EM LATAM CREDIT: Alpek: 2Q, Earnings Stabilized – Neutral

(ALPEKA; Baa3neg/BBB-/BBB-)

• Mexican chemical company Alpek earnings dropped YoY, as the previous quarter, but stabilized QoQ. The company was having some success improving profitability 4Q last year with net debt leverage falling to 2.9x so it’s likely the rating agencies give the company more time.

• Volumes fell 7% YoY but were flat sequentially while EBITDA was down YoY by 21% and flat QoQ. The drop in EBITDA was mostly driven by a 31% YoY decline in the polyester division.

• Debt inched up marginally but a drop in trailing twelve months EBITDA led to a higher net debt leverage of 3.5x, up from 3.1x the previous quarter.

• EBITDA guidance was lowered from USD625mn to a range of USD525-575mn.

• ALPEK 2031s were last quoted T+206bp, unchanged since March 31st and 32bp wider YTD. Moody’s moved their outlook to negative July 14th based on concerns about declining EBITDA and bond spreads moved about 11bp wider since then.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup: Rate Cut Pricing Gains Traction

Surge in two-way SOFR puts and upside Aug 10Y Tsy calls reported Monday as underlying futures rallied initially muted response by Iran to US bombing over the weekend and after dovish comments on potential rate cuts from Fed VC Bowman and Chicago Fed Goolsbee if inflation remains muted. Projected rate cut pricing gains traction vs. this morning's levels (*), Dec at the highest since May 12: Jul'25 at -5.9bp (-3.6bp), Sep'25 at -25.2bp (-19.5bp), Oct'25 at -32.6bp (-40.7bp), Dec'25 at -58.8bp (-49.9bp).

- SOFR Options:

- -10,000 SFRU5 97.50/98.00 call spds, 9.0

- Block, 5,000 SFRQ5 96.00/96.12/96.25/96.37 call condors ref 95.955

- -10,000 SFRU5 95.75/0QU5 96.25 put spds, 0.0 0QU sold over

- -20,000 0QZ5 95.87/96.12/96.25/96.50 put condors, 4.0 vs. 96.865/0.05%

- +16,000 SFRU5 95.62/95.75 put spds, 2.5 ref 95.96/0.14%

- +7,000 0QN5 96.62/96.75 2x1 put spds 1.5 ref 96.795

- -4,000 SFRQ5 95.62/95.75 put spds, 1.125 ref 96.23

- -6,000 SFRV5 95.75/95.87/96.00 put flys, 1.75 ref 96.225

- -7,000 SFRN5 95.75/95.81/95.87 put flys, 1.0 ref 95.95

- -7,000 SFRZ5 put fly strip: 95.56/95.68/95.81, 95.75/95.87/96.00, 96.00/96.12/96.25, collects 4.5

- -10,000 SFRH6 94.62/95.62 put spds, 2.25 ref 96.39

- -5,000 SFRU5 95.81/96.00 call spds 2.75 over 95.62/95.75 put spds

- +6,000 SFRZ5 96.25/96.37/96.50/96.62 call condors, 1.25 ref 96.155

- 2,250 SFRZ5 96.50/96.75/97.00/97.25 call condors ref 96.155

- Block, 2,500 SFRQ5 95.87/96.12/96.37 call trees, 2.5 ref 95.885

- 1,750 0QQ5 96.87/97.37 call spds

- 2,000 SFRU5 96.00/96.25/96.50 call flys ref 95.88

- 2,400 0QQ5 96.37 puts ref 96.69

- Block, 2,500 0QZ5 97.00/97.31 call spds, 8.5 vs. 96.765/0.10%

- Treasury Options:

- Update - over +77,300 TYQ5 112 calls, 28-27 vs 110-29.5/0.26%, appr vol 6.59%

- over 62,900 TYQ5 112.5 calls, 28 last

- over 76,200 TYQ5 113 calls, 21 last

- 4,000 TYQ5 110.5/111.5 put spds,

- 3,300 FVQ5 109/109.75 2x3 call spds ref 108-20.5

- 4,950 FVQ5 109.75 calls, 11.5

- 6,000 TYU5 111 puts, ref 111-17.5

- +32,000 TYQ5 113 calls, 21 ref 111-15.5/0.20, appr 6.68% vol (exp 7/25)

- 17,000 TYQ5 109.5/112.5 strangles

- 1,750 wk4 TY 110.25/111.5 call spds, ref 110-29.5, exp 6/27

- +20,000 TYQ5 112.5 calls, 20 vs. 110-29.5/0.19%, appr 6.71% vol

- -2,000 TYQ5 111 calls, 48 vs. 110-28/0.47%

ELECTRICITY: EU Commission Enables Targeted Industrial Electricity Subsidies

- The EU wants to allow member states to provide targeted subsidies to their energy-intensive industries under certain conditions, Handelsblatt reports.

- An industrial electricity price is currently being planned by the German government - the measure has previously raised questions around compliance with EU law.

- EU Competition Commissioner Teresa Ribera plans to present the CISAF on Wednesday, according to HB.

- Full article here: https://www.handelsblatt.com/politik/international/energie-eu-kommission-ermoeglicht-den-industriestrompreis/100136772.html

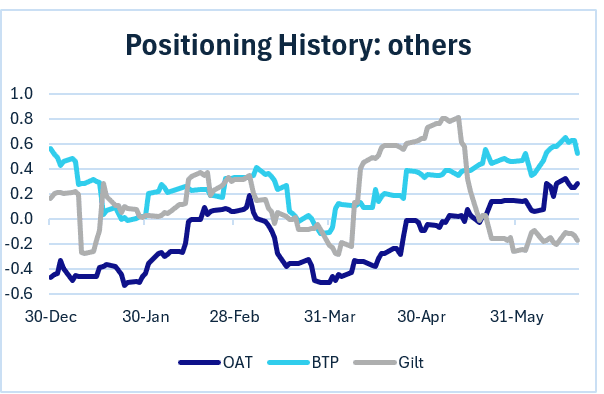

BONDS: Europe Pi: OAT And BTP Longs Pick Up, Gilts Pull Back (2/2)

Elsewhere in European bond futures positioning:

- OAT: OAT has edged to long positioning from flat previously, compared to a brief period in short territory in March/April. The most recent week's trade was indicative of short setting.

- GILT: Gilt structural positioning is in its typical "flat" territory where it has been for most of the year, versus a brief jump to "very long" pre-roll. Some longs were reduced last week.

- BTP: BTP has edged back into "very long" territory vs merely "long" pre-roll (it's typically long/very long). Trade indicative of short setting was seen last week.