EM LATAM CREDIT: CFE: $ 8Y, 12Y WAL Launch

(CFELEC; Baa2neg/BBB/BBB-) Launch IPTs FV 8-Year $1bn 200bp T+240bp Area 185bp 12-Year $500mn 230b...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

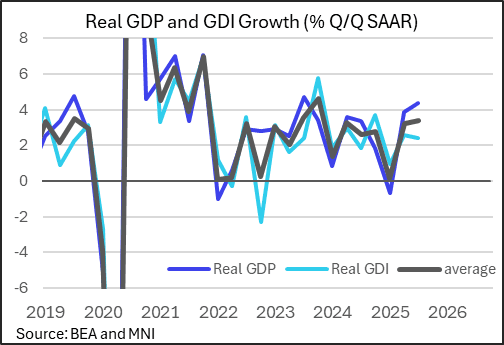

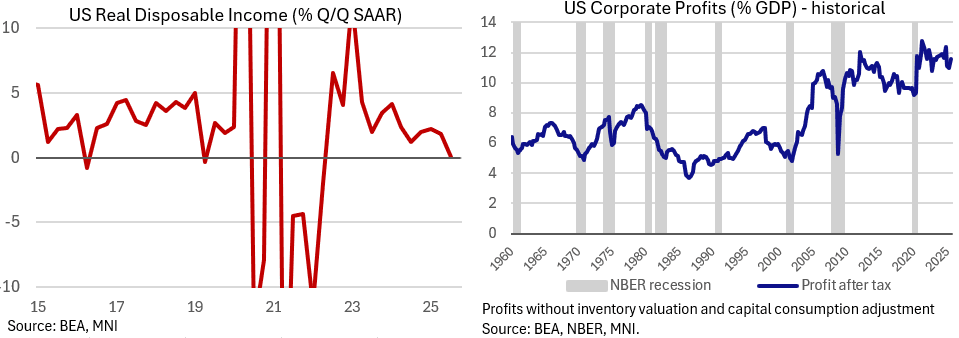

US DATA: Corporate Profits Buoyant, But Disposable Income Slowdown A Concern

The 1st reading of Q3 GDP also included an initial read of real Gross Domestic Income (GDI), which posted an estimated 2.4% Q/Q SAAR growth rate. That's substantially lower than the GDP growth rate of 4.3% and slower than the 2.6% printed in Q2. We took note of relatively soft dynamics for personal income which stood in contrast to robust corporate profits.

- This was the 2nd consecutive quarter GDI has printed well under GDP; the average of the two measures nonetheless ticked up to 3.4% (3.2% prior) for the best reading since Q3 2023. It also makes for the biggest "statistical discrepancy" (GDP - GDI as % of GDP) at 1.2% since Q3 2024, but since the figures should theoretically be equal the differential tends to narrow over subsequent revisions.

- Corporate profits (with inventory valuation and capital consumption adjustments) led the quarterly GDI gain, rising $166B (after a net negative 1st half, -$41.0). The breakdown of nonfinancial businesses ($100.4B)' profits by sector wasn't made available in this print, but overall they represented 2/3 of domestic industries' profits.

- After-tax corporate profits remain very elevated vs the longer-run historic series, at over 11% of GDP.

- We took note of relative weakness in personal income, however, with real disposable income growth basically flat in Q3 for the slowest growth since Q2 2022; the Y/Y rate (1.5%) was the weakest since Q4 2023.

- This came as nominal disposable income growth came in at just 2.8%, eroded by inflation; the savings rate fell to the lowest (4.2%) since Q4 2022.

- All of these series tend to get revised heavily in future quarters so we wouldn't read too much into it, but that marks the 2nd consecutive quarter of noticeable slowdown in real disposable income, amid a clear cooling in the labor market as a whole.

- It doesn't suggest particularly firm underpinnings to PCE spending, which is providing the single biggest pillar to growth (2.4pp of the 4.3% posted in Q3).

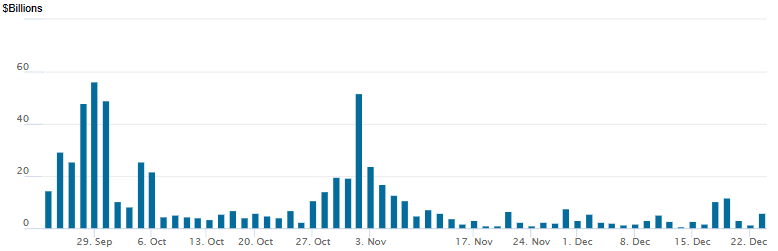

US: FED Reverse Repo Operation

RRP usage rebounds to $5.893B with 14 counterparties this afternoon vs. Monday's $1.523B. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

GBPUSD TECHS: Fresh Cycle High

- RES 4: 1.3661 High Sep 18

- RES 3: 1.3557 76.4% retracement of the Sep 17 - Nov 4 bear leg

- RES 2: 1.3527 High Oct 1

- RES 1: 1.3519 High Dec 23

- PRICE: 1.3477 @ 15:39 GMT Dec 23

- SUP 1: 1.3371 Low Dec 22

- SUP 2: 1.3306 50-day EMA

- SUP 3: 1.3180 Low Dec 2

- SUP 4: 1.3125 Low Nov 26

The trend condition in GBPUSD remains bullish and this week’s strong start reinforces current conditions. The pair has traded to a fresh short-term cycle high, confirming a resumption of the uptrend that started early November. Note that moving average studies have recently crossed and are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.3527, the Oct 1 high. Initial firm support is 1.3306, the 50-day EMA.