this month with a decent range of -0.1% to 0.6% M/M. The average of 0.2% M/M would be a slight acceleration from the 0.1% in June but it’s a category that can swing from month to month with a sizeable 3.5% weight in core CPI.

- Rents (neutral): Owners’ equivalent rent (OER) seen dipping to an average 0.28% (range 0.25-0.30) after 0.30% in June, but with primary rents firming to an average 0.26% (range 0.22-0.34) after 0.23%.

- Non-core: Food (small -ve): Food price inflation is seen easing to 0.25% M/M in July after 0.33% M/M. Food away from home has continued a robust run recently, with 0.40% M/M in June and a 1H25 average of 0.36% (feeding into core PCE but not CPI). Food at home meanwhile has seen two months averaging 0.27%.

- Energy (-ve): Energy prices are seen falling circa -0.6% M/M after a 0.95% increase in May, driven by a more than 2% M/M decline in seasonally adjusted gasoline prices.

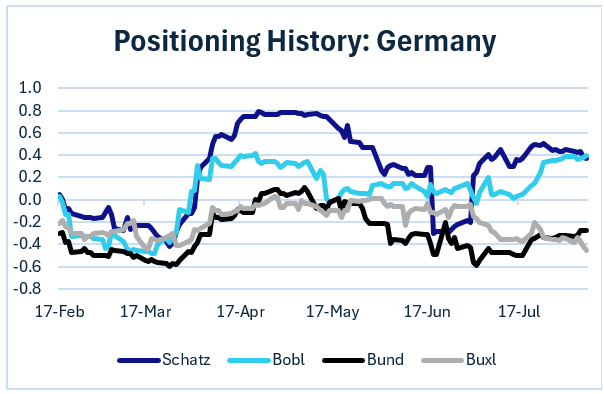

BONDS: Europe Pi: German Positioning Mixed (1/2)

From our latest Europe Pi futures positioning update (PDF):

- German contracts' structural positioning has been relatively steady since late July, with some subtle shifts. Schatz remains in "long", though has failed to pierce "very long" territory. Bobl has shifted into long territory alongside.

- Bund and Buxl remail short as with the last update.

- Shorts were set across 3 of 4 contracts last week, with the exception being Buxl (longs reduced).