JGBS: Cash Bonds Slightly Mixed After Yesterday's Holiday

In Tokyo morning trade, JGB futures are stronger, +4 compared to settlement levels, after yesterday’s holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today’s Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.7bp higher (40-year). The benchmark 10-year yield is 0.8bp lower at 1.646% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - See Some Demand As Risk Reverses Higher

US equities exploded higher in the Friday N/Y session as the market reacted to what it interpreted to be a very dovish speech. This morning US futures opened a little lower, ESU5 -0.10%, NQU5 -0.12%. The AUD was helped by this return in risk appetite and continued to pull back from its lows seen in the crosses last week.

- EUR/AUD - Friday night range 1.8030 - 1.8082, Asia is currently trading around 1.8060. This area just above 1.8100 has seen decent supply cap it the last few months, a sustained move above 1.8100 cis needed to see the move extend higher. With risk sentiment improving we could see this pair potentially drift lower if new highs can't be made.

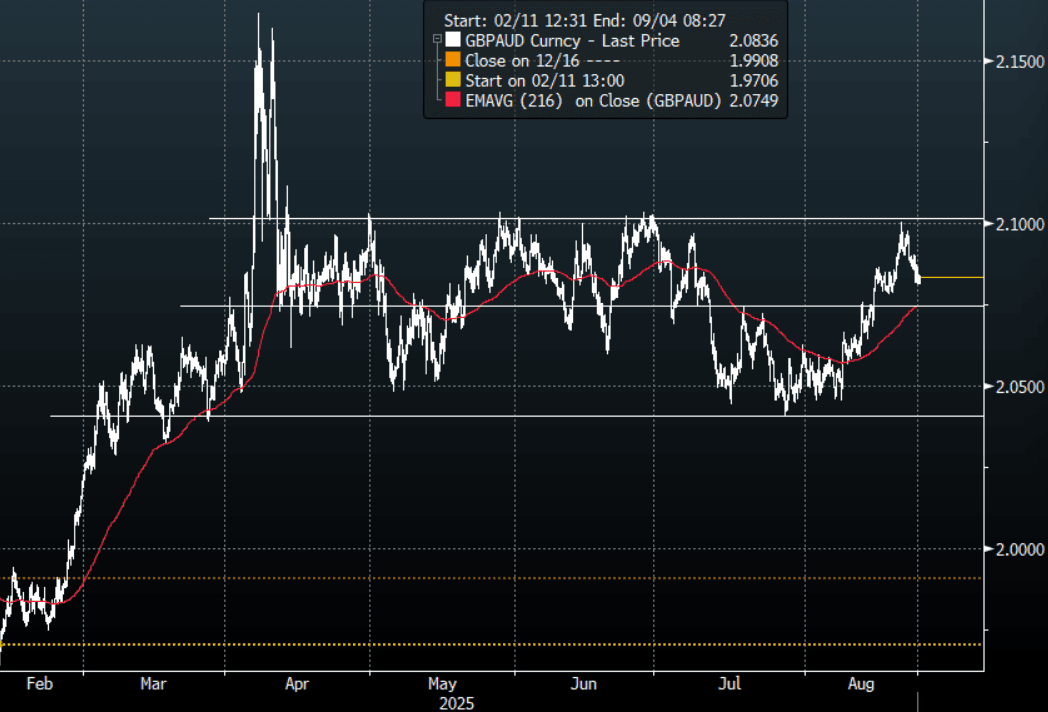

- GBP/AUD - Friday night range 2.0815 - 2.0903, Asia is trading around 2.0835. The pair failed back toward the 2.1000 area again where supply returned. Having reached the top of the range expect this 2.10/11 area to cap for now especially if risk is able to start moving higher again. First support is back towards the 2.0700 area.

- AUD/JPY - Friday night range 95.15 - 95.59, Asia is trading around 95.45. The pair found some demand around 94.50 and has bounced overnight, sellers should be around back towards 96.00 initially. This pair’s direction will be determined by the market's ability to follow on with this risk-on move or not.

- AUD/NZD - Friday night range 1.1052 - 1.1069, the cross is dealing in Asia around 1.1055. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

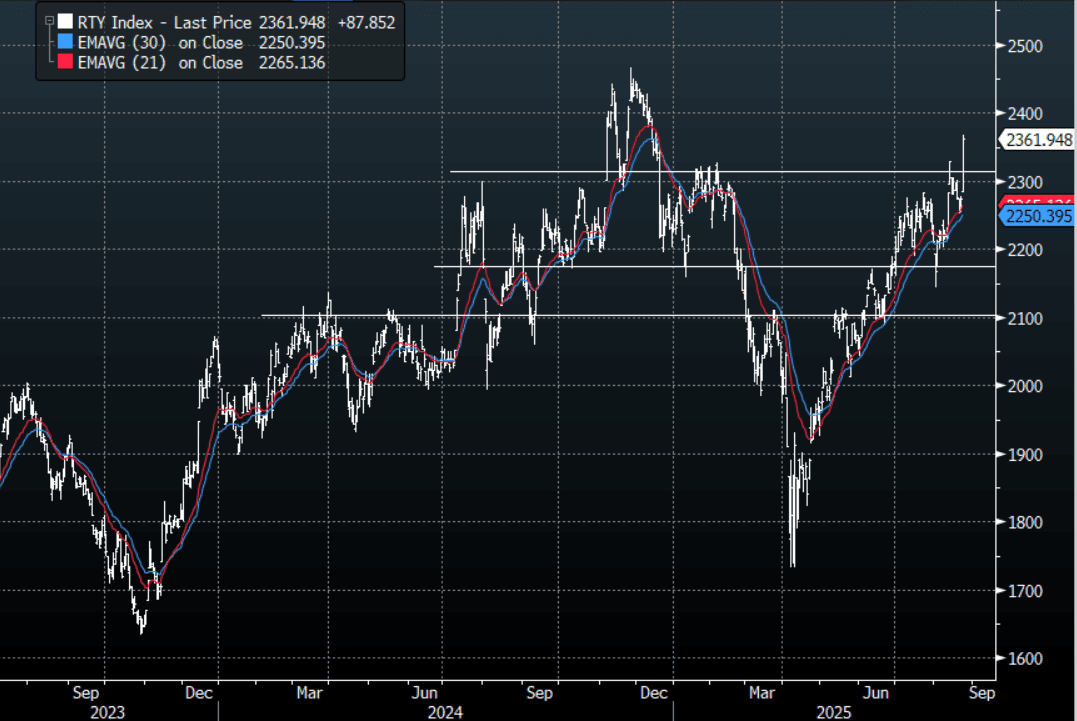

US STOCKS: Russell Explodes Through Resistance Just Above 2300

The Russell 2000 Friday night range was 2285.178 - 2366.598 closing +3.86%. The Russell 2000 has burst higher breaking back above the stubborn resistance just above 2300. I have subsequently read some varying interpretations of Powell's speech with some questioning if it really was that dovish ? So it will be interesting to watch the price action the first couple of days of this week to see if the Friday move can be firstly maintained and then potentially built on. What is clear is the huge shorts held by hedge funds in the Russell would be very uncomfortable with how things played out.

- Bloomberg - “Russell 2000 Surges to This Year’s High on Rate-Cut Prospects: Jerome Powell’s words are music to small-cap investors’ ears as rate cuts would bring huge relief to the Russell 2000, which houses a lot of struggling borrowers.”

- RenMac on X: “This is about September. If you get solid data, you’ll get a hawkish cut in September. If you get bad data, you’ll get a dovish cut. That’s how to think about this. Through the lens of an insurance cut being green lit in September. Importantly, Powell is accepting the Waller framing of the world. We had a shadow chair already. Time to give him the job.”

- Daily Chartbook on X: "EPS expectations for small caps are already extremely bullish, with earnings expected to grow by more than 80% over the next two years. Should interest rate relief be delayed, small caps will likely underperform." -@Daniel_VonAhlen @andrea_cicione @TS_Lombard.

Fig 1: Russell 2000 Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: RBA Minutes And July CPI This Week

In a light week, the focus will be on Wednesday’s July CPI data and Tuesday’s publication of the August RBA minutes. The Board cut rates 25bp this month. They will likely be monitored for further details on its concerns regarding lacklustre productivity growth, its view on the labour market and any discussion of the risks around its inflation outlook. The vote to ease was unanimous.

- July headline inflation is forecast to rise back to 2.3% y/y after falling to 1.9%. This would be the highest since April. The series continues to be impacted in both directions by state and federal electricity rebates. The trimmed mean moderated to 2.1% in June. The July data won’t include updates on most of the services components.

- The RBA’s attention remains on the quarterly data as the monthly CPI is still not complete with the first full release scheduled for the October release on November 26.

- The July Westpac leading index is released on Wednesday. Previous months’ prints are signalling that growth should remain sluggish but return to around trend by year end.

- Components that feed into Q2 GDP released on September 3 will be released with construction work done on Wednesday. It is forecast to rise 1.0% q/q after a flat Q1. Private capex is on Thursday and is expected to rise 0.8% q/q after falling 0.1%.

- Friday sees the RBA’s private credit data for July which is projected to rise 0.6% m/m again.