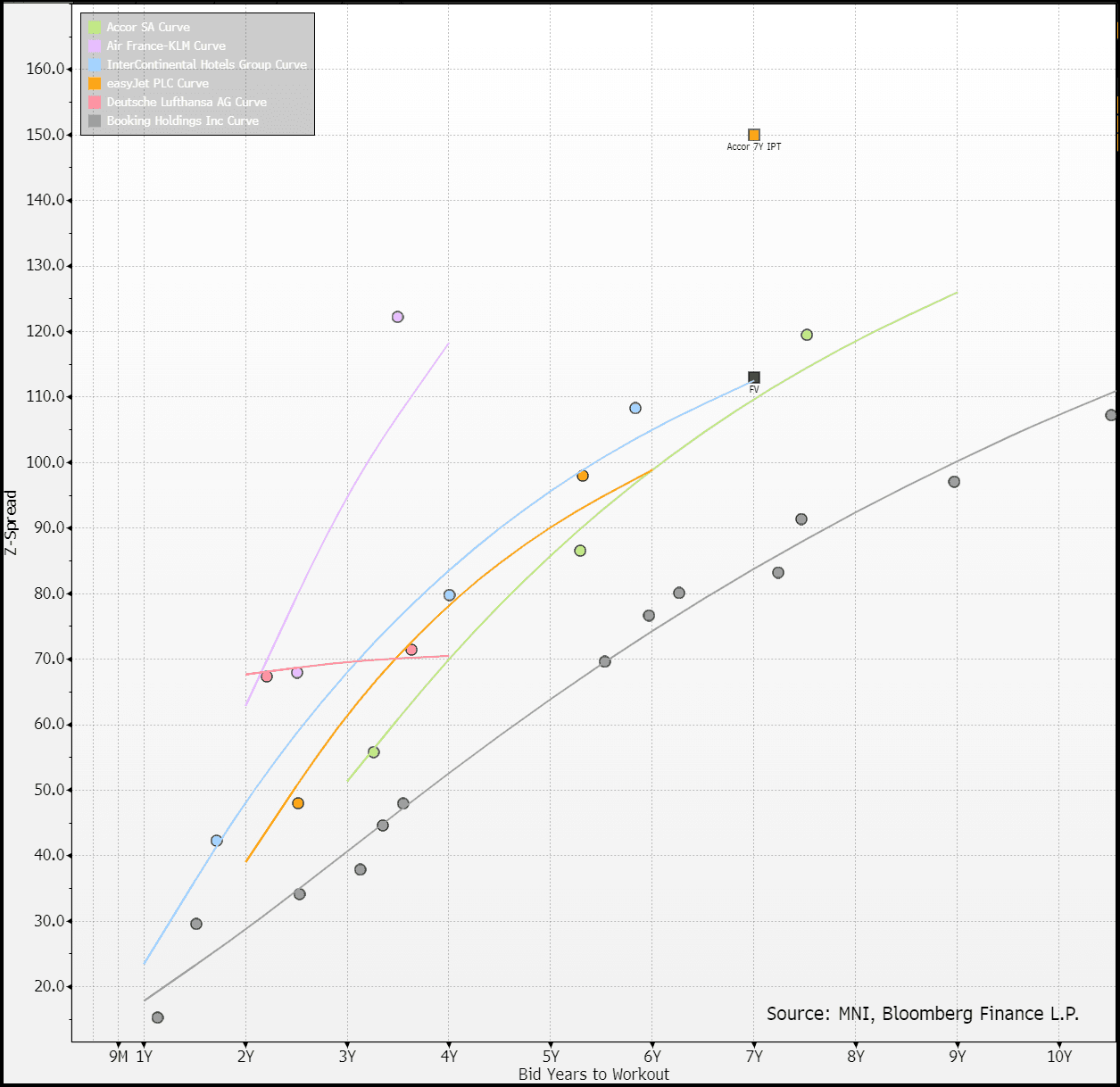

EU TRANSPORTATION: Accor: FV

(ACFP; NR/BBB-/BBB- Pos)

#MNI #Transport

Accor is well inside its leverage target (net 2.2x ex. the hybrids vs. target <3.0x) - equity payouts will push it higher over time. Earnings are fine/growing high-single digit. Both the asset light hotel operators, Accor & IHG, screen relative value vs. other travel names (particularly vs. Airlines). IHG we see as the firmer name on fundamentals - but secondary prices it wider, likely for the US tilt/yankee discount.

- WNG €500m 7y IPT +150-155 vs. FV +113 (-37)

- CoC, MWC, Clean-up (75%)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: /STIR: Goldman Hold Long SONIA Vs Euribor, Eye On QT & Reduced Gilt Risk

Goldman Sachs note that “despite the previous week’s inflationary speed bump, the UK curve outperformed last week, as soggy activity data insulated gilts from bearish price action in other markets. This muted spillover points to the continuing calming in UK-specific risk premium that had been a feature of UK macro assets in recent years. As inflation risk subsides, the half-life of bouts of gilt volatility seems to be shrinking”.

- They go on to suggest that gilts should “get additional support as the BoE slows the pace of QT from October onwards. Although the pace of active sales picks up in our forecasts, we expect the BoE to skew away from long-end sales. As a result, we maintain our constructive GBP vs EUR rates and continue to recommend long SFIZ6 vs. ERZ6”.

EQUITIES: Estoxx outright Put Buyer

SX5E (15th Aug) 4900p, bought for 4.70 in ~8.4k.

US TSY OPTIONS: Weekly TY Option

TY Weekly Option, Friday NFP Expiry:

- TY 111p, bought for '22 in ~5.11k.