MEXICO: Analyst Comments Following Mexico Economic Activity Data

- As a reminder on Wednesday, Mexico posted firmer than expected economic activity for August, coming in at +0.57% M/m. Focus now turns to both trade balance figures for September and the preliminary read of Q3 GDP scheduled next week. Below are some analyst comments following the release:

- *BBVA: Mexico’s economic activity grew by 0.6% MoM in August, an improvement on the preliminary estimate. The difference is explained by the preliminary data not including agricultural activities, which expanded by 14.5% and contributed 0.4% to overall growth. Looking ahead, BBVA anticipate that 3Q25 GDP growth (to be released next week) remained stagnant and that economic activity for 2025 will be relatively weak, with a recovery likely in 2026.

- *Itaú: The August activity data indicate that the economy experienced a negative performance in the Q3, with the QoQ/SAAR at -0.7% due to declines in industry and agriculture sectors. The carry-over for 2025 is 0.3%. Since this behaviour was expected, Itaú maintain their forecast of 0.6% GDP growth in 2025, although they remain cautious about potential unexpected shocks in the fourth quarter caused by hurricanes that affected the southern and central parts of the country in October. Currently, the damage assessment is still underway.

- *Banorte: Yesterday’s data seem to confirm that 3Q25 will likely be a negative quarter, with next week’s preliminary GDP data expected to show a contraction. Following this, the outlook for the end of the year remains challenging. However, Banorte anticipate a rebound given the strength of services, with a modest additional boost from industry.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

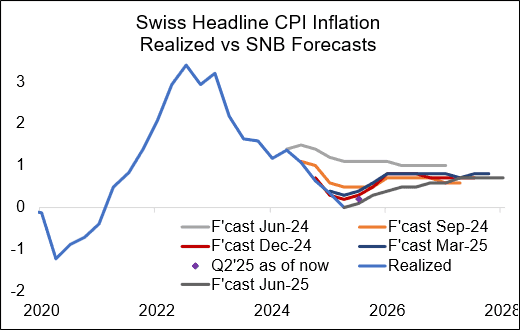

SNB: MNI SNB Preview - September 2025: Avoid Negativity

EXECUTIVE SUMMARY:

- Markets and analysts see a hold at 0.00% at Thursday’s meeting as most likely, with a cut into negative territory appearing improbable given inflation has remained within the SNB’s defined range of price stability for three months now.

- US tariffs at 39% remain of some concern for the Swiss economy leading to downside pressure on GDP estimates but should not move the needle for near-term SNB policy.

- The rates outlook is likely to continue to be characterized by a high bar to further cuts into negative territory, a comment on that may or may not make it into the press statement but will anyways be discussed in the subsequent media conference.

- The SNB’s FX communications paragraph is likely to remain materially unchanged given a limited move in the trade-weighted CHF since the June meeting.

For the first time, additional colour on the governing board decision making process will be the provided four weeks after the meeting with the new meeting summaries.

UN: Trump Posts On UNGA Speech

US President Donald Trump posts on Truth Social: "It was a great honor to speak before the United Nations. I believe the speech was very well received. It focused very much on energy and migration/immigration. I have been talking about this for a long period of time and this Forum, was the absolute best from the standpoint of making these two important statements. I hope everybody gets to watch it! The teleprompter was broken and the escalator came to a sudden hault as we were ridding up to the podium, but both of those events probably made the speech more interesting than it would have been otherwise. It is always an honor to speak at the United Nations, even if, their equipment is somewhat faulty. Make America Great Again!"

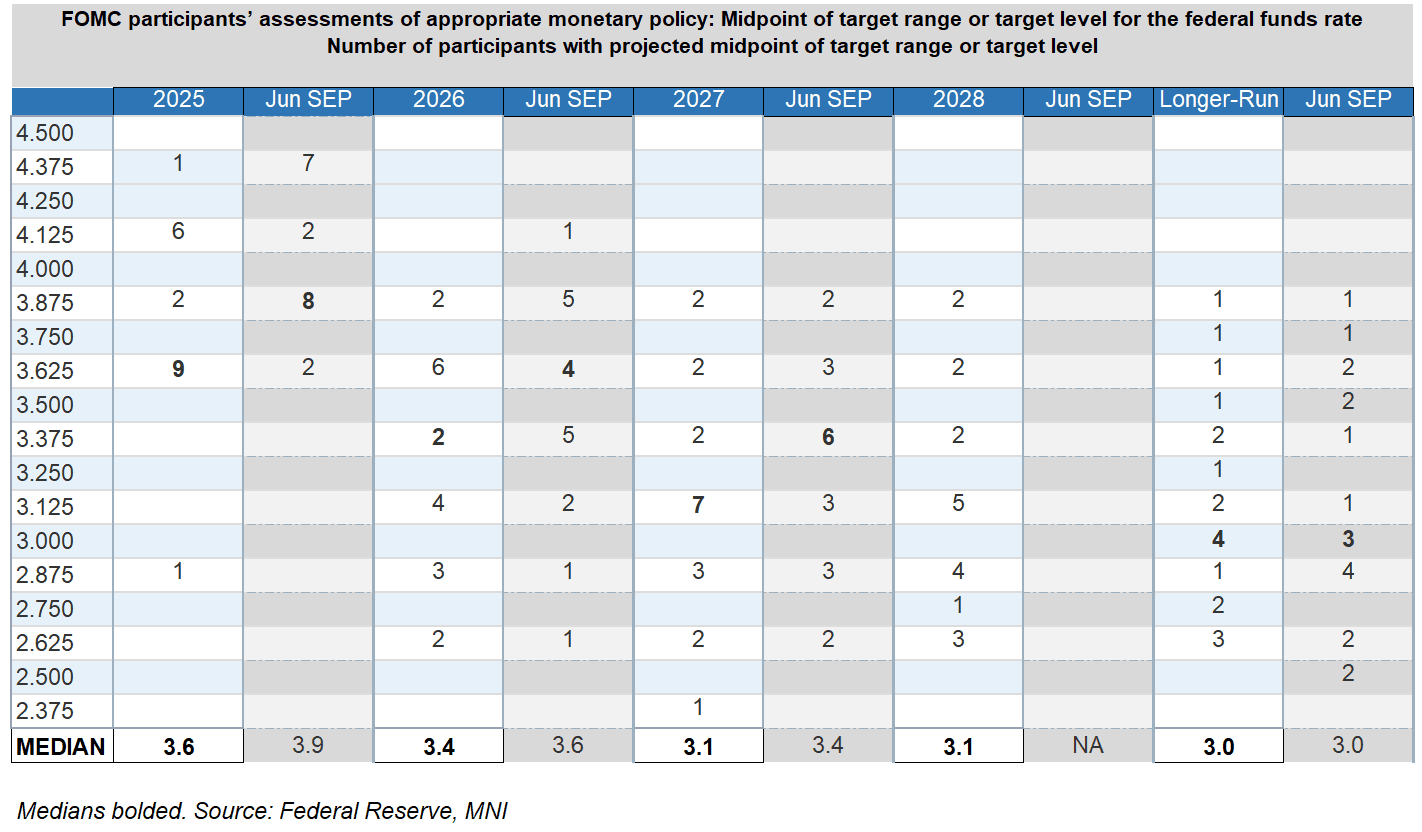

FED: Atlanta Fed Bostic's Longer-Run Dot Suggests Limited Impetus To Cut Further

Atlanta Fed President Bostic added some reflections on the economy and rates in a podcast recording Tuesday morning. Recall that in an interview published in the Wall Street Journal Monday he confirmed he maintained his view for just 1 rate cut in 2025, which makes him among the 7 most hawkish members on the Committee in terms of 2025 rates, with 6 of 19 members writing in 4.1% end-year Fed funds in the Dot Plot.

- His comments on neutral rates suggest that beyond this year, he only sees 3 or 4 more cuts in the cycle. He said Tuesday that "I have in my head that we are starting to see [longer-run neutral] rise. I think 3.1% is in the ballpark. Right now I'm at one and a quarter (in real terms)". Added to 2% inflation, this implies he's at 3.25% on the longer-run dot - and is the only one on the Committee at that level as of September (the median is 3.00%), and has moved up since the last projection since there was nobody at 3.25% in June. That said, it's consistent with what he said in early 2025 (probably in the 3% to 3.5% range) so maybe it's only just ticked up from 3.125%.

- Bostic acknowledges risks to the labor market but notes that it's still very much a low hiring, low firing environment: "The labor markets are very difficult to interpret today because ... the population supply issue is very present. ... I've been hearing from our businesses for many months that we are seeing more cautionary buying or more cautionary behavior so that the demand for product is actually shrinking a little bit. But the overarching story that we're hearing from businesses is, I'm not going to hire anyone, but I'm not going to hire anyone either. There's enough uncertainty in the economy that I don't want to find myself shorthanded, because people remember how hard it was to find quality workers during the pandemic. That's kind of where we stand."

- He adds: "Teasing all this out is a really, really hard thing. But one thing that is definitely sure for me is the sentiment around the risks to employment have gone up a lot and they are, for many, comparable to the risks to inflation. And that is creating some tension in terms of what the right policy should be."

- He emphasizes that it'll be important to observe consumer behavior when it comes to assessing sustained inflation pressures from tariffs: "I think not having been at target for over four and a half years, we definitely need to be concerned about it... there's been a lot of discussion and debate about whether one would expect that tariffs would have an impact on inflation initially. And to date, it's been much more muted, I think, than many expected. But then there is the additional question of will things like tariffs be one time shifts or will they lead to some structural changes. That might mean that we have a different dynamic for inflation. Like all of those things are in play in ways that I think are quite significant. And from our surveys, business leaders are telling us they are definitely feeling the cost pressures. And it is becoming increasingly difficult to prevent those from flowing into prices that are faced by consumers and by their customers. So so I actually think there's still more to come. And... the question will be, does that translate into structural things... I don't think we're at target today. And given that and given that the forces and the pressures are likely to move us away from that in the short and medium term, I really think we need to pay very close attention to the consumer psyche and to what businesses plan based on what they're expecting the future to have."