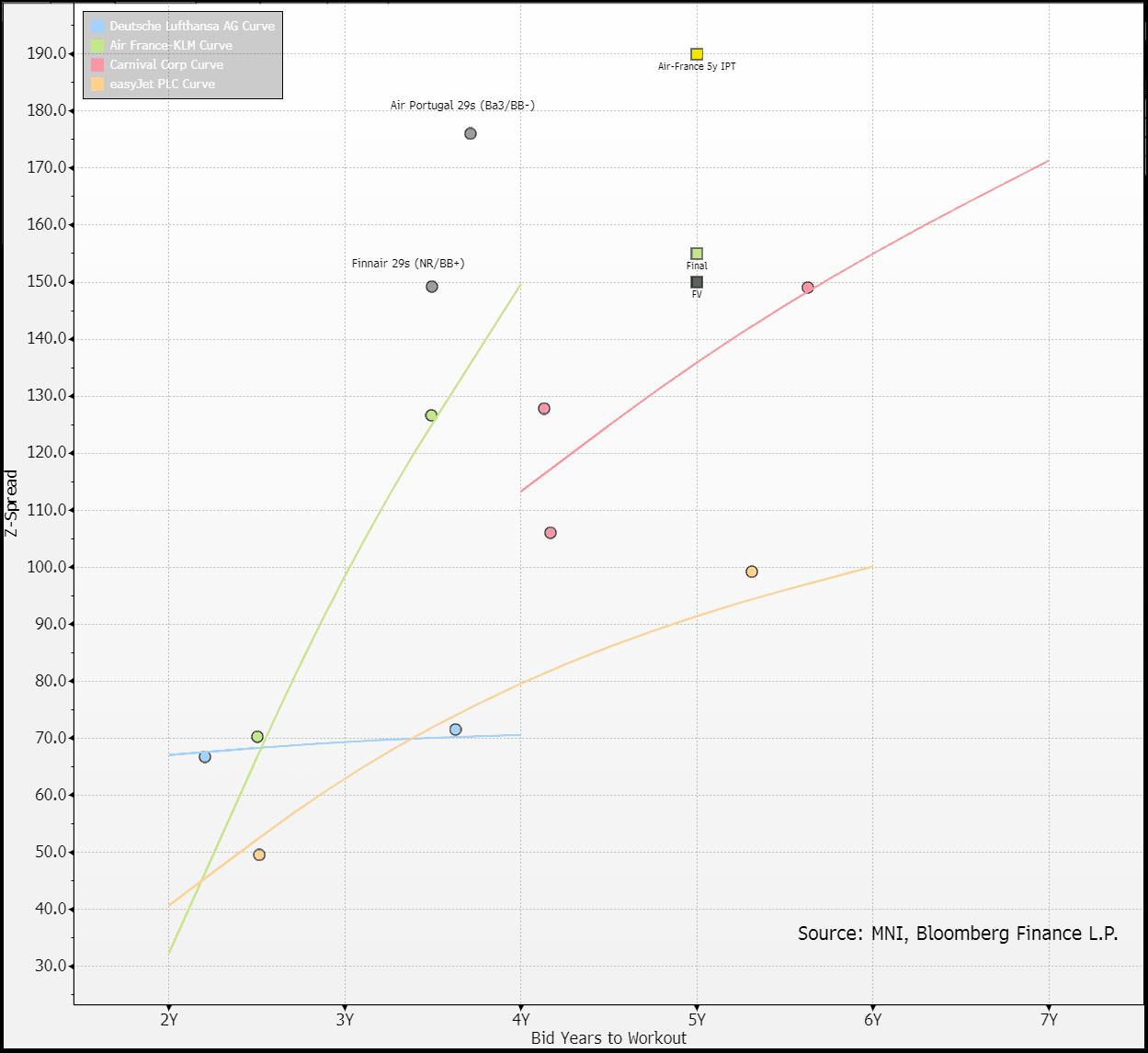

EU TRANSPORTATION: Air France-KLM: FINAL

Aug-28 12:12

(AFFP: NR/BB+/BBB-)

Weak books but it still locks in spreads at near tights.

- WNG €500m 5y +155 vs. FV +150 (5bp NIC)

- -35 from IPT, books > €1.3b

- 3m par call, MWC, CoC, Clean-up (75%)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Repo Reference Rates

Jul-29 12:05

- Secured Overnight Financing Rate (SOFR): 4.36% (+0.00), volume: $2.783T

- Broad General Collateral Rate (BGCR): 4.35% (+0.00), volume: $1.142T

- Tri-Party General Collateral Rate (TCR): 4.35% (+0.00), volume: $1.101T

- (rate, volume levels reflect prior session)

GILT PAOF RESULTS: GBP1.249988bln of the 4.375% Mar-28 Gilt sold.

Jul-29 12:03

- GBP1.250bln have been on offer.

- This leaves GBP42.042bln of the gilt in issue.

US TSYS: Early SOFR/Treasury Option Roundup: SOFR Calls, Blocks

Jul-29 11:50

Option desks report better upside call trade in SOFR & Treasury options overnight, much better SOFR volumes as they segue from earlier put interest. Underlying futures firmer, projected rate cut pricing mostly steady vs. late Monday (*) levels: Jul'25 at -0.8bp, Sep'25 at -16.6bp (-17.4bp), Oct'25 at -28.1bp (-28.2bp), Dec'25 at -44.4bp (-44.5bp). Year end projection well off early July level of appr -65.0bp.

- SOFR OPTIONS

- Block, 20,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 3.25 ref 96.075

- Block, 5,000 SFRQ5 95.81/95.93/96.00 broken call flys, 3.75 ref 95.84

- 1,500 SFRZ5 95.25/95.62/95.75 broken put flys ref 96.075

- 9,200 SFRZ5 96.25/96.50/96.75/97.00 call condors ref 96.05

- 2,000 SFRZ5 96.25/0QZ5 97.18 call spds, 0.5

- +10,300 SFRQ5 95.87/95.93 call spds, 1.25 vs. 95.835/0.15%

- Block, 2,500 SFRV5 96.18/96.43 call spds, 4.75 ref 96.07

- 3,000 SFRU5 96.62/97.25 2x1 put spds, 6.5 ref 96.655

- 2,000 SFRH6 95.87/96.25 2x1 put spds over 96.87/97.12 call spds ref 96.28

- 9,000 SFRV5 96.25/96.31 put spds over 96.50/96.75 call spds, 3.5 net ref 96.07

- +1,200 SFRU5 96.00/96.18, 1.0

- 1,250 SFRU5 95.68/95.75/95.81 put flys, 0.75 ref 95.835

- +1,300 0QV5 96.31 puts, 3.0

- Treasury Options

- 12,000 TUV5 104.12/104.37 call spds ref 103-25.62

- +1,500 wk2 TY 107.75/108.75 put over risk reversals, 0.5 net

- 2,450 TYU5 112/113 call spds, 8 ref 110-25

- 1,000 TUU5 103.75/104.12 call spds, 4.5 vs. 103-18.87/0.20%