CANADA: Carney Seen Running CAD75B Deficits, Record Outside Covid

- Economists surveyed by MNI say deficit in Canada budget due Tues after 4pm EST will be CAD75b in fiscal year that began April 1, and in the next fiscal year. La Presse newspaper reported it could top CAD100 billion.

- While small relative to GDP at around 2% it would be higher in cash terms than anything outside pandemic. Deficit was CAD328B in 2020-21, declined to CAD35B two years later, and moved up to CAD62B in 2023-24.

- First budget in almost 2Y after delays linked to Liberal leadership race, April's election taking Mark Carney to power, and US trade war uncertainty.

- Economists see little chance budget keeps pledge to lower debt- and deficit-to-GDP over next few years. Canada is doubling defense spending to 5% of GDP for NATO target.

- Carney needs some opposition votes to pass budget, avoid early election. Carney also plans to balance newly broken out operating budget in 3Y and use some of that cash to boost investment. Economists doubt his goal of cutting departmental spending more than 7% will be met.

- Investors not focused on Canada fiscal deterioration in world of rising government debt: 10Y bond yielding 3.15% Monday, below similar Treasury at 4.11%. Moody's affirmed Canada's triple-A rating Friday.

- CIBC: "Canada has to be careful not to let a cyclical bump in deficits turn into a large structural gap. What we’ll be eyeing on budget night is the projection for the future trend in interest costs as a share of GDP."

- National Bank Financial: "Even the most optimistic scenario shows Federal debt as a percentage of GDP rising from less than 50% to almost 60% over the next five years."

- And: "No matter the scenario, federal debt will rise, topping $2 trillion in a few years and could be flirting with $3 trillion in a decade’s time. It sounds like a lot—and it is—but scaled to GDP, the GoC debt stock could gradually level out assuming a structural deficit is addressed. Other jurisdictions (e.g., the U.S.) can’t say the same."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle High

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4045 3.0% Upper Bollinger Band

- RES 2: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 1: 1.3989 200-dma

- PRICE: 1.3953 @ 16:02 BST Oct 3

- SUP 1: 1.3897/3825 Low Sep 30 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact and yesterday’s break above the late September’s high, firms the bullish theme. This move higher also maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3825, the 50-day EMA.

AUDUSD TECHS: Support Remains Intact For Now

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6603 @ 16:01 BST Oct 3

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at 0.6558. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

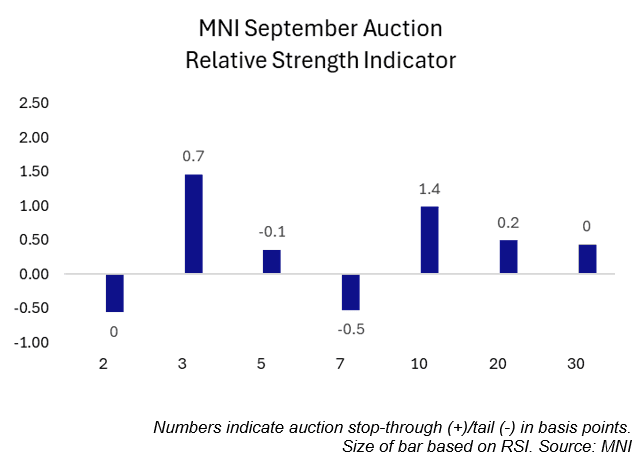

US TSYS/SUPPLY: September's Coupon Auctions Were Generally Solid (2/2)

September’s coupon auctions were generally solid, with three lines trading through, two coming out on the screws and two tailing slightly.

- Looking through the lens of MNI’s Relative Strength Indicator (RSI), five lines saw positive readings while two saw negative readings.

- The 3-year sale was the strongest auction of the month according to MNI’s RSI. The 3-year line traded through 0.7bps, the largest stop through in seven months. Meanwhile, the primary dealer take-up was just 8.4%, the lowest on record (data going back to 2003).

- The weakest sale of the month was the last – the 7-year line. This line saw the second consecutive 0.5bp tail, with the 12.0% primary dealer take-up above August’s 9.8% and July’s record low 4.1%.

September Auction Review:

- 2Y Note on-the-screws: 3.571% vs. 3.571% WI.

- 2Y FRN: 0.200% high margin vs. 0.195% prior

- 3Y Note trade-through: 3.485% vs. 3.492% WI.

- 5Y Note tail: 3.710% vs 3.709% WI.

- 7Y Note tail: 3.953% vs. 3.948% WI.

- 10Y Note trade-through: 4.033% vs. 4.047% WI.

- 10Y TIPS: 1.734% high yield vs. 1.985% prior

- 20Y Bond trade-through: 4.613% vs 4.615% WI.

- 30Y Bond on-the-screws: 4.651% vs. 4.651% WI.