HYBRIDS: Arkema (AKEFP): Hybrid Redemption

* FR0013478252 AKEFP 1.5 NC26 will be called on 21st Jan. * IR replied to me to let me know that the...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (H6) Bearish Outlook

- RES 4: 113-09 76.4% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 2: 112-27+ High Dec 5

- RES 1: 112-22+/23 High Dec 16 / 11

- PRICE: 112-15+ @ 16:48 GMT Dec 16

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

A bear theme in Treasuries remains intact. Today’s volatile activity resulted in a brief test above the 20-day EMA, at 112-20. The outlook remains bearish. A continuation lower would refocus attention on key support at 111-29, the Dec 10 low. Clearance of this level would confirm a resumption of the bear leg and open 111-19, a Fibonacci projection. On the upside, a clear breach of 112-23, the Dec 12 high would strengthen a S/T bull cycle.

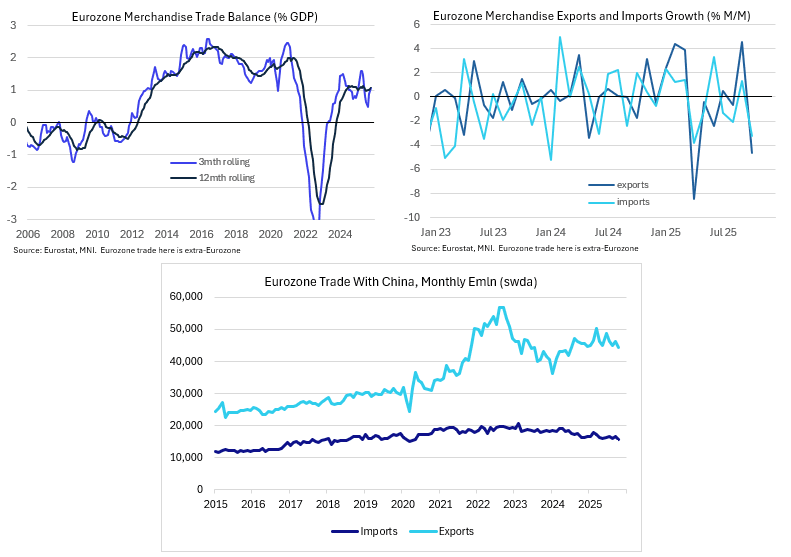

EUROZONE DATA: Little In October Data To Turn EU Stance On China Trade (2/2)

From a regional perspective, European trade with China remains in focus as pushback from the bloc continues; just over the weekend, the EU's justice commissioner floated plans on a crackdown on “very dangerous” products sold on online platforms including China’s Shein and Alibaba.

- October data does little to suggest the reported EC strategy of "derisking" its economic relationship with China will take a sudden turn. A "Fortress Europe" remains a possibility looking at current reports.

- Eurozone exports to China were E15.8bln in October (swda), -5.1% M/M and indeed the lowest monthly value since May 2020. Imports from China meanwhile decreased 4.1% M/M at E44.5bln, the lowest since July 2024.

- This means longer-term trends on EZ-China trade are intact: Exports to China remain on a downtrend while imports have been volatile but remain well of their highs.

- Recapping the European stance on the matter, officials seem cautious about tools aimed at tackling subsidies and dumping when a key potential upside driver of Eurozone imports from China are China’s own weak domestic demand and overcapacity.

- Taking the data at face value, these risks have not materialized (yet) - having said that, October data, again, will do little to question these beliefs.

- The EU could come closer to a joint China strategy at an informal summit in February, MNI understands.

EUROZONE DATA: Trade Surplus Normalizes as Chemicals Exports Drop (1/2)

The October fall in the Eurozone merchandise trade surplus was heavily driven by chemicals exports falling back to August levels, after a one-off jump in September. That tallies well with Eurozone net exports roughly stabilizing in real terms over the medium term.

- The Eurozone merchandise trade surplus fell to E14.0bn on a swda basis back in October after a downward revised E18.6bn (initially E18.7bn) in September which had been the highest monthly surplus since February.

- This means that as a 12-month rolling % of GDP, the Eurozone goods trade surplus appears to stabilize roughly around the 1.0% mark, a level reached in Q2 '24.

- The deterioration in the monthly trade balance vs September comes as exports declined 4.6% M/M, outstripping a decline in imports of 3.3%.

- Across categories, exports fell predominantly in the "manufactured goods" category, driven by 20.1% M/M fall in "chemicals and related products" after a jump of similar magnitude in September. Elsewhere, food, drinks and tobacco exports exhibit a bit of a downtrend recently, with a 0.8% M/M fall in October representing the fourth sequential fall in a row.

- As for imports, broad-based sequential October declines look a bit spurious, with food, drinks and tobacco down 3.7% M/M (-2.0% Sep), raw materials at -4.1% (-2.8 Sep), mineral fuels, lubricants and related materials at -10.9% (-2.6% Sep), and manufactured goods at -4.4% (2.0% Sep).

- The questions here come from the miscellaneous category which surged 135.6% M/M but there is a high chance this will be downwardly revised over the coming months, allocating the imports correctly. Nevertheless, the headline -3.3% M/M figure was also the weakest since April.