AMERICAS OIL: Baker Hughes Regional Update – Week of October 24th

Oct-24 17:53

See Regional Breakdown Here: MNI_Baker Hughes Summary_2025-10-24.pdf

Total US rigs were up 2 this week, with the addition of 2 oil rigs. Canada added 1 miscellaneous rig offshore week-over-week.

- Permian, Williston and Marcellus horizontal rigs all held flat week-over-week, holding at 235 rigs, 28 rigs, and 21 rigs, respectively.

- The Haynesville rig count fell by 1 rig this week, reaching 39 rigs. The basin added rigs between mid-March and mid-July, rising from 28 to 41 rigs, but activity has held flat around 38-40 rigs since July.

- Alberta lost 1 horizontal rig week-over-week but remains up 4 rigs from last month and only 7 below the same time last year.

- British Columbia gained 1 horizontal rigs, remains 5 rigs below last year’s levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Nov'25 10Y Skew Play

Sep-24 17:45

- +15,000 TYX5 111/112 put spds 1 over 114 calls ref 112-22.5

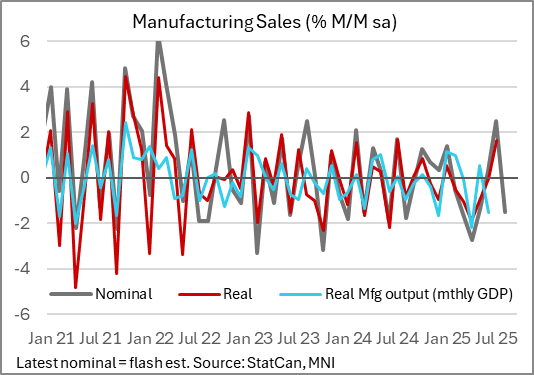

CANADA DATA: Pullback In Aug Manufacturing Sales In Line With Monthly Volatility

Sep-24 17:36

StatCan's advance estimate of manufacturing sales for August is for a 1.5% M/M decrease, which if confirmed would mark the first decrease in 3 months and partially reversing the 2.5% rise in July (all in value and not volume terms).

- As usual with the advance estimate there were no further details available, though StatCan reports the largest decreases were in the transportation equipment and food subsectors.

- Even with the M/M decrease, the comparison with the sharp drawdown in March /April/May means that manufacturing sales were due to post a 6-month best -1.5% on a 3M/3M annualized basis.

- As with other indicators, though, this one suggests the nascent pickup in activity and sentiment in various sectors in the summer - after the worst of the US-Canada trade conflict concerns - has subsequently petered out, with activity remaining volatile.

- We get July GDP data on Friday, with expectations and the advance estimate showing +0.1% M/M after -0.1% in June. Per StatCan's advance GDP release, there were no notable mentions of July manufacturing output :"Increases in real estate and rental and leasing, mining and quarrying (except oil and gas) and wholesale trade were partially offset by a decrease in retail trade" in the month.

- July manufacturing sales were confirmed at 2.5% last week, with wholesale sales ex-petroleum growth reported at 1.2% - so three of the four major "sales" categories point to a pickup in July activity (retail sales fell 0.8% however), in line with the StatCan advance anecdote).

- For August, retail sales are estimated to have bounced (1.0% M/M).

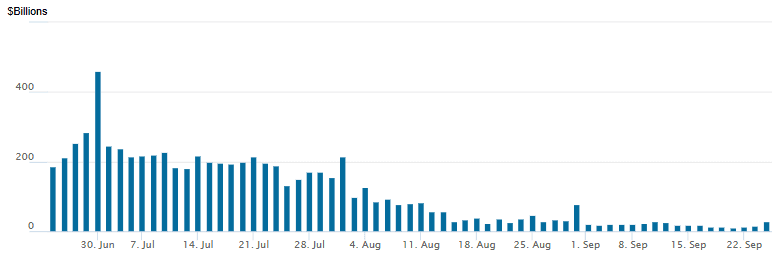

US: FED Reverse Repo Operation

Sep-24 17:30

RRP usage bounces to $29.172B with 22 counterparties this afternoon from $14.402B Tuesday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.