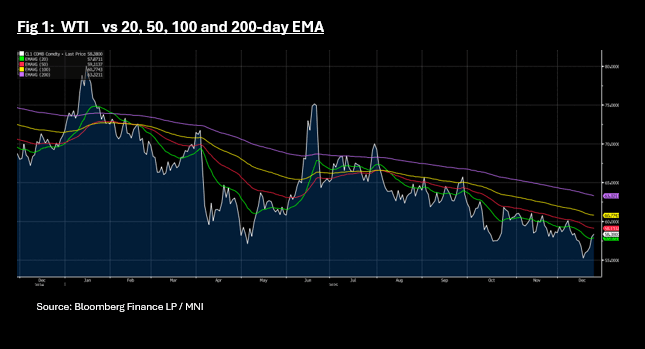

COMMODITIES: WTI Through Key Tech Level; Gold Overbought on RSI

- The US has boarded a Venezuelan oil tanker, is in pursuit of a second tanker by the US coastguard and seized another as Washington ramps up its pressure on Venezuela and the government of Maduro.

- The ongoing threat to Venezuelan shipments, the unresolved conflict in Ukraine and the rising threats from the US of land strikes on drug operations continue to weigh heavy on oil prices.

- A cargo of Russian crude from US-sanctioned Rosneft PJSC has finally been delivered to a Chinese oil terminal after spending three months at sea, ship-tracking data from BBG show.

- WTI finished the US trading day up +0.88% to US$58.46 bbl. The gains takes WTI back to flat for December in what has been a volatile month with ranges from US$55.18 to US$60.14.

- The gains takes WTI back above the 20-day EMA of US$57.87 with topside resistance from the 50-day EMA of US$59.11

- Brent finished up +0.73% at US$62.51 bbl but remains down by -1.1% for December. Brent too has moved above the 20-day EMA of US$61.75 bbl with topside resistance from the 50-day EMA at US$63.00 bbl

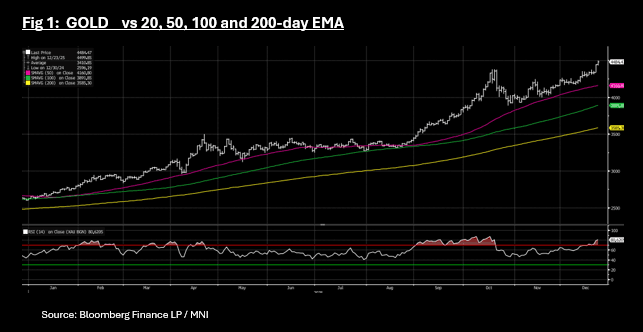

- Gold closed at a new high of US$4,484.47 overnight following gains of +0.92%.

- That leaves gold up +71% year to date in what has been a record breaking year for the precious metal.

- Ongoing volatility from the US trade war has supported gold this year but the key has been the uptick in purchases from key central banks looking to diversify away from the USD.

- Exchange-traded funds added 388,309 troy ounces of gold to their holdings in the last trading session, bringing this year's net purchases to 15.4 million ounces, according to data compiled by Bloomberg. This was the biggest one-day increase since Sept. 26.

- Gold continues to be overbought on the 14-day relative strength index, where it spent most of September and October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBs Steady Start, NZ-US 10yr To Fresh Multi Week Wides, RBNZ on Wed

NZGB yields are little changed in the first part of Monday trade, down only a touch in yield terms at this stage. The 2yr was last 2.58%, while the 10yr was around 4.15%. This comes despite a softer US Tsy yield lead from Friday. Tsy benchmarks fell around 2bps across key parts of the curve, as Fed NY President Williams struck a dovish tone. The NZ-US 10yr spread is around +10bps in early Monday dealings, fresh highs since the first half of Oct. Our fair value estimate for this spread has been suggesting risks of wider spreads in recent sessions.

- "I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions. Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals," Williams Said. Dec Fed pricing shifted to -17bps, from around -9bps prior.

- The trend in the 2yr NZGB has been relatively flat in Nov, holding reasonably close to 2.60%. The 10yr has built some upside momentum, with focus on moves back above 4.20%. Note the 100-day EMA is around 4.25%. The 2/10s curve remains elevated at +157bps.

- The 2yr swap rate (NDSO2) is holding close to 2.41%, within recent ranges. Moves towards the 50-day EMA, which is near 2.46%, have faltered of late. Earlier Nov lows were close to 2.30%.

- The main focus this week will be on the RBNZ decision (on Wednesday). Slightly more than 25bps worth of easing is priced by the market. The data released since its October decision have been consistent with a gradual but soft recovery and close to the RBNZ's August expectations and thus there is unlikely to be another outsized 50bp easing. Updated staff forecasts and a press conference will be included with the November statement. Again attention will be firmly on the OCR path, which shifted materially lower in August. Q3 CPI and unemployment rate printed at the RBNZ's forecast and so are unlikely to show major revisions.

OIL: Ukraine Talks Pressure Oil Prices, Holding Above Bear Trigger Levels

Oil prices fell around 3% last week driven by progress towards a Ukraine peace deal, which the Europeans have said still needs a lot of work. Talks took place over the weekend between the US, Ukraine and Europe. One of Russia’s demands is that it is reintegrated into the global system, which would not only involve rejoining the G8 but also likely include an easing of sanctions which would increase already ample global oil supplies. Tight enforcement of current restrictions is unlikely, with those against Russian oil majors imposed on Friday, while talks are ongoing.

- WTI fell 1.7% to $57.98/bbl to be down 4.3% in November, strengthening a bearish theme. It recovered to around $58.60 before then falling to a low of $57.38, holding above the bear trigger at $55.99. Initial resistance is at $61.84, 24 October high.

- Brent is down 1.4% to $62.51/bbl and 3.5% lower this month. It reached $63.10/bbl before declining to $61.87, above the bear trigger at $59.97. Initial resistance is at $65.95.

- Talks between the US and Ukraine/Europe are due to continue on Monday and if they go well President Zelenskyy could visit the US this week.

- Concerns that the US deal, which favours Russia, was inflexible have been calmed with President Trump saying that it was not final and Zelenskyy posting there are “signals that President Trump’s team hears us”. Europe, Canada and Japan voiced worries that Ukraine would have to give up too much.

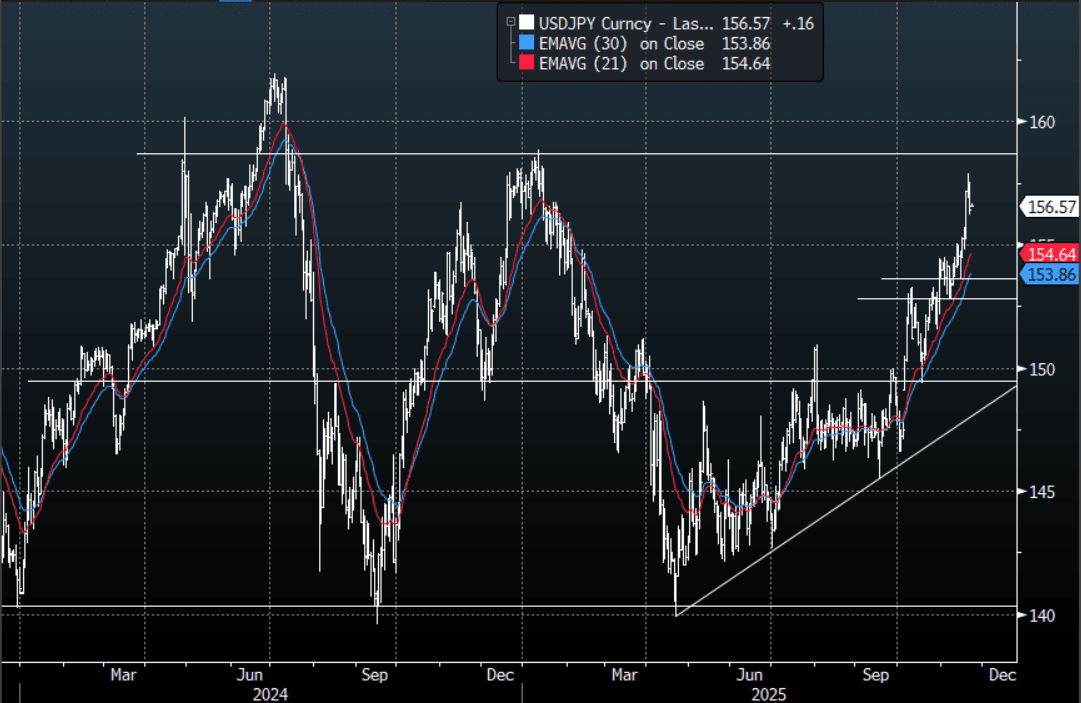

JPY: USD/JPY - Retreats From Highs, Look For Dips To 154-155 To Be Bought

The overnight range was 156.20 - 157.19, Asia is currently trading around 156.60. The pair finally took a breather from its move higher last week. The price action looks pretty clear for now though and Japanese officials would have to do something extraordinary to change the narrative. The path of least resistance is now a higher USD/JPY and I suspect any dips back toward the 154-155 area would be used as buying opportunities. I feel they will have to show some sign of fighting this toward or above 160, but given the current inputs this could potentially go a lot higher than that. It will be interesting when we get the CFTC data back as I suspect real money would only just be starting to turn back to a short Yen position.

- MNI BOJ: Board Member Masu Notes That Rate Hike Is "Getting Closer". BOJ board member Masu tells Nikkei that the decision to raise interest rates is "getting closer". He notes that "I can't say what month it'll be, but in terms of distance, we're close". Masu also provided comments to Jiji in an interview released around an hour ago

- Bloomberg reports that the chief economist at Credit Agricole believes, “Takaichi to be proactive with Yen intervention and will intervene more actively in the foreign exchange market.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.07b),158.00($383m). Upcoming Close Strikes : 153.00($1.17b Nov 26), 154.00{$2.14b Nov 26), 155.00($1.86b Nov 26) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 103 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P