BRENT TECHS: (X5) Bear Threat Still Present

- RES 4: $79.16 - 2.618 proj of the Apr 9 - 23 - May 5 price swing

- RES 3: $77.28 - 2.382 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $76.39 - High Jun 23 and a bull trigger

- RES 1: $69.53/71.93 - High Sep 2 / High Jul 30 and a key resistance

- PRICE: $66.98 @ 07:10 BST Sep 10

- SUP 1: $64.50 - Low Jun 30 and a key short-term support

- SUP 2: $60.82 - Low May 30

- SUP 3: $58.37 - Low May 5

- SUP 4: $57.81 - Low Apr 9 and a key support

Recent short-term gains in Brent futures are for now, considered corrective and a bear cycle remains intact. A resumption of weakness would refocus attention on $64.50, the Jun 30 low, where a clear break would confirm a continuation of the bear leg. This would open $60.82, the May 30 low. Key short-term resistance has been defined at $71.93, the Jul 30 high. Clearance of this level would cancel a bear theme.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (U5) Rally Fails to Stick 50-day EMA

- RES 4: 131.33 High Jun 20

- RES 3: 130.85 61.8% retracement of the Jun 13 - Jul 14 bear leg

- RES 2: 130.76 High Jul 22

- RES 1: 130.60 High Aug 5

- PRICE: 129.81 @ 07:07 BST Aug 11

- SUP 1: 128.84 Low Jul 25 and the bear trigger

- SUP 2: 128.40 Low Apr 9

- SUP 3: 128.19 Low Mar 27 (cont)

- SUP 4: 127.83 76.4% retracement of the Mar 11 - Apr 7 bull leg (cont)

Slipping into the Friday close, Bund futures edged back below the 130.00 handle into the close - although the bear trigger and notable support of 128.84 wasn’t tested. The 50-day EMA of 130.12 has been pierced to the upside, but the rally failed to stick. A continuation higher would open 130.76, the Jul 22 high. A hammer candle formation on Jul 25 followed by a bullish engulfing candle on Jul 28 signals a potential reversal.

US TSYS: Yields A Touch Lower In Early Cash Trade

Cash Tsys open around levels indicated by futures after closure during Asia hours owing to the observance of a Japanese holiday.

- Yields ~1.5bp lower across the curve.

- Familiar themes continue to dominate, with Fed succession and clear divides in views surrounding the end of the Russia-Ukraine war front and centre early this week.

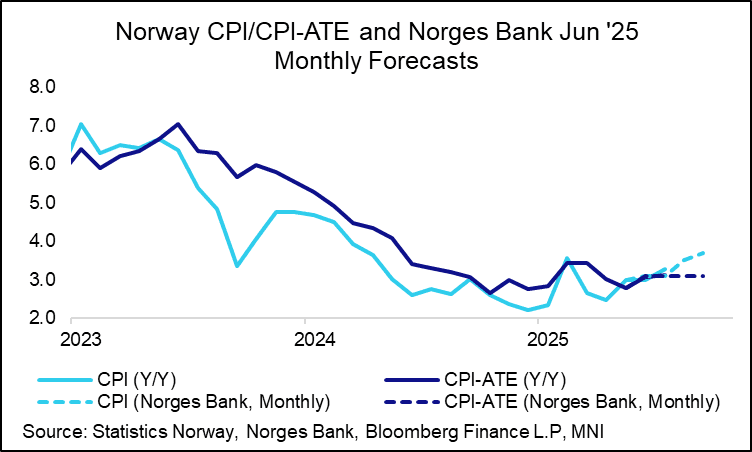

NORWAY: CPI-ATE A Touch Higher Than Expected By Analysts But Inline with Norges

July CPI-ATE at 3.12% Y/Y is higher than expected by consensus (3.0% Y/Y) but in line with Norges Bank's June MPR projections. Headline CPI (3.27% Y/Y) sees a larger upward surprise.

- Norges Bank were already expected to hold rates on Thursday. This reading should cement those expectations.

- More to follow on the details, but at first glance this shouldn't have major impacts on Norges Bank's guidance in August. The broad trend of gradually reducing the policy rate is still intact.

- At the June press conference, Governor Wolden Bache said that the June MPR rate path was consistent with one or two more cuts this year. Analyst calculations on the rate path (and baseline forecasts) leant more towards 2x25bp cuts in September and December.

- There is still another CPI report due before the September 18 decision, alongside Q2 GDP, another Regional Network Survey, and plenty of labour market data.

- Some modest NOK strength following the release, with NOKSEK up just 10pips to 0.9311. This will likely set the tone for the cross through the session.