OIL: WTI Regains Ground in Volatile Trading

WTI has regained ground in a day where Trump headlines have sparked volatility. The latest rally appears to be driven by news that the Pentagon has greenlit providing US long-range missiles to Ukraine. Providing Tomahawks would be a sign of the US taking a harder stance against Russia.

- WTI DEC 25 up 0.6% at 60.95$/bbl

- the Pentagon gave the White House the green light to provide Ukraine with long-range Tomahawk missiles after assessing that it would not negatively impact US stockpiles, leaving the final political decision to President Donald Trump, according to US and European officials.

- This follows reports from the FT that the Budapest summit between Trump and Putin was axed after a Russian memo to Washington held firm on the Kremlin’s hardline demand on Ukraine.

- In a call between US Secretary of State Marco Rubio and Russia’s Foreign Minister Sergei Lavrov, Rubio told Trump that Moscow was showing no willingness to negotiate, sources told the FT. Consequently, Trump is said to be “not impressed” with their position.

- While current news implies a worsening of Russia-US relations, it remains to be seen if Trump will agree to send the Tomahawks, which can strike deeper into Russia and put Moscow in range.

- Trump had previously resisted sending Tomahawks amid fears it would ramp up escalation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: September Meeting Deliberations Suggest Some Caution On Future Easing

The deliberations of the September Bank of Canada meeting (link) showed Governing Council's 25bp easing in the policy rate to 2.50% was reasonably straightforward but that future cuts were hardly certain. There was minimal market reaction to the release with much of the information already conveyed in the September post-meeting press conference.

- They discussed either holding rates or cutting by 25bp (which Gov Macklem mentioned at the press conference). Arguing for a hold: still-elevated core inflation, strong consumption growth in Q2, uncertainty over growth vs slack, and potential passthrough of trade disruption to consumer prices, even as "past cuts to the policy rate were still spreading through the economy."

- But in favor of a cut: "First, the economy had weakened, with further softening in the labour market. Second, there was more evidence from recent monthly inflation readings that the upward pressures on core inflation may be easing. Third, the removal of most retaliatory tariffs by Canada also meant there was less upside risk to future inflation. In reviewing all these factors, Governing Council judged that the balance of risks had shifted in favour of cutting the policy rate" and a 25bp reduction "better balance[d] the risks going forward".

- But going forward, "Members agreed that they would continue to emphasize that, with uncertainty still high, they would be guided by their assessment of the risks to inflation. They also agreed they would continue to look over a shorter horizon than usual and take a risk management approach. They recognized there were risks on both sides and agreed they would be ready to respond to new information."

- The deliberations also note that "members expected they would be able to present a baseline projection for growth and inflation in the October Monetary Policy Report" as opposed to the scenario analysis provided in recent MPRs.

- On inflation: "Governing Council members agreed that the latest inflation data indicated that upward momentum in core inflation seen earlier in the year had dissipated. This could be seen most clearly in the three- and six-month rates of inflation in the preferred core measures that had been running above 3% earlier in the year...Members also agreed that the federal government’s recent decision to remove most retaliatory tariffs on imported goods from the United States will mean less upward pressure on the prices of these goods going forward...Members stressed that while the upside risks had diminished, they had not gone away."

- On the labour market: "Overall, members agreed that the labour market had softened" with "job losses concentrated in sectors that rely on US trade. However, employment growth in other parts of the economy had also slowed, as businesses had scaled back their hiring intentions. Wage growth continued to ease. Members were concerned that continued tariffs and ongoing uncertainty about US trade policy could lead to further labour market weakness across the economy."

- On overall growth: "Members agreed that consumption should continue to support growth going forward. Overall, the economy was expected to grow modestly, roughly in line with the current tariff scenario outlined in the July Report...Economic growth could slow further while the adjustment in business investment and jobs plays out...Given the uncertainty surrounding the impact of [] structural changes on demand and supply, members acknowledged it was particularly difficult to assess the amount of slack in the economy."

- On potential fiscal policy changes ahead: "once federal and provincial spending plans are tabled, Governing Council would review the overall macroeconomic impact and incorporate it into their outlook."

SOFR OPTIONS: BLOCK: Dec'25 SOFR Conditional Curve Steepener

- 8,000 0QZ5 97.12/97.50 call spds vs. 3QZ5 96.87/97.25 call spd, 1.5 net - conditional curve steepener at 1334:07ET

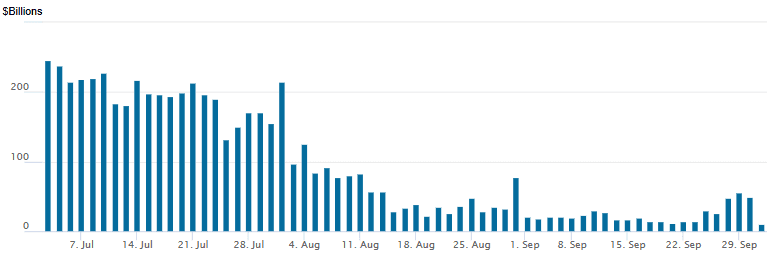

US: FED Reverse Repo Operation - New Multi Year Low

With October underway - RRP usage falls to the lowest level since early April 2021 this afternoon: $10.179B with 15 counterparties, down from $49.071B Tuesday. Compares to the year's high usage of $460.731B on June 30.