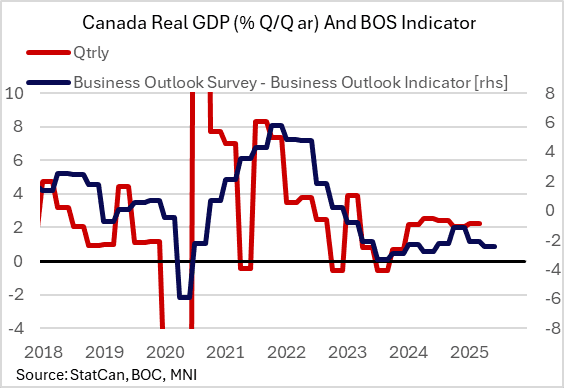

CANADA: BOC Business Outlook Survey Roughly Neutral For Rate Path (1/3)

The Bank of Canada's quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations (CSCE) showed broadly that the economy and inflation expectations stabilized between February (the Q1 survey) and May (the Q2 report released this month).

- Neither survey's findings are an obstacle for further BOC rate cuts, but nor do they make a compelling case for further easing (although the consumer survey was clearly the weaker of the two).

- Additionally, there is something of a staleness about the Q2 survey, whose responses were collected before US Pres Trump raised his tariff threat to 35% while pushing back his deadline to Aug. 1. As such there was only limited market reaction to the Q2 release on July 21.

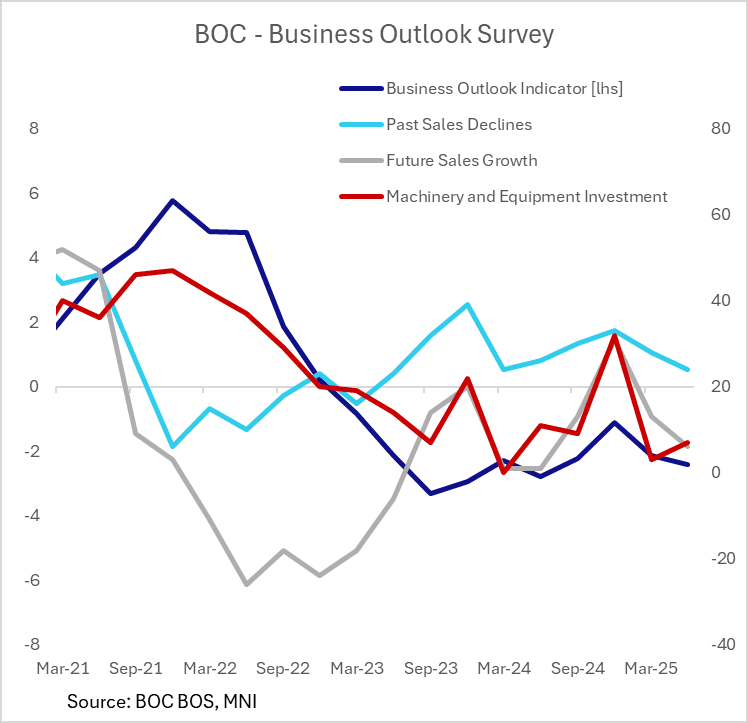

- In the BOS, the 0.3 point drop in the Business Outlook Indicator (-2.42) in Q2 brought the level to the lowest since Q4 2023 but was a stabilization of sorts compare to the 1 point drop between Q4 2024 and Q1 2025 (which was the largest since early 2023 albeit that was from a much higher starting level). Past and future sales dropped to the lowest level since Q1 2024, with indicators of future sales at -6, the lowest since Q4 2023.

- 28% of business owners expect a recession in the next 12 months.

- Even so, machinery investment intentions and future employment actually picked up slightly.

- From the report: "Tariffs and related uncertainty, along with spillover effects on the Canadian and global economies, continue to have major impacts on businesses’ outlooks. However, the worst-case scenarios that firms envisioned last quarter are now seen as less likely to occur. Sales outlooks remain pessimistic overall due to widespread concerns about the broader effects of a slowing economy. But recent monthly survey results suggest some improvement in firms’ outlooks—particularly among exporters—because few have been directly affected by the current tariffs. Uncertainty continues to drive cautiousness in outlooks for hiring and investment. Most firms expect to maintain current staffing levels and limit investment to regular maintenance over the next 12 months."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: May CPI Preview: Analysts Eyeing Services Closely (3/3)

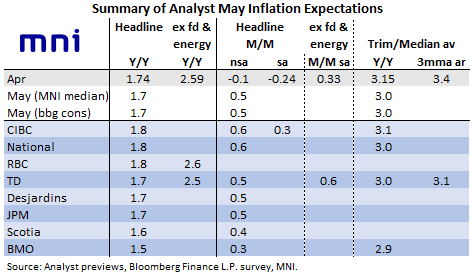

Selected Sell-Side commentary from May CPI previews:

- CIBC (Headline 1.8% Y/Y / 0.6% M/M; Trim/Median 3.1% Y/Y): "The acceleration in the monthly pace will be largely tied to food prices that are picking up counter tariff impacts, and core goods prices that could begin to reflect broader tariffs...We expect rent inflation to decelerate after a surprising jump in April, and in line with industry data, leaning against food price increases... The Bank of Canada will need to see a cooling in its key core measures to feel comfortable cutting in July as we expect."

- RBC (Headline 1.8% Y/Y / 2.6% ex-food/energy): "The removal of the consumer carbon tax in April in most provinces will continue to keep energy prices well below levels from a year ago. The Bank of Canada’s preferred core measures (which exclude indirect taxes like the carbon tax) likely eased slightly after exceeding 3% in April."

- TD (Headline 1.7% Y/Y / 0.5% M/M; Trim/Median 3.0% Y/Y): Prices to be "underpinned by strength in core goods and food. Softer energy

prices will offer a modest offset, along with continued deceleration across shelter." The report overall "should give the Bank of Canada some new evidence that inflation pressures are starting to stabilize from the stronger momentum entering 2025.... Ultimately, we will looking at the next May/June CPI reports together (along with industry-level GDP for April) ahead of the July policy decision, and while our base case for CPI should leave an open path to a July rate cut, another upside surprise on CPI-trim/median (or Friday's GDP report) would prove much harder to look past." - Scotiabank (Headline 1.6% Y/Y / 0.4% M/M): "shelter cost inflation has been ebbing and with help from the elimination of the consumer portion of the carbon tax and the effects on home energy bills, but not because of rent inflation that remains sticky. Gasoline is not expected to be a material driver ex-taxes, but energy in general won’t be the same carbon-tax driven drag on m/m CPI that it was the prior month. Key will be services that were a significant part of the contributions to April CPI in categories like travel, rent, and health care...It’s feasible we see cooler m/m SAAR pressures in May off of the strong readings in April and effects cited above. The measures exclude all taxes including tariffs and so there will be no direct effect of tariffs on the core gauges, but there could well be indirect ones. A lousy two months of inflation data after overshooting for a year and with long and variable lags surrounding global supply chain responses to trade wars should merit setting a higher standard for evaluating pressures than just two months."

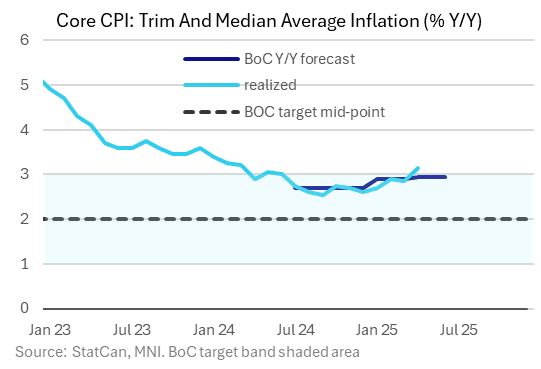

CANADA: May CPI Preview: Q2 Inflation Set To Remain Above BOC Estimates (2/3)

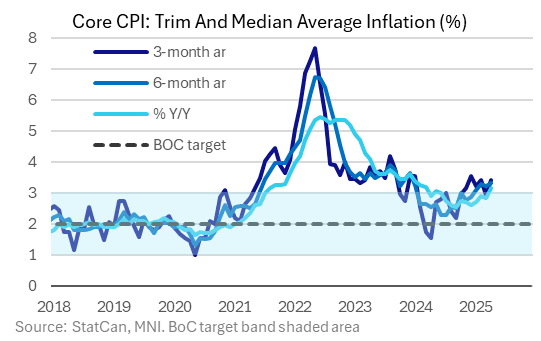

April CPI: April's 3.15% trim/median average represented inflation above target and tracking above the BOC's latest quarterly forecast for Q2 of 2.95% (taking the average of the BoC's two trade scenarios).

- Despite a soft headline print in April of 1.7%, Gov Macklem said last week that "The bottom line is we have seen more firmness in underlying inflation and that's something that's gotten our attention" though he raised some doubt over the underlying signal for policymakers: "There's some unusual volatility - how temporary or persistent this is remains an open question" (he previously noted some components such as travel on this front) while noting that the bank's trim and median core inflation measures may overstate the broader trend: "There is I think potentially some distortion in our core measures, maybe exaggerating a little bit. Underlying inflation, certainly above 2 (percent) and it's probably a little bit lower than our preferred measures."

- There were arguably some mitigating factors in the April report details, for instance a slight downtick in inflation breadth, but there were strong readings through the report including services (3.5%, up from 3.1% prior) and durable goods (1.7%, highest since Q2 2023, after 1.1%) as well as on other core metrics (ex 8 most volatile & indirect taxes up to 2.5% from 2.2% prior). Gasoline prices -18%, travel tours +6.7% and food prices +3.8% moderated the decline in headline CPI; Grocery prices were elevated for a third straight month.

- May components: Among the larger items in the core CPI basket, services will be eyed most closely - expectations appear to be softer housing inflation to continue, with travel and other volatile categories also potentially pulling back from April's sharp gains. Energy is seen falling sharply Y/Y again following the removal of the consumer carbon tax at the start of April (was -12.7% Y/Y in April), while food prices are broadly seen decelerating Y/Y from 3.8% in April but still solid. Core goods prices are seen higher than the prior 0.9% Y/Y but the stronger CAD is seen as a headwind offsetting tariff tailwinds.

- Idiosyncratic Factors: As the M/M consensus indicates, May NSA price rises are typically strong. Meanwhile the annual reweighting of the CPI basket, whose results were announced last week, were modest and are not expected to have any material impact on May's figures. However, they are likely to be mentioned in the release, even if only for StatCan to reassure that there was limited impact.

USDCAD TECHS: Approaching The 50-Day EMA

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.3828 50-day EMA

- PRICE: 1.3746 @ 15:48 BST Jun 23

- SUP 1: 1.3635 Low Jun 18

- SUP 2: 1.3540/3525 Low Jun 16 / 1.0% 10-dma envelope

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A primary downtrend in USDCAD remains intact and recent gains are considered corrective. Resistance at the 20-day EMA, at 1.3713, has been breached. A continuation higher would signal scope for a stronger retracement and expose pivot resistance at the 50-day EMA, at 1.3828. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. A break of this price point would resume the downtrend.