JGBS AUCTION: 5-Year Supply Shows Mixed Demand Metrics

Today’s 5-year JGB auction delivered mixed demand signals. The low price was in line with expectations at 100.22, but the bid-to-cover ratio fell to 3.33x from 3.69x, while the tail narrowed to 0.03 from 0.06.

- The result is broadly consistent with the subdued demand seen at this month’s 10-year auction.

- Overall, with an outright yield and the 2s/5s curve near cycle highs, today’s outcome points to generally lacklustre demand conditions.

- In the aftermath, the 5-year sector is little changed in afternoon trading.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Higher Beta FX Struggling, NZD At Fresh Multi Month Lows, JPy Firmer

Risk currencies are underperforming as Tuesday trade unfolds, the softer tone to China/HK equities likely weighing at the margins. Otherwise fresh catalysts are lacking, gold and silver continue to rally, but they may hint at broader mkt risk aversion. USD/JPY is also off session highs (last 152.15/20), helped drive yen crosses lower. We saw another round of verbal FX jawboning from FinMin Kato. The pair was 152.15 in latest dealings, against session highs of 152.10/15.

- AUD/USD is testing under 0.6500(still above Friday lows of 0.6473)

- NZD/USD is lower though, eyeing 0.5700 test, levels last seen in April of this year. (last 0.5710).

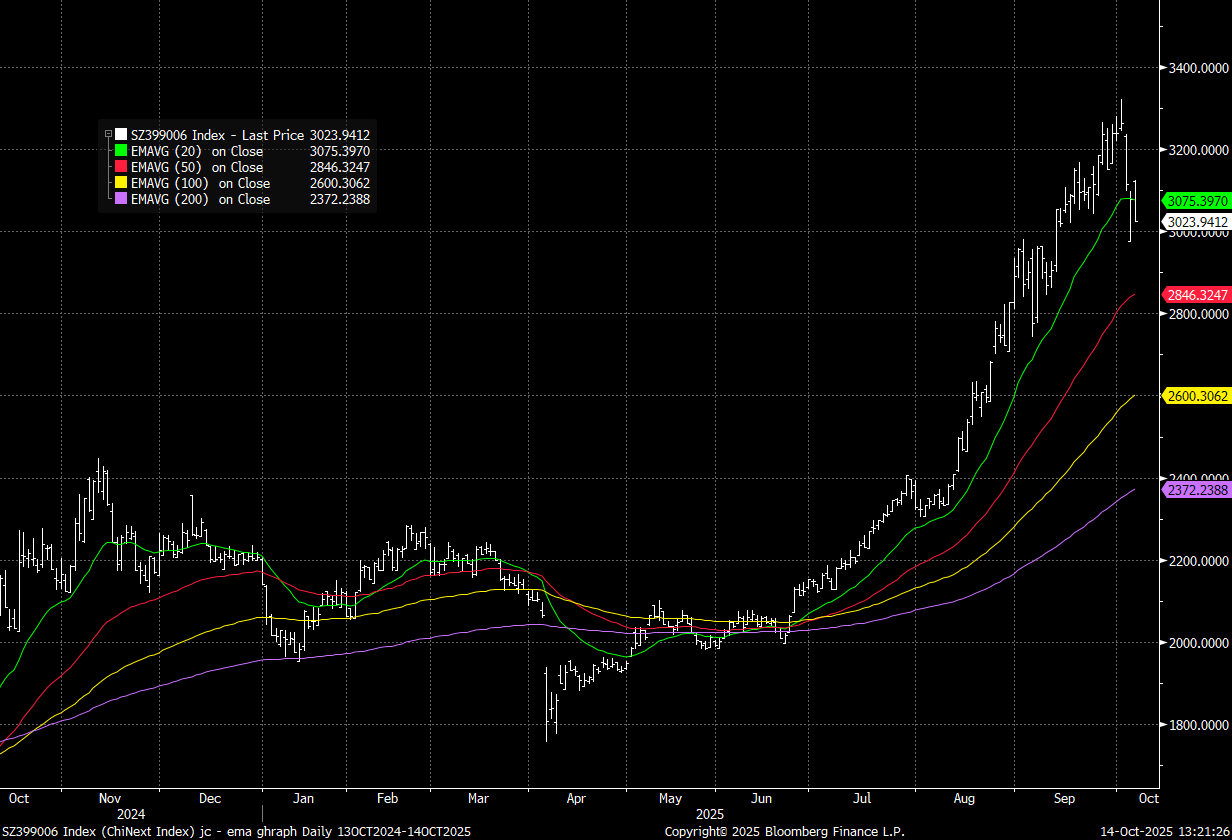

CHINA STOCKS: China/HK Equities Still Struggling Despite Better Global Trends

China/HK equities still struggling to maintain positive momentum, despite the broader gains seen over the past 24hrs in global equities. With sentiment stabilizing amid Trump's softer comments around China. Positioning/valuation concerns (tech headwinds amid export control fears) may also be playing a role. Chipmaker Wingtech also down earlier today after the Dutch government took control of its Nexperia unit.

- The Chinext is plotted in the attached, still above yesterday's intra-session lows, but sub 20-day EMA.

Fig 1: Chinext Equity Index Versus Key

Source: Bloomberg Finance/MNI

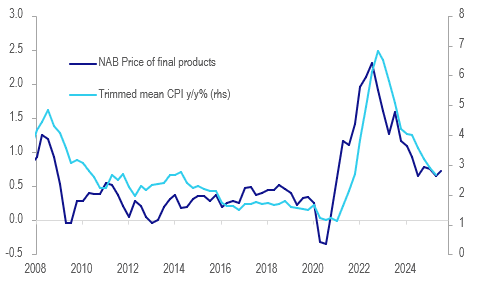

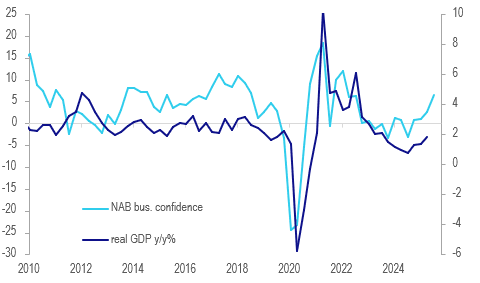

AUSTRALIA DATA: NAB Survey Shows Recovery Continued & Inflation Stable In Q3

The September NAB business survey showed the gradual recovery in the Australian economy continued. Business confidence rose to 7.3 from 4.3 while conditions were similar to August at 7.6. The Q3 averages though were their highest since Q1 2022 and Q2 2024 respectively, suggesting stronger Q3 GDP growth. While the price/cost components were a bit higher in September, they were little changed in Q3 signalling steady inflation. The data are consistent with activity picking up and concerns that disinflation has stalled, and so with the RBA remaining cautious.

Australia NAB business prices vs trimmed mean CPI %

- Given the volatility amongst some of the components of the monthly NAB survey, it is worth looking at Q3 averages to gauge the recovery and inflation picture in the quarter. Its measure of labour demand fell over 2 points to 2.9 in September but the Q3 average was stable at 3.5 consistent with the RBA’s assessment that labour market conditions are “broadly stable”. September jobs print Thursday and a 0.1pp rise in the unemployment rate to 4.3% is forecast.

- The increase in September business conditions was driven by a pickup in trading to 16.0, its highest since November 2023, and profitability to 5.9, best in almost 18 months. However, forward orders declined to -2.3 from +1.1 but while still weak in Q3 improved one point to -0.5.

- Average Q3 labour cost growth was steady at 1.6% 3m/3m while purchase costs moderated 0.1pp to 1.4% (it has held around 1.5% for 6 consecutive quarters). Final product prices rose 0.7% 3m/3m, in line with 2025 average, while retail prices increased 0.8% down from Q2’s 1.0%, lowest since Covid-impacted Q4 2020. Cost, retail and final product price growth rose in September while labour costs fell 0.1pp.

Australia NAB business confidence vs GDP y/y%

Source: MNI - Market News/LSEG