OIL: WTI Down Almost 10% In August On Supply Outlook

Oil prices continued trending lower falling a percent as another step was made towards a Ukraine peace deal after the US and Europe agreed on security guarantees and the first steps were taken for Presidents Zelenskyy and Putin to meet. While a truce is a long way off, progress increases expectations that eventually sanctions on Russia will be eased. A setback could see the recent sell off reverse.

- WTI was down 1.4% to $62.51/bbl to be almost 10% lower in August. It reached a low of $62.25, above support at $61.29. Key resistance is at $69.36. It is currently around $62.60.

- Brent fell 1% to $65.95/bbl off the intraday low of $65.61, holding above initial support at $65.01, 13 August low. A clear break of this level would confirm the resumption of the bear leg. Key resistance is at $72.83. The benchmark is down 8% this month.

- The US threatened to increase tariffs on countries who buy Russian crude if there isn’t a peace deal. President Trump announced an extra 25% on India and that China could be next but then he met with Putin. On Tuesday, Treasury Secretary Bessent said that India could still face that punitive tariff.

- Bloomberg reported that there was a US crude inventory draw of 2.4mn barrels last week, more than offsetting last week’s 1.5mn build. Gasoline stocks fell 1mn barrels but distillate rose 500k, according to people familiar with the API data. The official EIA data is out on Wednesday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: LPR Preview

- Today sees the decision on the China Loan Prime Rate (LPR) is important because it serves as a benchmark interest rate for lending in China, influencing both loan and mortgage rates.

- The China Loan Prime Rate (LPR) is important because it serves as a benchmark interest rate for lending in China, influencing both loan and mortgage rates. Changes to the LPR can impact borrowing costs for businesses and consumers, potentially affecting economic growth and financial stability.

- It is unlikely that the Commercial Banks will submit any changes to aid in the preservation of their margins, which have been pressurized. The PBOC has not changed its policy rates since May and given second quarter GDP in line with projections, there appears no immediate need for a cut in rates.

- The PBOC appears to be happy to use the 7-day reverse repo rate as its main tool at present.

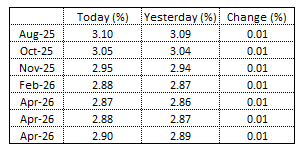

STIR: RBNZ-Dated OIS Slightly Firmer Ahead Of Q2 CPI

RBNZ dated OIS pricing is slightly firmer across meetings ahead of today’s Q2 CPI data.

- 16bps of easing is priced for the August meeting, with a cumulative 30bps by November 2025.

Figure 1: RBNZ Dated OIS Today vs. Prior (%)

Source: Bloomberg Finance LP / MNI

CNH: Recent Ranges Hold, LPRs Seen On Hold, Local Equities Supported

USD/CNH tracks near 7.1790 in early Monday dealings. The pair didn't shift much in Friday's session, with recent ranges still holding. Spot USD/CNY finished up at 7.1746, while the CNY CFETS basket tracker rose for the 6th straight session on Friday, to 96.14, per BBG.

- For USD/CNH spot, we are largely tracking sideways. We haven't tested the 50-day EMA resistance on the upside, which current rests near 7.1925. Earlier July lows were near 7.1500, but more recently, the pair has been supported on dips sub 7.1700.

- A slight downtick in US-CH yield differentials at the end of last week likely helped curb USD/CNH upside. Still, broader yield differential trends will remain dominated by US yield shifts.

- In the equity space, the CSI 300 closed at fresh highs back to Nov last year on Friday. The China to global equity ratio is trending higher, another CNH support point.

- Prospects for a return to previous large scale stimulus measures in the housing sector remain quite low, although broader sell-side consensus put such prospects as fairly low, with China now focused more on quality rather quantity when it comes to housing sector upgrades. Local real estate stocks have no been a key driver of recent aggregate market shifts.

- Today we have the 1yr and 5yr loan prime rate decisions, no change is expected.