ITALY DATA: A Surprise Step Higher In The U/E Rate Off Lows

Jul-02 09:19

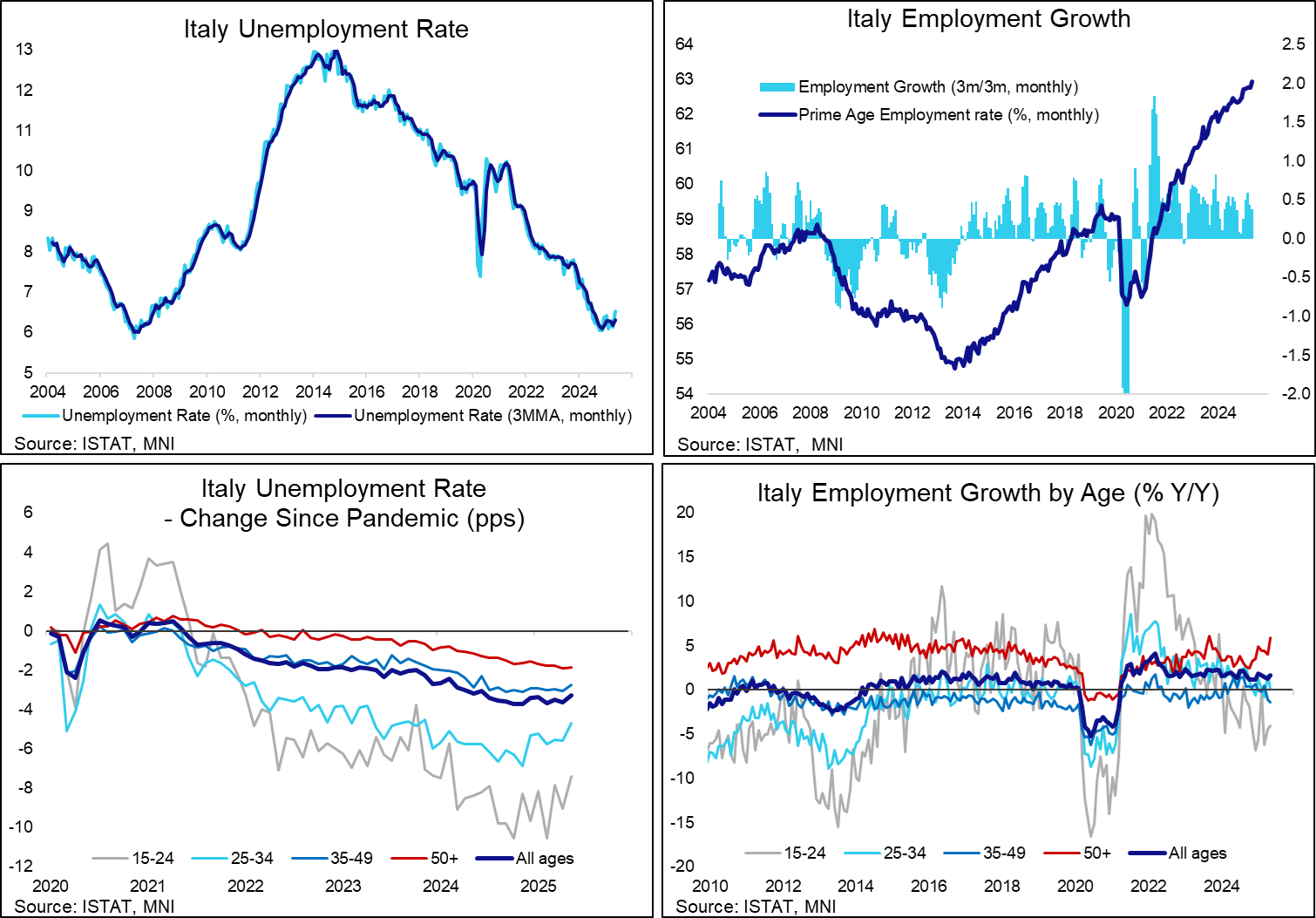

The Italian unemployment surprisingly stepped higher from low levels in May with further signs that younger cohorts have been under pressure in recent months.

- The unemployment rate saw a surprisingly large increase in May to 6.5% (cons 6.0) after an upward revised 6.1% in April (initially 5.9%).

- It leaves it at its highest since Jun 2024 after what are now seen to have been recent lows of 6.05% in Oct and Nov 2024 having last been lower in mid-2007.

- Whilst the absolute magnitude of the move is certainly not unprecedented – it last saw 0.4pp declines in Jul 24, Mar 24 and Dec 23 – it’s a little more notable considering it’s the first increase of that size since Jul 23.

- This is however a series that is prone to surprises: it overshot expectations also by 0.5pp in Dec, before a 0.1pp overshoot in Jan, a 0.4pp undershoot in Feb, an in line Mar and a 0.2pp undershoot in Apr.

- Increases in the u/e rate in May were led by younger cohorts, with 15-24 rising 1.7pps to 21.6% (highest since Feb 24), 25-34 +0.9pps to 10.3% (highest since Nov 23), 35-49 +0.3pps to 5.7% (highest since Jun 24) and 50-64 unchanged at 3.7% (technically 3.65% after 3.64% for a higher rounded).

- As for actual changes, unemployment increased by a large 113k in May, with increases across the board: +28k 15-24, +42k 25-34, +32k 35-49 and +10k 50+.

- Somewhat countering this was a still healthy +80k increase in employment, the strongest rise since January and before that Oct 23. It left overall employment rising 1.7% Y/Y or a similar 0.4% on a 3m/3m basis.

- However, this increase in employment was entirely driven by the 50+ category (+124k) whilst there were declines elsewhere: -6k for 15-24, -29k for 25-34 and -8k for 35-49.

- It further exacerbates a gap between older cohorts, where employment is increasing strongly in part as a factor of an ageing population (50+ employment is 5.9% Y/Y) whilst other ages struggle (-4.1% Y/Y for 15-24, 0.1% Y/Y for 25-34 and -1.3% Y/Y for 35-49).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Bunds Weaken, Curves Steepen On Medium-term Inflation Risks

Jun-02 09:17

- Bund futures have weakened through the course of this morning, currently 39 ticks below Friday’s settlement at 130.82. Initial support is 130.39, the May 29 low. Despite the intraday selloff, a bullish theme remains intact from a technical perspective.

- Markets may be pricing in risks of structurally higher medium-term inflation, seemingly a combination of Trump’s latest tariff threats and higher oil prices following the weekend OPEC+ decision.

- Eurex rolls have been active, with today’s data calendar relatively quiet ahead of risk events later this week.

- The EU will sell up to E6bln of EU-bonds this morning, which may be adding further pressure to core EGB futures in the lead-up to the 1030BST bidding deadline.

- The German curve has bear steepened, with yields 2.5 to 6bps higher. 10-year EGB spreads to Bunds are up to 1bp wider, while EU-bond spreads are 1bp tighter despite the impending supply.

- The Eurozone May manufacturing PMI confirmed flash estimates at 49.4 (vs 49.0 prior), with an upward revision in France offset by a downward revision in Germany. The stronger-than-expected Spanish data was also countered by a slightly softer-than-expected Italian reading.

- This afternoon’s macro focus turns to the US ISM manufacturing reading at 1500BST. A reminder that Eurozone-wide May flash inflation is due tomorrow. There may be downside risks to the 2.0% headline consensus. Thursday's ECB decision (25bp cut to 2.00% expected) headlines this week's regional calendar.

SLOVAKIA AUCTION RESULTS: New 2.50% Jun-29 SlovGB

Jun-02 09:16

| 2.50% Jun-29 SlovGB* | Previous | |

| ISIN | SK4000027397 | SK4000024683 |

| Amount | E817mln | E136mln |

| Avg yield | 2.5000% | 2.2945% |

| Bid-to-cover | 1.56x | 2.20x |

| Avg Price | 100.0000 | 101.8317 |

| Low Price | 100.0000 | 101.8100 |

| Pre-auction mid | 101.936 | |

| Previous date | 19-May-25 |

FOREX: USD Index Bear Trigger Within Range; Next Drivers?

Jun-02 09:14

- Broad dollar weakness Monday has shifted market focus back to the post-election cycle lows for the USD Index at 97.921. A close at today's lows would mark a resumption of the S/T downcycle, narrowing the gap with the bear trigger to just 0.75%. The formation of a bearish engulfing daily candle on Thursday last week adds to the S/T downside focus.

- Today's moves may not only be being driven by the repricing of structurally higher inflation (as covered earlier this morning), but the street consensus for USD is also shifting. This weekend's Morgan Stanley note is garnering plenty of attention - seeing a 9% decline in the USD Index to 91.00 in the next 12 months. This is considerably more bearish than consensus (street looks for ~96.00 at end-Q2'26), but the growing USD net short position suggests these expectations are coming under pressure.

- Derivatives markets often move with a higher beta to spot - so it's a surprise to see a synthetic USD Index risk reversal proving more resilient to the recent sell-off relative to today's price (see below). Should the sell-the-US narrative return in earnest (likely via US equities breaking through the mid-May lows), options positioning could extend lower and provide the needed impetus for the next leg lower in the greenback, compensating for the already-stretched CFTC net position.