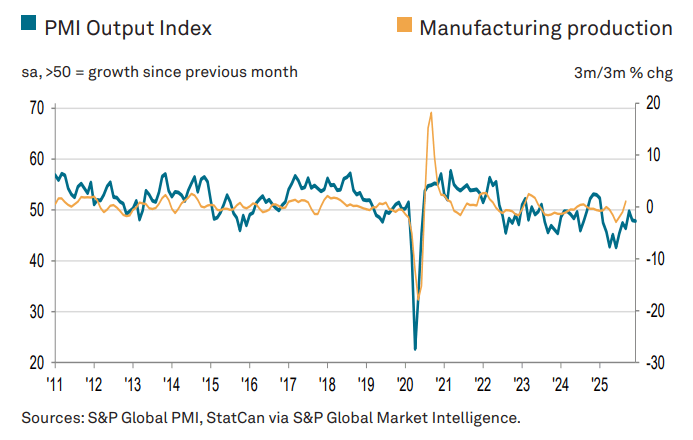

CANADA DATA: Another Soft PMI Points To Continued Soft Manufacturing Activity

Jan-02 14:37

The S&P Global Manufacturing PMI for Canada was relatively steady in December at 48.6 vs 48.4 in November (no consensus), consistent with recent other indicators pointing to flat growth in the 4th quarter. This was the 11th consecutive month below 50.0, consistent with chronic softening activity in a sector beleaguered by the US-Canada trade conflict.

- Per the report: "The performance of Canada’s manufacturing economy worsened again at the end of 2025. Output and new orders fell as tariffs and broad market uncertainty continued to weigh on the sector. Supply-side delays were again apparent, whilst the survey’s price indices picked up since November. Job losses were also reported, whilst confidence in the outlook remained historically subdued."

- Tariffs remained the key theme. "Panellists reported that market uncertainty remained a key depressor of sales, especially in relation to tariffs. This was again especially the case for exports, which declined steeply and at the quickest rate since July...tariffs also continued to impact supply chains and prices at year end. Average lead times for the delivery of inputs lengthened to a solid degree amid customs delays, especially in relation to US imports. Due to tariffs, firms in some instances reported sourcing inputs from suppliers based in countries outside of the US, which also led to a deterioration of delivery times."

- And this maintained a floor on prices: "Meanwhile, input price inflation picked up slightly, therefore remaining marked overall (albeit still below levels typically seen in 2025). Firms noted that metals like steel had increased in price, and tariffs were generally reported to be inflationary. Wherever possible, higher input costs were passed on to firms in the form of increased output charges. Overall, selling price inflation picked up to a six-month high."

- Tuesday's release of Services/Composite PMIs and Wednesday's Ivey PMI will help round out the December growth picture.

- October's -0.34% M/M growth rate for GDP by Industry with just +0.1% expected for November puts Q4 tracking to post a sharp slowdown in GDP growth from Q3's 2.6% Q/Q SAAR - probably below the 1.0% projected by the Bank of Canada.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

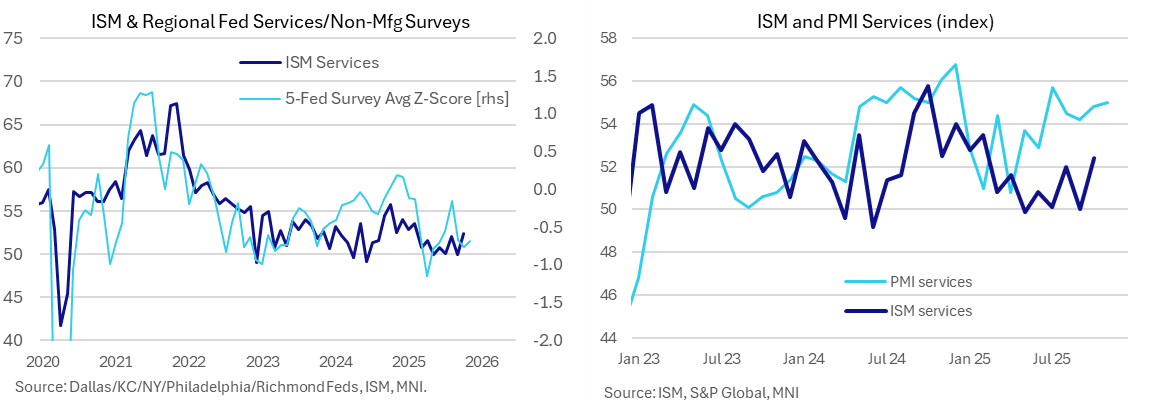

US OUTLOOK/OPINION: ISM Services Seen Dipping In Nov Despite Optimistic PMI

Dec-03 14:35

- Released at 1000ET, the ISM services index is seen dipping to 52.0 in November to only modestly ease after a stronger than expected eight-month high of 52.4 in October.

- The index has ranged between 49.9 (May) and 53.5 (Feb) so far this year and more recently oscillated between 50 and 52 handles since July.

- Alternate indicators on balance point to some limited upside but that's mainly from the services PMI, which is typically much more optimistic and by notably differing amounts month-to-month.

- S&P Global PMI: upside. The services PMI ticked up further to 55.0 in the flash November release from 54.8 in October for a fresh high since July and before that Dec 2024. As such, it points to both directional and level upside risk but, just as with the manufacturing survey, it has been far more optimistic than its ISM counterpart. It has averaged 3.4pts higher than ISM services in the latest six months but with a range of 2.1-5.6pts which means its predictive power should be viewed cautiously.

- Regional Fed surveys: neutral. The average of five regional Fed service/non-manufacturing surveys ticked down from -12.2 to -12.5 whilst the z-score inched higher from -0.8 to -0.7. The latter points to a small directional improvement on the month but is starting from a relatively lower level - see chart. The combination sees little conviction on risks to the ISM reading this month.

- There's no consensus for new orders although we'll watch them closely to see if it's possible to decipher a trend after what has been a particularly noisy few months (56.2 in Oct, technically a twelve-month high, after 50.4 in Sep and 56.0 in Aug). The flash PMI (link) encouragingly noted the "largest rise in new business so far this year" along with its "strongest output gain since July".

- The employment index meanwhile steadily increased in Sept and Oct to 48.2, still contractionary but a five-month high nevertheless. With no more BLS payrolls data due before the Dec 9-10 FOMC meeting, that should carry greater weight than usual.

EQUITIES: US Cash Opening calls

Dec-03 14:27

SPX: 6,818.5 (-0.2%); DJIA: 47,409 (-0.1%/-65pts); NDX: 25,445.4 (-0.4%) .

STIR: Effective Fed Funds Rate

Dec-03 14:20

FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.89% (+0.00), volume: $91B

- Daily Overnight Bank Funding Rate: 3.89% (+0.00), volume: $160B

Repo Reference Rates from earlier:

- Secured Overnight Financing Rate (SOFR): 4.01% (-0.11), volume: $3.407T

- Broad General Collateral Rate (BGCR): 3.96% (-0.11), volume: $1.310T

- Tri-Party General Collateral Rate (TCR): 3.96% (-0.11), volume: $1.276T

- (rate, volume levels reflect prior session)

Trending Top

Mar-27 20:13