AUSSIE BONDS: ACGB Nov-32 Linker Auction Result

The AOFM sell A$100mn of 0.25% 21 Nov 2032, # CAIN416: * Average Yield (%): 2.2373 * High Yield (%)...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: S&P - Pulls Back From 7300 As Headwinds Mount

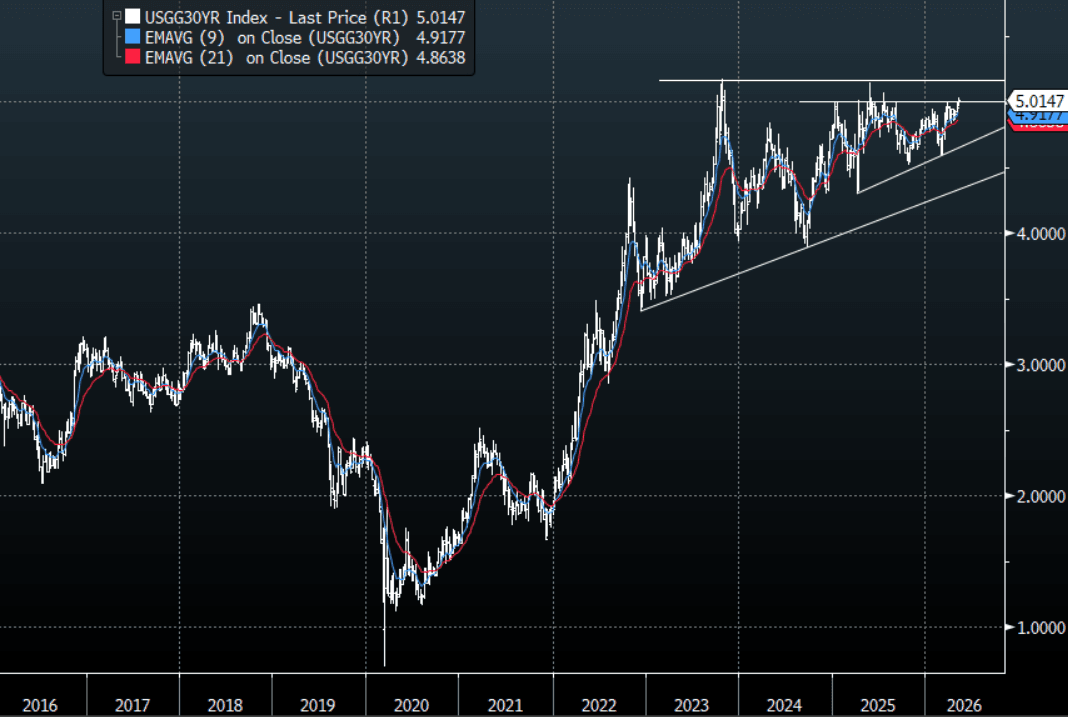

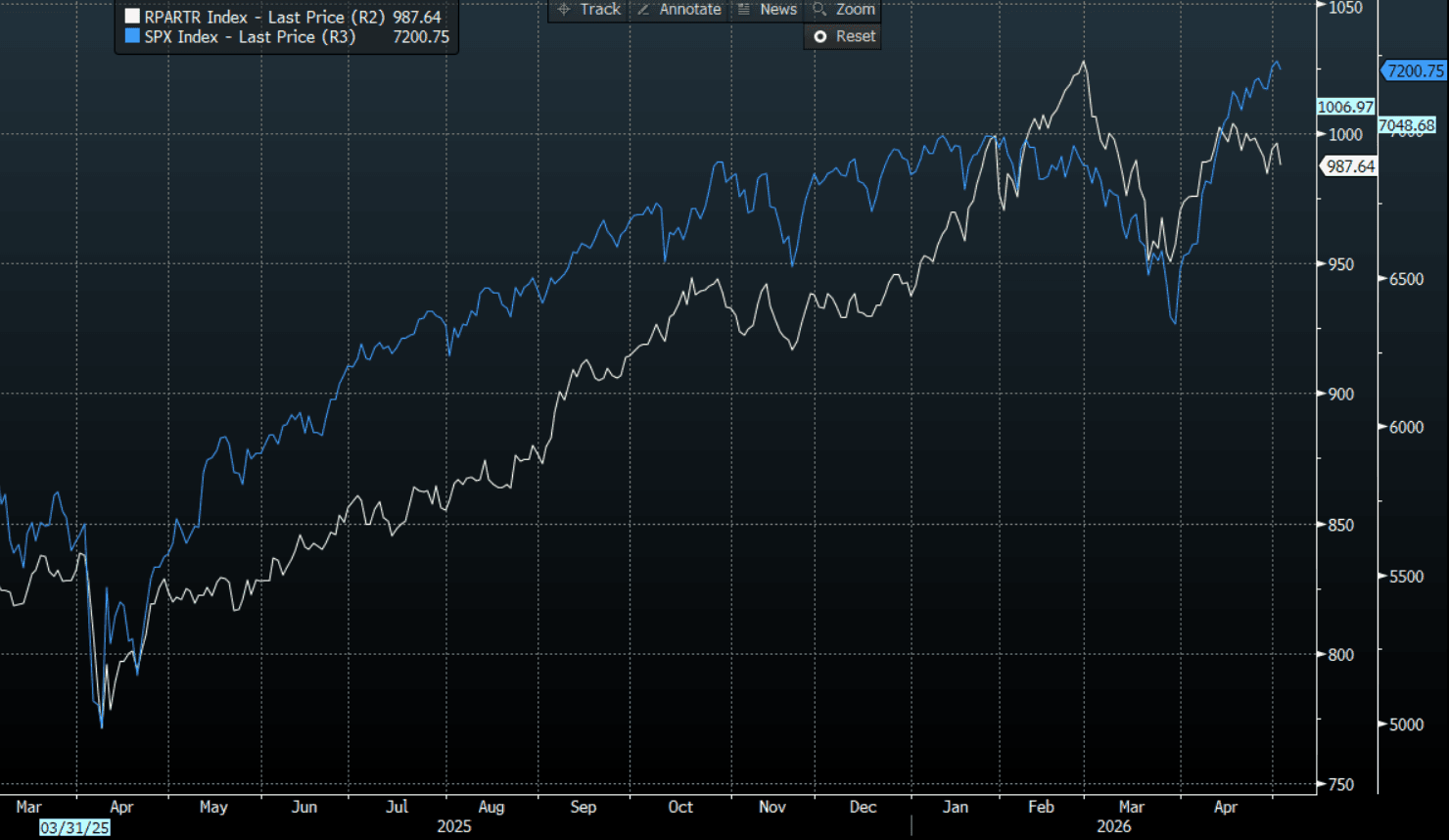

The S&P(ESM6) range overnight was 7199.50 - 7273.50, SPX closed -0.41%, Asia is currently trading around 7229. The S&P(ESM6) retraced toward 7200 as momentum stalled and tensions rose in the Middle-East again. Again there are some clear red flags for risk, Oil is not backing off and the longer the Straits remain closed the more likely it extends higher. The attempted “Project Freedom” indicates the US does not have “all the time in the world” that Trump likes to repeat. The US bond market is selling off, how much longer can Stocks ignore the 30-Year yield above 5% ? A break above the 5.15% area(Fig.1) would be particularly worrying. Risk-Parity continues to show divergence as it looks like it is putting in a lower high, this while the S&P and the Nasdaq break higher to new all-time highs(Fig.2). This morning US futures have had a quiet open, E-minis(S&P) -0.02%%, NQZ5 -0.02%. On the day, I suspect the market will continue to look at everything through a rose colored lens in the short-term, with dips toward 7100-7150 now potentially being supported. The trend is your friend but prudence dictates you should be aware of the risks beginning to mount.

- Javier Blas on X: “The push to re-open the Strait of Hormuz today, with two US warship crossing it and two US-flagged merchant vessels, signals the White House realises it can not keep waiting for the blockade to force Iran into the negotiation table. "

- Jim Bianco on X: "The 30-year yield is now 8 bps away from a new 18-year high.”

- The Market Ear on X: “Calls are exploding. Shorts are gone.”

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 68 Points

Fig 1: US 30-Year Yield Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Fig 1: S&P Vs Risk-Parity

Source: MNI - Market News/Bloomberg Finance L.P

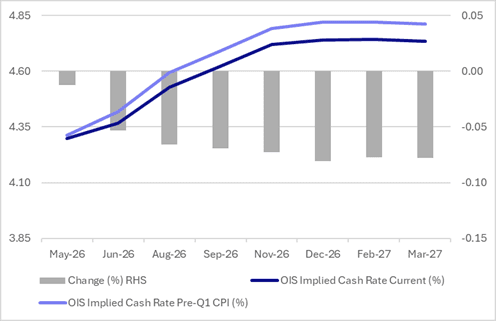

STIR: RBA-Dated OIS Holding Post-CPI Softening Ahead Of RBA Decision

RBA-dated OIS pricing is little changed today but remains 1-8bps softer across meetings versus pre-CPI levels, with late 2026 / early 2027 leading.

- Today’s decision is expected to be closely contested, with another split vote possible, though most analysts still expect a 25bp hike given persistent inflation, excess demand, and early signs of price pass-through from higher costs linked to the Iran war and Strait of Hormuz disruption.

- Despite some argument for a “wait and see” approach, recent commentary from Deputy Governor Hauser suggests limited confidence that policy is restrictive enough, reinforcing the case for further tightening as firms continue to struggle passing on rising costs.

- Nevertheless, OIS pricing continues to show tightening across all meetings, with the probability of a 25bp hike rising from 80% for tomorrow to 172% by August and 254% by December 2026.

- Moreover, the market remains more confident about a May hike than it was ahead of February and March 25bp hikes.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI

RBA: MNI RBA Preview - May 2026: RBA Hike, CPI Too High

Executive Summary:

- The RBA’s 5 May decision is expected to be closely contested, with another split vote possible, though most analysts still expect a 25bp hike given persistent inflation, excess demand, and early signs of price pass-through from higher costs linked to the Iran war and Strait of Hormuz disruption.

- Despite some argument for a “wait and see” approach, recent commentary from Deputy Governor Hauser suggests limited confidence that policy is restrictive enough, reinforcing the case for further tightening as firms continue to struggle passing on rising costs.

- Inflation remains above target on both headline and underlying measures, with trimmed mean around 3.5% and headline inflation rising to about 4%, while input cost pressures (fuel, shipping, labour, and materials) and inflation expectations are all trending higher.

- The labour market remains tight with job growth steady and unemployment stable around 4.2%, though softer consumer confidence and weaker consumption signals are being closely monitored alongside potential fiscal support and terms-of-trade benefits from higher energy prices.

- If the RBA hikes in May, it may then pause to assess incoming data, but more tightening cannot be ruled out; policy decisions will be highly data-dependent, with key releases (jobs, CPI, GDP, wages, Budget) and updated forecasts in August likely shaping the next move.

- See full MNI RBA Preview here