PLN: Zloty Cuts Losses Despite Expectation-Missing Wage Growth Print

EUR/PLN gradually trimmed gains after the release of the latest package of monthly labour market and economic activity data. The pair last deals at 4.2519, around 40 pips higher on the day. In the grand scheme of things, the pair continues to trade sideways since a dynamic rally in early April. A break above Apr 16/Dec 25 highs of 4.3102/4.3114 would represent an important bullish development. Bears keep an eye on May 15 low of 4.2230.

- If related to the data, the reduction of earlier PLN losses would be counterintuitive, considering the net dovish interpretation of the statistics. Nominal wage growth eased to the slowest pace since 1Q21, missing all estimates in the Bloomberg survey, in a sign of abating pressure in the labour market. On the other hand, industrial output grew faster than expected, although the level of production in absolute terms remains below historic highs.

- A regional prosecutor said that a military drone that crashed in Poland likely flew in from the territory of Belarus. The authorities identified the aircraft as a Russian decoy drone and accused Moscow of another provocation. The incident has raised concerns about insufficient radar coverage along the eastern border, which allows low-flying objects to evade interception.

- POLGB curve runs slightly flatter; yields have moved away from earlier highs. The WIG Index has added 0.7% and WIG20 is 0.6% better off.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

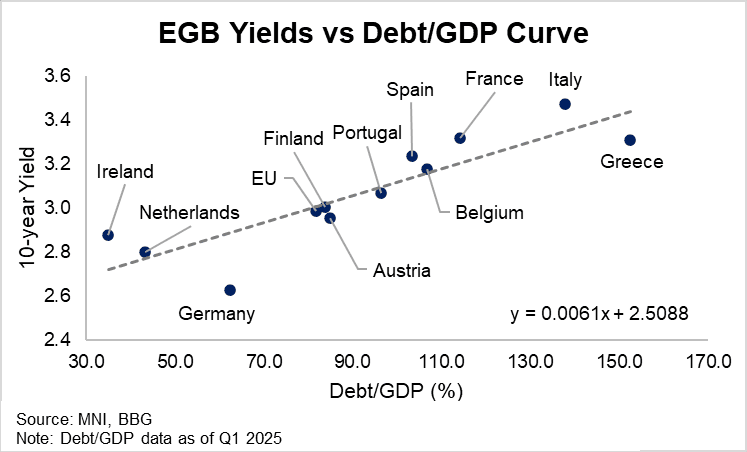

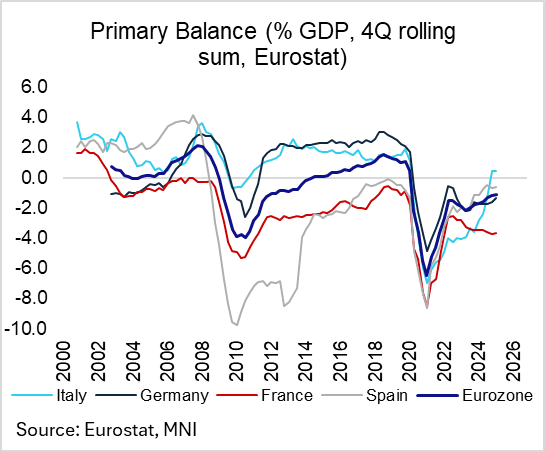

EGBS: Fiscal and Issuance Flow Supportive Of BTP/Obli Outperformance vs OATs

Incorporating yesterday’s Q1 Eurozone fiscal data, a simple chart of debt/GDP to 10-year yields crudely isolates Spanish, French and Italian bonds as cheap (i.e. trading above the linear line of best fit). While well documented French political and fiscal risks continue to warrant a yield premium for OATs, there may be scope for continued relative outperformance of Oblis and BTPs in the coming months.

- We wrote yesterday that while Italian interest expense growth exceeds that of nominal GDP, this is mitigated by the Government’s Q1 primary surplus of 0.4%. Meanwhile, strong Spanish real GDP growth post Covid has kept a healthy gap between interest expense growth and nominal GDP growth. Spain’s primary deficit also narrowed to 0.6% in Q1 from 0.7% in Q4. On the other hand, the difference between French interest expense growth and nominal GDP narrowed a notable 0.8pp to -0.7pp in Q1, a concerning development for the debt/GDP outlook given France's 3.6% primary deficit (despite ongoing attempts at fiscal consolidation).

- The outlook for net issuance also favours Italian and Spanish paper over France: We expect the mid-August Bono/Obli auction to be cancelled, while there is a sizeable E24bln Spanish redemption due on July 30. We also expect the mid-month 3/7/15-50-year BTP auction to be cancelled, with a E13bln BTP redemption then due on August 15. Meanwhile, we expect the two August OAT auctions to go ahead as planned, and there are no French redemptions due until October.

- Elsewhere, 10-year Bund yields trade rich to the debt/GDP curve owing to German paper’s haven/reserve status in the EGB space. Greece’s impressive fiscal consolidation continues to support GGBs, with 10-year yields currently trading just below OATs.

EGB OPTIONS: Bund Z5 Put Spread Buyer

RXZ5 127.00/125.50 put spread, paper pays 35 in 5k.

UK: Chancellor Faces HoL Economic Affairs Committee At 14:30BST

Chancellor of the Exchequer Rachel Reeves will answer questions from the House of Lords Economic Affairs Committee at 14:30BST (09:30ET, 15:30CET). as part of the upper chamber's annual scrutiny session. A live stream can be found here.

- Ministerial evidence sessions with the Economic Affairs committee from the unelected House of Lords tend to garner less market and press attention than those from the House of Commons' Treasury select committee. However, given the pressures facing the chancellor amid rising gov't borrowing and demands from the left of the governing Labour party for tax hikes on tourists and the higher earners, Reeves' session may prove more instructive than is usually the case.

- The committee outlines a lengthy list of potential topics Reeves will face questions on: "whether the government needs to fundamentally rethink its approach to dealing with the UK’s economic ills, the government’s use of rolling debt targets, the UK’s productivity problem, using immigration to mitigate the rising dependency ratio and widespread skills shortages in the economy, whether the rise in the benefits claimant count has been primarily driven by economic incentives rather than a rising prevalence of illness, the fiscal consequences of the government’s concessions to ensure passage of the benefits bill, wealth taxes, the government’s plan to address the growing crisis in long-term adult social care funding."