BRAZIL: XP Expects Worsening Credit Conditions To Continue To Weigh On Activity

Aug-21 13:46

- XP notes that most sectors have lost momentum in recent months, especially those sensitive to credit conditions amid tightening monetary policy. They now estimate that total GDP rose by 0.3% q/q in Q2 (data released Sept 2), below their initial +0.5% estimate, after a strong 1.4% expansion in Q1.

- On the supply side, agriculture is expected to register only a relatively modest decline in Q2, after strong growth in Q1, reflecting the record grain harvest. Industry and services are expected to show moderate growth. On the demand side, domestic absorption remained stable in Q2, as the contraction in investment likely offset increases in household and government consumption. Net exports likely made a positive contribution to q/q growth.

- Looking ahead, XP expects worsening credit conditions to weigh further on domestic activity, although strong income growth should prevent a sharper economic slowdown. They note that the labour market remains robust, and fiscal transfers are still high. They see Q3 growth at 0.5% q/q and full year growth at 2.2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

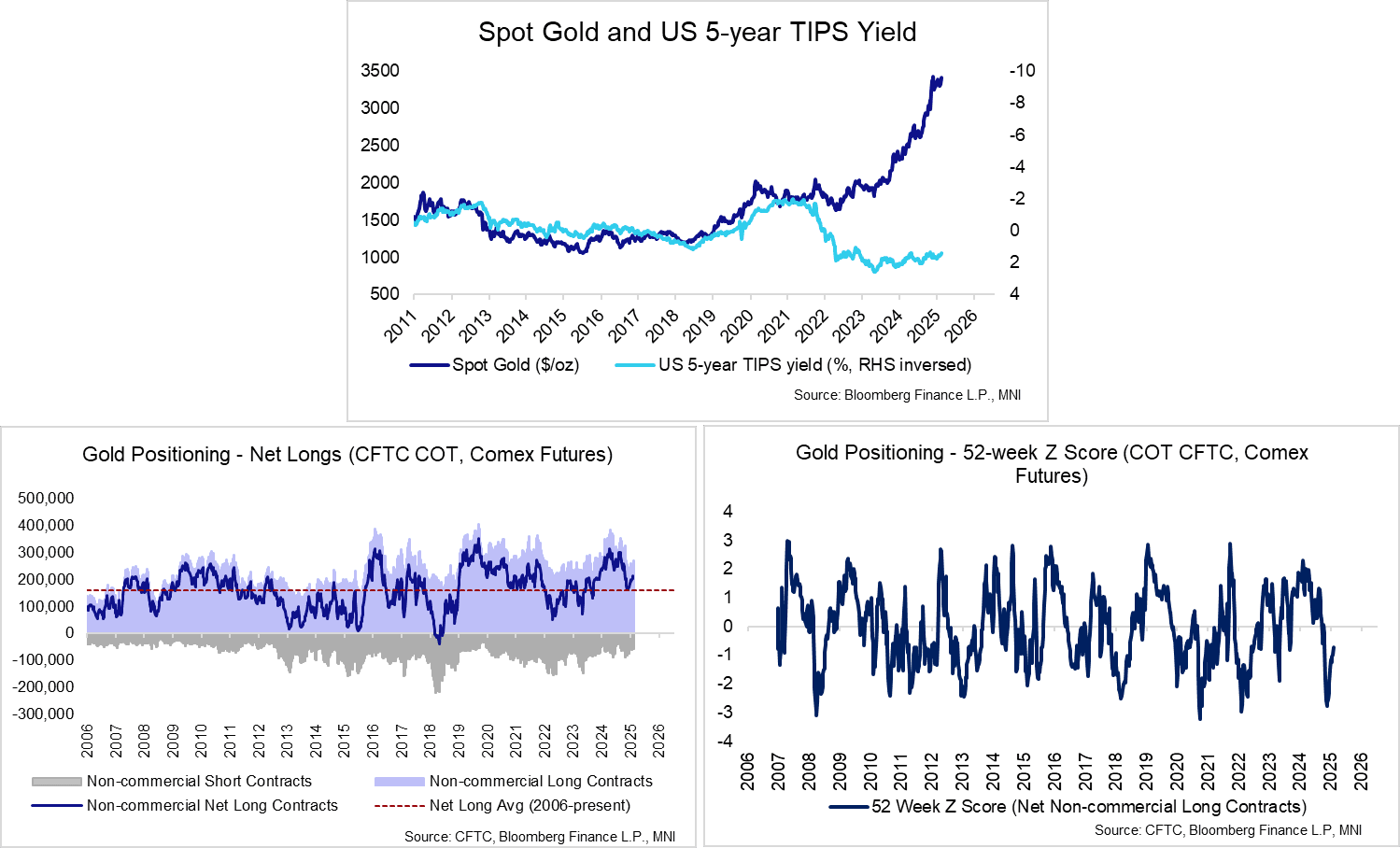

GOLD: Extending Higher Again Without An Obvious Trigger

Jul-22 13:30

Spot gold is building on yesterday’s solid 1.4% rally, extending higher over the last 90 minutes to its highest since June 16. This widens the gap with prior resistance at $3,395.1 (Jun 23 high, which was pierced yesterday), signalling scope for a push towards $3,451.3 (Jun 16 high). Note that moving average studies are in a bull-mode position highlighting a dominant uptrend.

- Today’s 0.4% uptick doesn’t appear to have a clear trigger. US Treasury Secretary Bessent signalled that trade negotiations with China will continue next Monday and Tuesday, with talks moving to a “new level”. Meanwhile, he continued to suggest an ousting of Powell as Fed Chair is unlikely in the short-term. Neither of these comments seem overtly positive for Gold.

- Positioning data as of last Tuesday indicated another 10k increase in net Gold future longs to 213k, the most since the start of April. After stretched long positioning moderated during April, longs have gradually started building back up over the last two months, likely helping underpin price action.

- Looking ahead, focus remains on tariff/Fed-related headline flow from the Trump administration, alongside next week’s heavy macro calendar (including but not limited to the Fed decision, US quarterly refunding, US nonfarm payrolls and the BOJ).

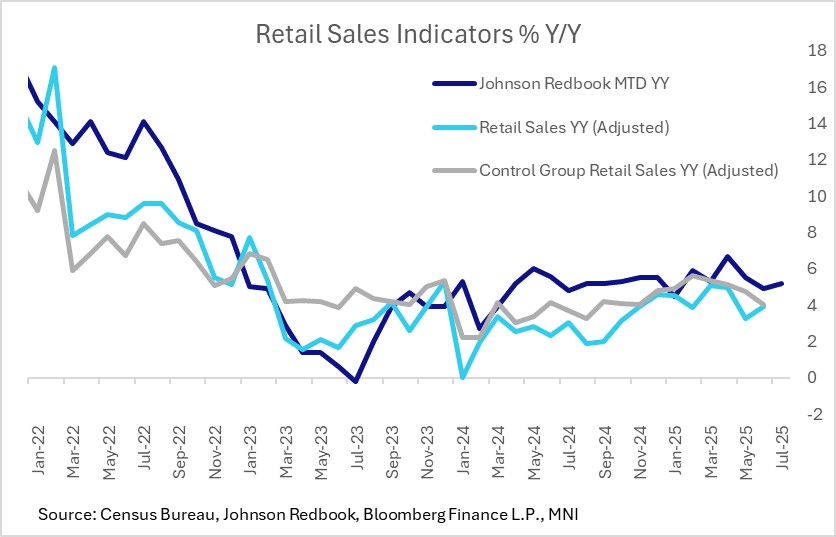

US DATA: Redbook Retail Sales Maintain Steady Growth In Early Q3

Jul-22 13:15

The Johnson Redbook Retail Sales Index continues to post solid gains, rising 5.1% Y/Y in the week ending Jul 19, fairly steady compared with 5.2% the prior week. The month-to-date rise is 5.2% Y/Y (albeit below retailers' targeted 5.7%).

- The report's anecdotal section notes upcoming sales tax holidays in various states, and mentions the impact of tariffs for the first time in several weeks: "As heat waves swept across the country, retailers reported brisk demand for their remaining inventories of hot-weather merchandise. With some school systems starting early, Back-to-School Tax-Free Holidays in many states are approaching quickly this year. Families are increasingly turning to discount stores for value-oriented back-to-school savings in light of rising costs and tariffs."

- Census Bureau retail sales rose 3.9% Y/Y in June, with Control Group sales up 4.0% - mirroring above-typical Redbook sales in their Y/Y peak in Feb-April but slowing slightly since then.

- The Redbook report (which captures 80% of Census Bureau retail sales) suggests fairly steady retail sales growth in the early part of Q3.

US TSYS: Extending Highs

Jul-22 13:10

- Treasury futures have recovered from late overnight lows (initially following Bund rebound), making modest gains across the board at the moment: Sep'25 10Y +2.5 at 111-08.5, yield at 4.3599% (-.0178).

- No policy related comments from Chair Powell at regulatory conference (Fed in policy Blackout since last Friday); Philly Fed non-mfg activity much better than expected.

- Early week support has resulted in a break of the 20-day EMA, strengthening the recovery, and this has exposed resistance at 111-13+, the Jul 10 high. A clear break of this hurdle would highlight a stronger reversal.