EM CEEMEA CREDIT: Zambia: IMF’s SLA on Sixth Review of ECF

(ZAMBIN; Caa2pos/CCC+/NR)

- Neutral read for credit sentiment. Zambia reached SLA conclusion on the Sixth Review of the Extended Credit Facility (ECF), subject to Executive Board approval. Of relevance, Zambia is thus expected to receive SDR138.9mn (USD190mn equivalent). As this is the final Review, the total disbursement under the program is expected to reach SDR1.27bn (USD1.7bn equivalent).

- At a glance, the Fund’s statement cites GDP growth projection for ’25 is at 5.2%, on “lower-than-expected mining and wholesale and retail trade”; just last month, the Fund had revised lower ’26 projections to 5.8% on concerns around hydropower generation impairing mining activity, and medium-term projections indicate an average 5.6% for ’26-’31 period.

- Current account deficit projection for ’25 is higher at 2.1%, “driven by broad-based import growth and lower official grants”. A rebound to 1.7% surplus is expected in ’26, and to reach 3.2% by ’30, on expected strength in copper prices and volumes. Gross int’l reserves are on the rise and expectations are for them to reach 4-month of prospective imports by year end.

- Reference Is made to the “open access to the TAZAMA pipeline is rolled out, consistent and transparent application of the guidelines, anchored in private sector participation, will be key to ensuring the reform delivers its expected gains”. This refers to the renewed efforts to modernize and expand with a new pipeline the link from Tanzania’s Dar es Salaam port to Zambia’s Ndola in the Copperbelt, seen as an essential infrastructure project.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Downside EURUSD Momentum Coinciding With WMR Fix

EURUSD seeing downside momentum, coinciding with the WMR fix in the absence of a headline or data driver. Sizeable spike in futures volumes with close to 3000 contracts trading inside 60 seconds.

- The pair is approaching the daily low of 1.1596. Key support meanwhile sits at 1.1469, the Nov 5 low.

OPTIONS: Return of CFTC CoT Could Result in Sizeable Shifts for NZD, AUD, MXN

We anticipate the collection of CFTC collection of positioning data will begin again for the first time in two months at today’s close – meaning this Friday could see the first full CFTC CoT positioning data since September 23rd *.

In the absence of positioning data since then, we blend the front-end of each currency’s risk reversals curve to estimate the changes in positioning since we got the last CFTC update:

- EUR: Small net long of 114,345, or 13% of OI, likely trimmed

- GBP: Very small net short of 1,964, or 1% of OI, likely extended to a larger net short

- JPY: Large net long of 79,500, or 26% of OI, likely broadly unchanged

- AUD: Large net short of 59,590, or 37% of OI, likely extended to larger net short

- NZD: Large net short of 21,120, or 38% of OI, likely short cover, turning positioning closer to flat

- CHF: Large net short of 23,018, or 32% of OI, likely slight short cover

- CAD: Large net short of 114,806, or 54% of OI, likely broadly unchanged

- MXN: Large net long of 83,433, or 57.4% of OI, likely trimmed sharply

Full chartset here: MNIPosiCFTC.pdf

As such, we see the most notable shift in positioning as likely to be in NZD, AUD and MXN given the improvement in NZD options market positioning and the parallel deterioration of AUD and MXN options market positioning.

- * The CFTC have not confirmed this release date, but before the shutdown they did commit to resuming publication “when the federal government operations return to normal”.

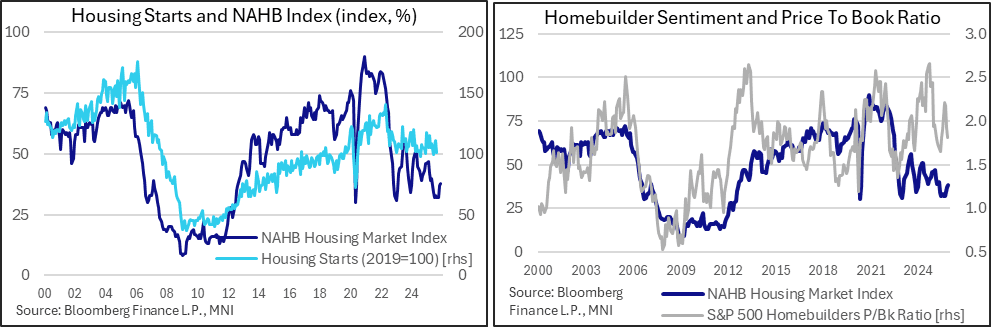

US DATA: Mixed Consolidation Of Improvement In NAHB Homebuilder Sentiment

NAHB homebuilder sentiment firmed marginally in November in a mixed report, building on a larger improvement back in October. The increase over the past two months is likely helped by lower mortgage rates (aided by a reasonable decline in mortgage swap spreads) but the tailwind appears marginal with sentiment still depressed historically.

- The NAHB housing market index was roughly as expected in its November release at 38 (cons 37), slightly extending what had been a 5pt increase to 37 in October.

- It leaves homebuilder sentiment at its highest since April, having improved from the low 30s at what had been close to lows since 2012. Still, it’s comfortably below the 66k averaged in 2019 or a long-term post-2000 average of ~50.

- Latest drivers on the month were mixed, with present sales +2pts to 41 and prospective traffic +1pt to 26, but the outlook for sales in six months’ time -3pts to 51 (albeit after an unusually strong 9pt increase in October).

- Broad sentiment by region was also mixed, with the south (easily the largest for new home sales) and west (second largest) rising 2pts, the midwest falling 2pts and northeast sliding 10pts to also fully reverse an 11pt jump.