US STOCKS: Can't Keep A Good Thing Down

The ESM5 Overnight range was 6046.25 - 6109.00, Asia is currently trading around 6060. A potentially protracted Middle East war, a short oil market surging and Stocks still cannot correct. This morning's post by President Trump that everyone should evacuate Tehran immediately has seen stocks open soft in our session, if something significant is not seen the danger is this move will also just be reversed. ESU5 -0.40%, NQU5 -0.50%

- ZeroHedge on X: “Retail favorite stocks exploding higher this morning; most are among the HF most shorted which means retail is again about to force another hedge fund deleveraging.”

- Andreas Steno Larson on X: “Powell & Co have been 100% wrong on inflation since March. They all flagged upside risks to PCE — and inflation fell instead. That misread is the dovish shift you will get this week. Risk now tilting balanced = steeper curve, risk-on, bullish crypto.”

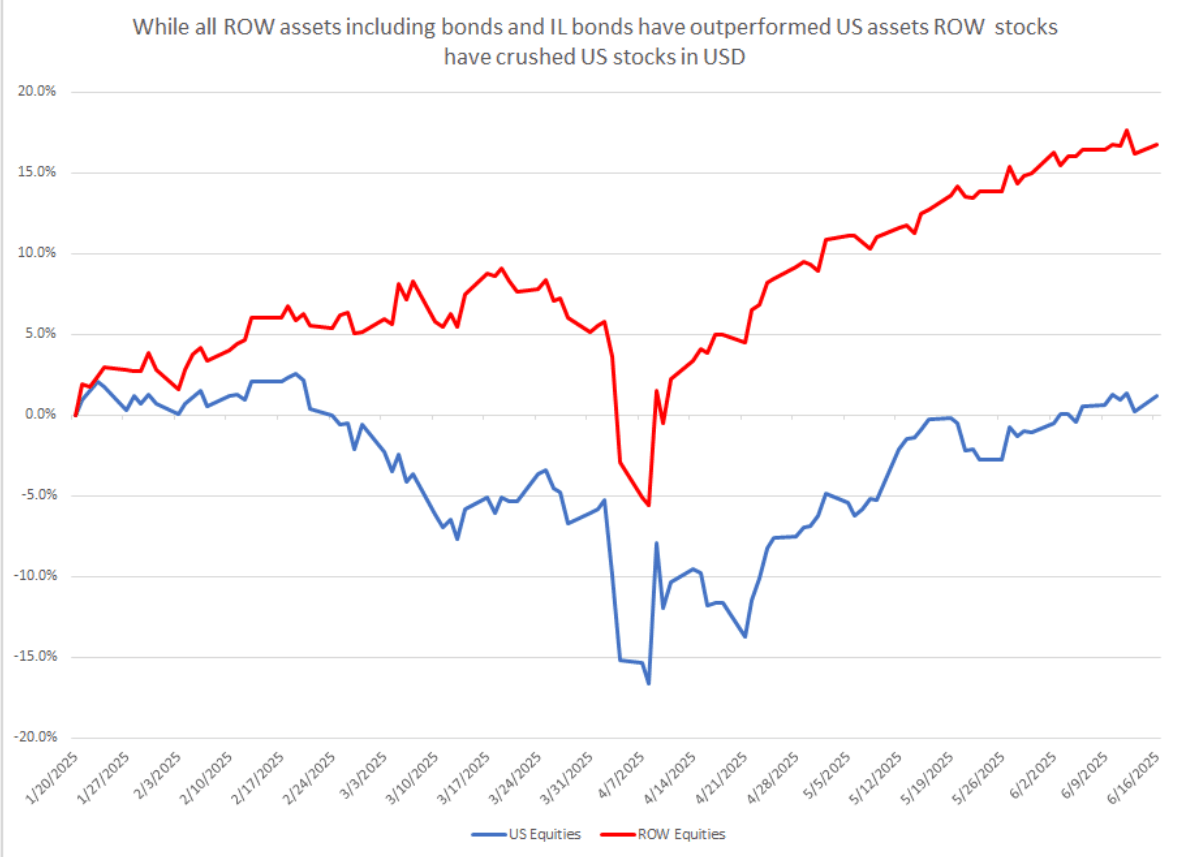

- Andy Constan on X: “The Get out of US Assets (Bonds + Stocks) and into ROW assets continues to be the dominant trend. Since inauguration and since we switched half of our USD Denominated Assets into ROW Assets. Even ROW equities continue to outperform in USD. It's a trend with plenty of room.” See Graph Below.

- The Shallow dips in US Equity markets continue to point to a market that has been caught underweight and is using any dips to get back in.

- Momentum type funds and share buybacks have kept the market well supported as an underweight market has been forced to reenter.

- Share buybacks are set to enter their blackout period starting this week, will the absence of this large underlying bid allow for some sort of a retracement.

In the short-term stocks continue to look overbought but it is very tough to fight this price action. The S&P looks set to test the 6100 area and through here focus will turn to the all-time highs.

Fig 1: US Equities Vs ROW Equities In USD

Source: Andy Costan,@dampedspring

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Downgrades US's AAA Rating As Deficits Seen Ballooning

Moody's has downgraded the US's long-term credit rating to Aa1 trom Aaa. The move may not have been fully expected today. But it was the last holdout among they S&P and Fitch to demote the USA from the top rating, and they placed negative outlook on the US last year (now stable). Fiscal deterioration, both past and anticipated as Congress wrangles with the Republican fiscal bill, is cited as the key factor. From the release (link):

- “While we recognize the US’ significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics."

- "This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns...We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration."

- "If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade. As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation."

- "We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024."

- "Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns."

US FISCAL: "Extraordinary Measures" Continue To Dwindle Amid Debt Impasse

The "extraordinary measures" available to Treasury to stave off a debt default were down to $82B as of May 14, per a Treasury Department release today.

- That compares unfavorably with a high of $335B in January when the debt limit impasse began. Combined with $562B in Treasury cash on hand, though, after April's large tax intakes, that makes for around $644B in available resources before the "x-date" is reached.

- Resources are gradually being eroded since reaching nearly $800B in mid-April.

- Per Tsy Sec Bessent's letter to Congress last week, "after reviewing receipts from the recent April tax filing season, there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July, before its scheduled break, to protect the full faith and credit of the United States."

CANADA DATA: Sales Activity Points To Potential Marking Up Of GDP Ests

There was mixed news on the housing and wholesale/manufacturing sales fronts this week, which on net look to slightly upwardly bias Q1 GDP estimates, pending next week's retail sales reading.

Housing starts blew through expectations at 278.6k in April (226.2k expected, 214.2k prior). This came after building permits fell a worse-than-expected 4.1% M/M in March as reported Wednesday.

- Meanwhile, he Canadian Real Estate Association reported existing home says April sales unexpectedly contracted -0.1% M/M (+1.0% expected, -4.8% prior). Sales are now down 9.8% Y/Y, while prices fell 1.2% M/M (3.6% Y/Y on the price index). (Link)

- Overall, confidence appears subdued, which is likely to translate into subdued activity.

On the sales front, March data was soft but positive versus expectations and could add a slight upward drift to Q1 GDP expectations.

- Manufacturing sales were less negative than expected at -1.4% M/M (-1.9% expected/flash estimate, -0.2% prior rev up 0.4pp). The decline was led by primary metals -6.5%, an area hit by U.S. tariffs, and oil -4.2%. Overall Q1 factory sales grew +1.6% vs prior +1.1%.(Link)

- Wholesales ex-petroleum and grains rose 0.2% in March, vs the advance estimate / consensus -0.3%. Sales volumes fell 0.3%. Overall Q1 wholesales rose 2.5%, led by machinery/equipment and autos/parts.