CANADA DATA: Canada Oct Payroll Employment +21.2K Vs Sept -23.4K

Dec-18 14:03

- Payroll employment +68K YOY or +0.4% in Oct.

- Manufacturing -3K MOM and -31K YOY, as the sector continues to face tariff pressures.

- Average weekly earnings +2.2% YOY, slowing from +2.9% in Sept.

- Payroll growth is consistent with BOC Governor Macklem's view that the economy is showing signs of resilience over recession.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

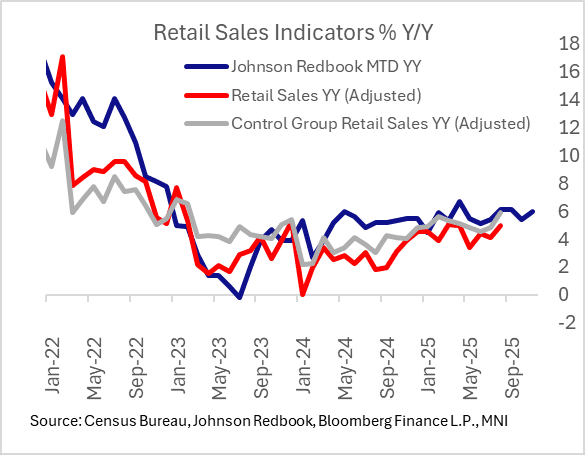

US DATA: Redbook Retail Sales Maintain Robust Pace, Q4 Still Looking Solid

Nov-18 13:59

In yet another indicator of solid retail sales continuing into Q4, the latest Johnson Redbook Retail Sales Index posted a 6.1% Y/Y rise in the week ending Nov 15, a pickup from 5.9% the prior week. This brought month-to-date sales gains to 6.0% Y/Y (note, retailers target a 6.7% gain).

- We still don't have release dates for the delayed September and October reports, but we expect them to print solidly, at least in nominal terms (which is how US retail sales are expressed).

- Between the Chicago Fed's CARTS retail sales ex-autos estimates for September and October, and Redbook, Control Group sales looks to be running at the fastest quarterly-equivalent pace since Q3 2024 as of October, with November looking good as well so far.

- Per Redbook, "Promotions for Veterans Day contributed to an increase in foot traffic and sales at the beginning of the week."

- The report notes that this is a "crucial month for retail, as it coincides with the third quarter reporting season and the holiday promotional calendar, which is already in full swing. Holiday merchandise has begun to be displayed in stores. Retailers have introduced online and in-store Pre-Black Friday deals earlier than ever to encourage shoppers to make purchases. Sales are expected to gradually strengthen as we approach Thanksgiving and the start of the holiday season."

MNI: US REDBOOK: NOV STORE SALES +6.0% V YR AGO MO

Nov-18 13:55

- MNI: US REDBOOK: NOV STORE SALES +6.0% V YR AGO MO

- US REDBOOK: STORE SALES +6.1% WK ENDED NOV 15 V YR AGO WK

STIR: Markets Price Slightly Greater Than Even Odds Of Fed Dec Cut

Nov-18 13:53

Dovish repricing in the U.S. front end in the wake of the negative weekly ADP employment print and downward revisions covered in recent bullets.

- Liquid FOMC-dated OIS 1-2bp more dovish when compared to pre-data levels, showing 13.5bp of easing for next month, 24bp through January, 35bp through March, 42bp through April and 58bp through June.

- A reminder that December meeting pricing moved to 10.5bp of easing at one point yesterday.

- SOFR futures now 0.5-5.5 firmer on the day vs. 0.5-3.5 higher pre-data, with implied terminal rate pricing 3.05% vs. 3.07% heading into the data