MEXICO: Banxico Releases Minutes Of August MPC Meeting

Aug-21 15:00

- The minutes to the August 7 MPC meeting are here.

- At that meeting, the Board delivered the expected 25bp rate cut to 7.75% in a split 4-1 decision, with Deputy Governor Heath voting to stay on hold.

- The Board also maintained its forward guidance, hinting at additional rate cuts ahead.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD Sold Hard into 4pm WMR Fix

Jul-22 15:00

- USD is being sold in recent trade - helping boost EUR/USD through yesterday's highs just a few minutes out from the 4pm WMR fix. The volume impact is evident here: very, very decent size crossing in the past few minutes: almost 10k contracts trade over ~5 minutes for a cash equivalent of ~$1.4bln

BONDS: Gilt Futures Through Resistance, Now Outperforming Bunds

Jul-22 14:57

Gilt futures have pierced initial resistance at the 20-day EMA (91.97), now +35 ticks versus yesterday’s settlement at 92.13 and a more notable +67 ticks up from earlier session lows. A clear break of the 20-day EMA would call into question the current bear cycle, and signal scope for a push towards 92.24 (July 15 high).

- Beta to US Treasuries appears to have been the main driver of this afternoon’s Gilt rally. US Treasury Secretary Bessent continued to suggest that an ousting of Powell as Fed Chair is unlikely in the short-term. This will be helping to assuage immediate concerns around Fed credibility/independence, pulling down US breakeven inflation rates in the process.

- Gilt yields are 2.5 to 4bps lower across the curve, with UST yields down 3.5-4.5bps.

- Bund futures have also been supported this afternoon, currently +28 ticks at 130.73, at fresh session highs and probing initial resistance at 130.76 (Jul 4 high).

- BTP futures underperform Bunds (+17 ticks at 121.37), owing to the 1% intraday fall in European equities.

- The 10-year Gilt/Bund spread is now 1bp tighter today at 198bps, after briefly piercing the 200bps handle this morning after the UK public sector finance data.

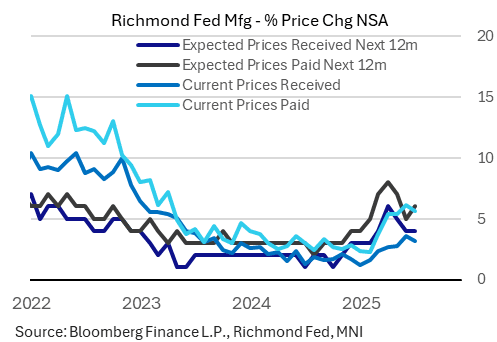

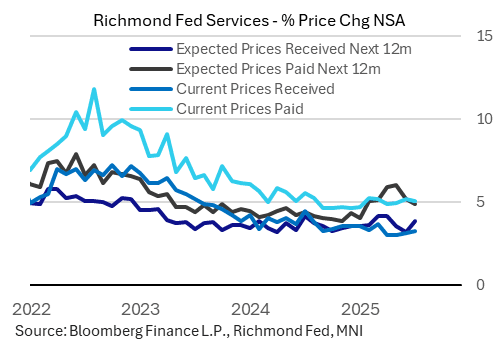

US DATA: Richmond Fed Regional Inflation Pressures Abating Slightly (2/2)

Jul-22 14:57

One commonality in the Richmond Fed's services and manufacturing surveys for July was that price pressures were seen to have abated from the tariff-panicked peak earlier in the year.

- Manufacturing current prices paid (expressed in the survey as a % Y/Y change) dipped to 5.7% from 6.1%, with received to 3.2% from 3.6%. Expected (12-month) prices paid rose to 6.0% from 5.0%, but just a 2-month high and vs an 8% peak, with expected prices received steady at 4.0%.

- For Services, current prices received fell to 5.1% from 5.2% prior; received ticked up to 3.3% from 3.2% but this remained well below March's 3.7% high. Expected prices paid fell to a 6-month low 4.9% (5.2% prior), though received rose to 3.9% from 3.2%.

- As with the activity portion of the survey, this is a slight divergence that's just one month but could portend something more meaningful: services firms are slightly less concerned over future margins (expected prices paid less received) than they were over the prior 3 months, whereas manufacturers appear to view tougher margin pressures than they did a month earlier.

- That would, of course, chime with tariffs being the primary driver of incoming prices paid.