ASIA FX: Yen Weakness Drags Majors Lower Over Week

- All major regional currencies finished with losses for the week, as the KRW continues to underperform peers. Jawboning from the Finance Ministry has given the Won a boost today, yet it remains one of the worst regional performers over the last month, weaker by 2% as Yonhap reported "The finance ministry said Thursday it sold US$1.7 billion worth of foreign exchange stabilization bonds. The ministry has issued $1 billion worth of dollar-denominated bonds with a maturity of five years and $700 million worth of yen-denominated bonds with a maturity ranging from two to 10 years. Currency stabilization bonds are designed to raise the money needed by the government to keep foreign exchange rates stable." The plight of USDJPY didn't help the Won as the Yen lost ground by -1.5%, dragging the Won, Peso and TWD with it.

- The Rupiah continues to struggle despite the surprise Central Bank hold on rates this week. In what appeared an attempt to support the Rupiah in their endeavour to reach their target of 16,300 the hold hasn't followed through to FX markets as the Rupiah finishes the week weaker by -0.30% at 16,634 as some forecasters suggest that 17,000 is a real possibility now.

- The Peso fell to it's weakest level versus the USD since February with declines of -0.75% this week. We have broken above 58.60 and are holding there for now.

- FX markets will be paying close attention to US CPI tonight. With next week's cut priced in, an upside surprise could have material impacts on the USD and expectations for monetary policy for the remainder of 2025.

- USD/CNH has edged a little higher but remains sub 7.1300 and is outperforming broader USD gains. Key US-China meetings next week, headlined by the the Trump-XI meeting on Thursday in Seoul (on the sidelines of APEC) are coming into focus. USD/CNH implied vol levels are very low though. Trump remarks this week have continued to express confidence in a deal with China.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (Z5) Trading Closer To Its Recent Lows

- RES 4: 129.50 High Aug 5

- RES 3: 129.44 High Sep 10 and key short-term resistance

- RES 2: 129.13 High Sep 17

- RES 1: 128.56 20-day EMA

- PRICE: 128.23 @ 05:36 BST Sep 24

- SUP 1: 128.01 Low Sep 23

- SUP 2: 127.61 Low Sep 3 and the bear trigger

- SUP 3: 127.46 1.00 proj of the Aug 14 - 15 - 28 price swing

- SUP 4: 127.13 1.236 proj of the Aug 14 - 15 - 28 price swing

Bund futures are unchanged and the contract is trading closer to its recent lows. Key support and the bear trigger lies at 127.61, the Sep 3 low. A break if this level would cancel a recent bullish theme and confirm a continuation of the medium-term bear cycle. For bulls, a reversal higher would refocus attention on key resistance at 129.44, the Sep 10 high. First resistance is at 128.60, the 20-day EMA.

AUSSIE BONDS: Sharply Cheaper After CPI Beat, 0% Chance For Cut Next Week

ACGBs (YM -8.5 & XM -4.0) are weaker and at session cheaps.

- The headline August CPI print was 3.0%y/y, against a 2.9% market consensus and 2.8% July outcome. The trimmed mean was 2.6% y/y, after printing 2.7% in July.

- Today's data will reinforce some caution for the RBA around further easing. It is likely to firm the no-change stance next week (although market pricing has priced in very little chance of a move). The Q3 CPI print is out on Oct 29, with the RBA outcome on Nov 4.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash ACGBs are 4-8bps cheaper on the day, with a flatter curve and the AU-US 10-year yield differential at +20bps.

- The bills strip is -8 to -11 across contracts.

- RBA-dated OIS pricing is sharply firmer across meetings after the data. A 25bp rate cut in September is given a 0% probability, with a cumulative 17bps (22bps pre-data) of easing priced by year-end.

- Tomorrow, the local calendar will see Job Vacancies.

- The AOFM plans to sell A$900mn of the 2.75% 21 November 2029 bond on Friday

- (Bloomberg) NSW TCorp is marketing a Feb 2039 bond that will carry a coupon of 5.25%, according to Westpac.

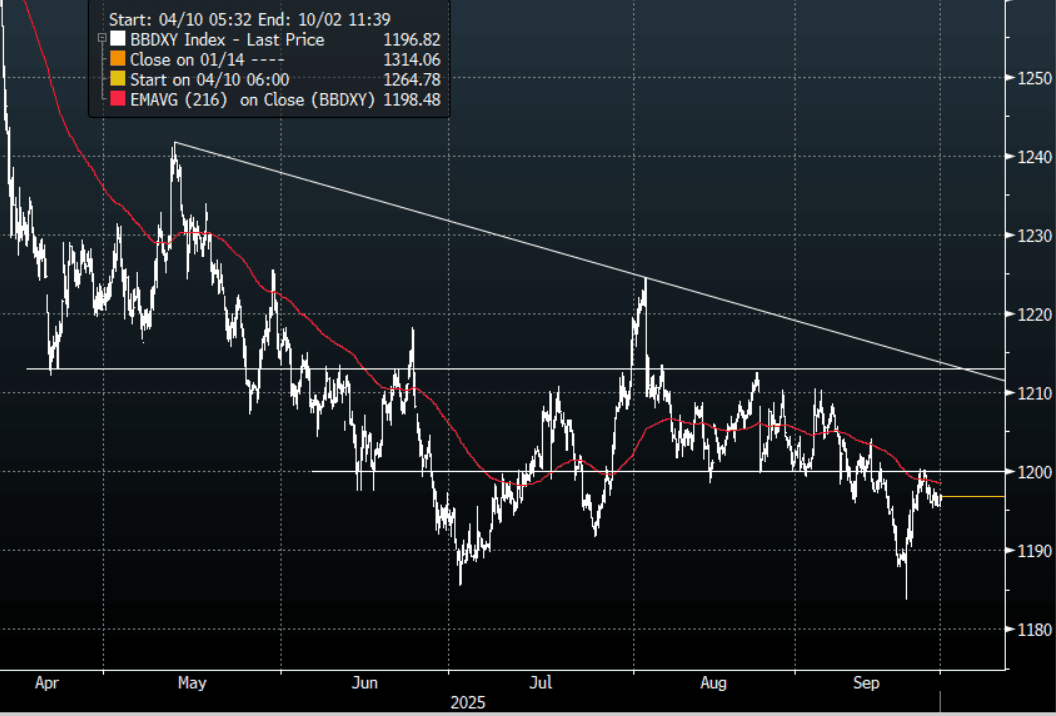

FOREX: Asia FX Wrap - The BBDXY Consolidates Just Below 1200

The BBDXY has had a range of 1195.57 - 1197.02 in the Asia-Pac session; it is currently trading around 1196, +0.10%. The USD has stalled just above 1200 and consolidated in a quiet session overnight. The market is clearly more comfortable selling USD’s but for the moment it lacks any real impetus. Should the market stay below 1200 then the focus will again turn back to the pivotal support back towards the 1180 area, a move back above 1200 might signal a deeper pullback. Bloomberg - “Chinese state-owned banks are selling the yuan in the spot market and offsetting their trades with swaps, putting the brakes on a recent rise in the currency.”

- EUR/USD - Asian range 1.1795 - 1.1819, Asia is currently trading 1.1800. The pair found some demand back towards 1.1700 and is looking to regain momentum higher.

- GBP/USD - Asian range 1.3506 - 1.3528, Asia is currently dealing around 1.3510. The pair rejected the break higher and has moved back into the middle of its recent range. No clear direction for the moment as it consolidates around 1.3500.

- USD/CNH - Asian range 7.1122 - 7.1210, the USD/CNY fix printed 7.1077, Asia is currently dealing around 7.1190. The pair has found demand towards the 7.1000 area and is looking to potentially revert back to the mean. Sellers should be around on bounces while price holds below the 7.2000/2200 area and the PBOC manages the fix lower. A move above 7.2500 is needed to see a test of the USD Shorts.

- Cross asset : SPX +0.05%, Gold $3767, US 10-Year 4.108%, BBDXY 1196, Crude Oil $63.55

- Data/Events : Germany IFO Business Climate, Spain PPI

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P