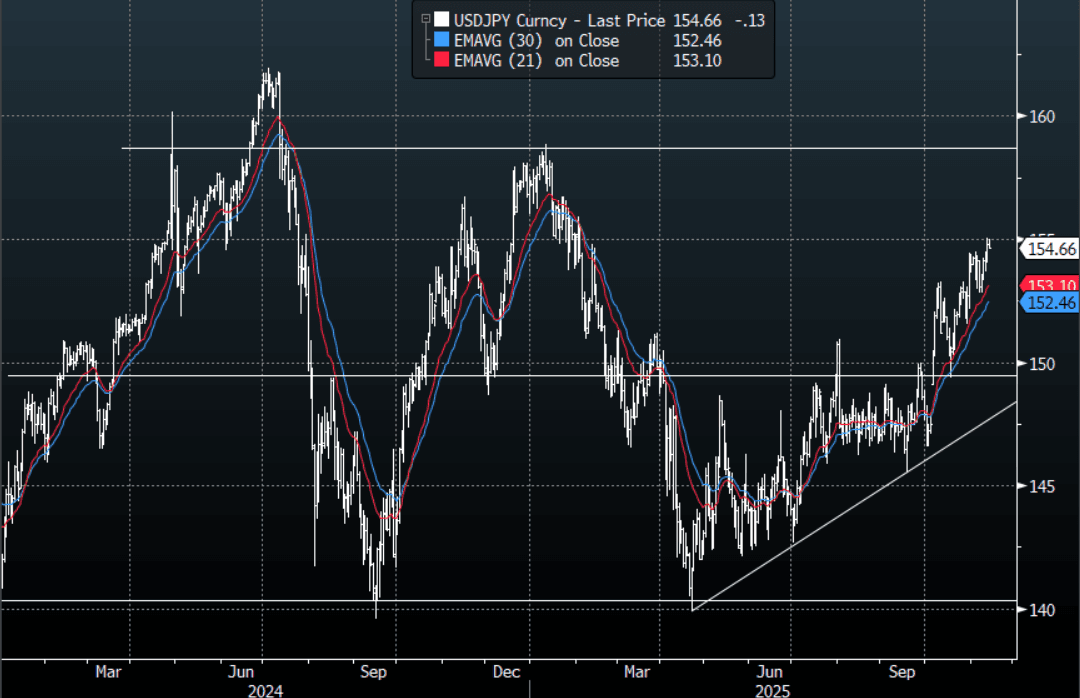

JPY: Asia- Pac: USD/JPY Capped Around 155.00 Again

The USD/JPY range today has been 154.63 - 155.01 in the Asia-Pac session, it is currently trading around 154.70, -0.05%. The pair stalled again around the 155.00 area as it did overnight. The return of a positive sentiment in risk has brought the focus in USD/JPY back to the 154-155 resistance area. A sustained break above this area is needed to potentially see the uptrend begin another extension higher, the focus would then turn toward the 160 area where I would start to become wary of intervention risks. On the day the support toward 154.30-154.50 needs to hold in order to have another test of the 155.00 area. More Jaw-Boning from Katayama overnight points to officials understanding what the risk of a move back through this area poses. The first strong buy-zone is back toward 152.50 then the more important 149-150 area.

- MNI BRIEF: BOJ's Ueda Sees Underlying CPI Toward 2% Target. He said Thursday that underlying CPI inflation, excluding temporary factors, is gradually moving toward the bank’s 2% target, and that the mechanism in which wages and prices rise moderately in tandem will be maintained. Ueda is scheduled to deliver a speech in early December ahead of the Bank’s next policy meeting, which is expected to provide a stronger signal on the BOJ’s next move.

- MNI AU - Import Prices Rising M/M, As USD/JPY Firms, But Y/Y Still Negative: Rebounding USD/JPY levels has helped push up imported price pressures in Japan. Recent comments from Japan policy makers suggest the weaker yen's impact is not going unnoticed. Still, it remains to be seen if we see policy steps to address this, particularly as PM Takaichi remarks seemingly push back against an aggressive BoJ tightening cycle.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 155.00($978m Nov17) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 101 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Move Higher in Yields Stalls in the Afternoon

- As treasuries began trading in the Asia trading day, yields across the curve opened 1-3bps higher before taking back some of the early moves.

- The US 2-Yr traded up at 3.515%, but rallied back to again test a near term support of 3.50% that it has been unable to hold below.

- The US 5-Yr is back to flat at 3.63% having been +2bps higher in the morning session.

- The US 10-Yr is up +1bps to 4.04%, having opened at 4.06%. Last week it failed to test 4.00% and looks likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out. With FED speakers in coming days and the FEDs Powell's economic address at the NABE meeting, treasury traders will be looking for signals for monetary policy that could challenge this current range.

- The US 30-Yr is up +2bps at 4.64% just off the Tuesday morning high of 4.65%.

- Futures are edging lower too as TYZ5 is has not traded too far from where it started the day and is currently +01 at 113-06

OIL: Crude Range Trading As Watching US-China & Supply/Demand Developments

Oil prices are slightly higher but have been trading within a narrow range during today’s APAC session with no new developments to give it direction. Later on Tuesday though, the IEA’s October report, US industry-based inventory data and Fed Chair Powell comments on the economy have the potential to move crude. Brent is up 0.4% to $63.56/bbl off the intraday low of $63.41 following a peak of $63.63. WTI is 0.4% higher at $59.72/bbl after reaching $59.82. The USD index is slightly lower.

- OPEC left its oil market outlook unchanged with demand forecast to rise by 1.3mbd in 2025 and 1.4mbd in 2026. The IEA releases its monthly report Tuesday and tends to be less optimistic than OPEC. It has been projecting a record market surplus for 2026.

- US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and that the US should negotiate. Oil is likely to sell off if there is any deterioration in the situation as it remains concerned about the impact on energy demand from increased protectionism.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism, UK labour market data and German September HICP and euro area October ZEW print.

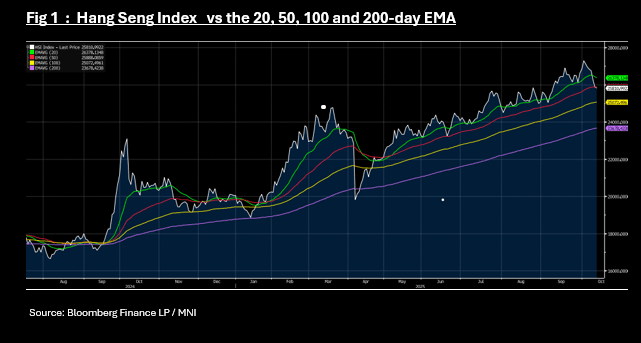

ASIA STOCKS: Equities Remain Weak as HSI Breaks Through Key Technical

With Japan back today playing catch up from yesterday's weakness, most key markets in the region have moved lower Tuesday. This comes despite the better global risk tones on Monday, as Trump softened his language around China (after tariff threats late on Friday).

Having closed at new highs Thursday, the NIKKEI's falls started Friday on apparent profit taking which was then over ran by Trump's comments as risk appetite declined. Out yesterday for a public holiday, Japanese investors continued to sell today taking the NIKKEI lower by -1.30%.

In Hong Kong the Hang Seng fell -0.45% today, despite trying to open stronger and traded through the 50-day EMA of 25,886. Were the HSI to hold below the 50-day EMA it would be the first time since the trade war induced sell off from April which then resulted in a near on five month rally to new highs. Other key Chinese bourses did little holding near to opening levels.

The KOSPI was a regional exception jumping +0.50% today as the 19% constituent - Samsung - beat profit estimates for its most recent quarter and its biggest quarterly profit in three years.

Following a terrible end to September for the NIFTY 50, it has rallied seven out of nine trading days in October. Against the regionally weak backdrop yesterday, the NIFTY 50's fall of -0.23% was a relative outperformance and in opening trade Tuesday it has recovered yesterday's falls.