BTP: Block trade

Aug-20 08:23

BTP Block trade, suggest unconfirmed seller:

- IKU5 ~1.29k at 120.40.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Goldman Sachs Recommend Short ERZ6 vs. Long SFIZ6

Jul-21 08:19

Late on Friday Goldman Sachs recommended short ERZ6 vs. long SFIZ6.

- They continue to expect one more ECB cut, in September, and think “think the prospect of German fiscal expansion will keep 2026-2027 pricing at current levels or higher in yield”.

- Meanwhile they note that the quantity side the UK labour market data is “increasingly softening, which has been acknowledged by multiple MPC speakers, and weaker global growth remains a headwind to UK activity”. While they do not expect “any notable updates to the borrowing figures, the potential for higher taxes at the autumn budget may also weigh on demand. Combined with a decline in inflation from elevated levels, this should still see the BoE cut well below market pricing through 2026”.

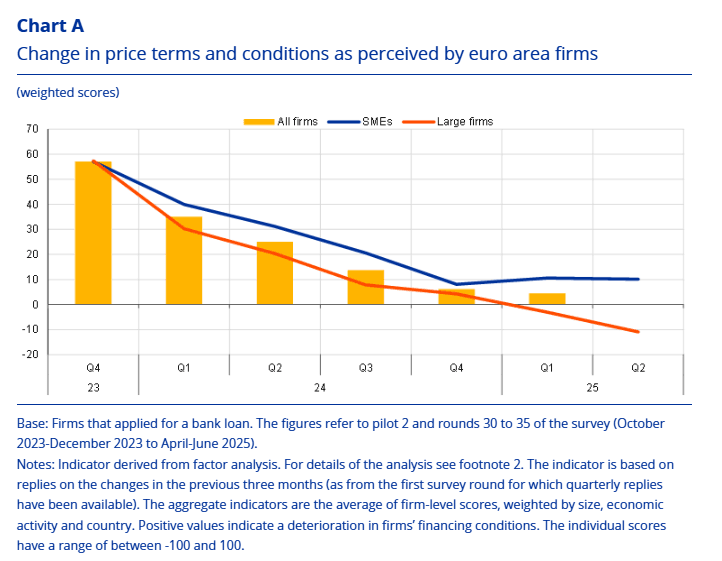

ECB: Q2 SAFE: Rate Cuts Feeding Through But Near-term Business Prospects Subdued

Jul-21 08:19

The ECB‘s Q2 SAFE survey (link) suggests rate cuts are continuing to feed through into lending condtioisns and demand. However, near term prospects for business activity remain subdued.

- Q2 business activity appears weaker than in Q1: “Relatively few firms reported an increase in turnover, and expectations for the next quarter have become less optimistic”…“Meanwhile, firms continued to report a deterioration in profits”.

- Q2 investment was weaker than the previous survey, but “firms remain optimistic about future investment”. “Investing in artificial intelligence technologies (AI) was reported by 34% of firms, with an average of 5.6% of overall investment”.

- On trade tensions, “firms reported considerable challenges”….”22% of firms reported a high impact, 31% reported a medium impact and 47% reported a low impact”. “Survey replies reveal the efforts of euro area firms to adapt to changing trade dynamics”, namely “refocusing sales within domestic and EU markets (38%), diversifying into non-EU markets (21%) and restructuring supply chains”.

- As a precursor to tomorrow’s Bank Lending Survey (albeit from the perspective of firms rather than Banks), “a higher share of firms reported applying for bank loans compared with the previous survey”…"the percentage of firms reporting obstacles to obtaining a bank loan remained low” and “firms continued to report an increase in banks' willingness to lend”

- In line with ongoing ECB rate cuts through Q2, “an estimated indicator of firms’ financing conditions, which shows no further tightening compared with the previous quarter, confirms lower pricing conditions for firms”.

- 3 and 5-year ahead inflation expectations were unchanged at 3.0%, but “the majority of firms, albeit fewer than in the previous wave, continue to indicate upside risks to long-term inflation expectations”.

BONDS: New Session Highs

Jul-21 08:12

Another round of demand for core global FI takes major bond futures to fresh session highs in recent trade. Once again, no clear headline drivers here, with our best guess being that EGB outperformance is being driven by the hawkish U.S. tariff reports from late on Friday/over the weekend.