MNI EXCLUSIVE: BoJ Communication Discussion

MNI discusses how the BOJ plans to communicate its neutral-rate estimate following a potential hike.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

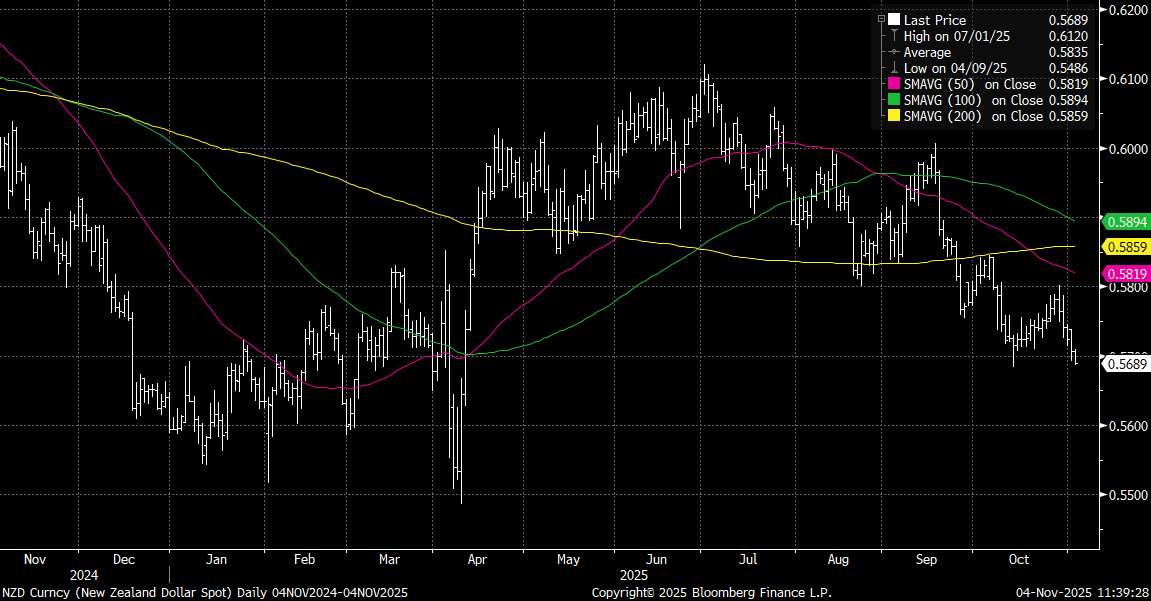

NZD: NZD/USD Near Mid Oct Lows, Tracking Sub 0.5700

The Kiwi is the weakest performer in the G10 space, back close to mid Oct lows (0.5683), see the chart below. A fresh break lower targets the 0.55/0.5600 region. Fresh highs in AUD/NZD (last around 1.1480), as we await the RBA later, likely aiding NZD underperformance (we also have NZ jobs data tomorrow). Anything which pushes out the RBA easing timing, with inflation forecasts key, could see a 1.1500 test in the cross.

Fig 1: NZD/USD Eyeing Test Sub Mid Oct Lows

Source: Bloomberg Finance L.P./MNI

CNH: USD/CNY Fixing Egdes Up, But Error Term Wider, Aiding CNH Outperformance

The USD/CNY fixing printed at 7.0885, up on yesterday's outcome (7.0867), but well below market forecasts. The fixing error widened to -363pips, fresh wides since early Sep of this year. This continues to see the fixing bias lean against the higher dollar levels. In turn this should aid CNH outperformance on key crosses. USD/CNH was a little higher in latest dealings, last near 7.1295, while USD indices were 0.10% higher. CNH/JPY is above 21.66, eyeing a move above 21.70, which marked recent highs. EUR/CNH is testing under 8.2000.

RBA: Updated Inflation Forecasts Key To Monetary Policy Outlook

The RBA is widely expected to leave rates at 3.6% when its decision is announced today at 1430 AEDT. As a result, there will be particular focus on the statement tone but also the accompanying updated staff forecasts to determine the monetary policy outlook. Given trimmed mean inflation’s “material miss” in Q3, the question is how far the target of around 2.5% will be pushed or will the higher market rate profile mean that it still returns to 2.6% in Q2 2026. Changes to the RBA’s growth, especially consumption, and jobs forecasts are also likely to be a focus.

- The 0.3pp pickup in trimmed mean inflation in Q3 to 3%, the top of the RBA’s band and well above the August forecast of 2.6% for Q4, put an end to November easing expectations and also likely ruled out December. A meagre 0.2% q/q rise is needed to achieve 2.6% in Q4, which hasn’t happened since 2016 outside of Covid.

- If the RBA continues to expect 2.6% underlying inflation in Q2 and Q4 2026, possibly driven by higher market rates and softer labour market, then rate cut expectations are likely to rise again. Currently the AUD OIS market doesn’t have a full 25bp priced in.

- However, if Q4 2026 is forecast to be above 2.6% at even 2.7-2.8%, then an extended pause is likely to be the base case.

- The Q4 2025 unemployment rate may be revised higher after Q3 came in at 4.3%, the RBA’s August Q4 projection. Employment growth was also slower than it expected. Any weakening of 2026 projections could drive wage expectations down and thus help inflation.

- See MNI RBA Preview.