SECURITY: WSJ-US Forces Board Sanctioned Venezuela Tanker 'Olina'

The Wall Street Journal reports : https://www.wsj.com/world/americas/u-s-forces-board-fifth-tanker-i...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT PAOF RESULTS: GBP1.124999bln of the 4.75% Oct-35 Gilt sold.

- GBP1.125bln had been on offer.

- This leaves GBP28.624bln of the gilt in issue.

US TSYS: Early SOFR/Treasury Option Roundup: Heavy Volumes Ahead FOMC

Heavier 2-way SOFR & Treasury option flow overnight, SOFR leaning towards downside put structures ahead of today's final FOMC & Sep annc of 2025. Underlying weaker, TYH6 breach of round number support - strengthens a bear theme and signals scope for a move towards 111-19 next a Fibonacci projection. Curves twist flatter ahead of Wed's final FOMC for 2025 (2s10s -1.385 at 57.339, 5s30s -2.452 at 102.931). Projected rate cut pricing eases slightly vs. late Tuesday levels (*): Dec'25 at -23.5bp (-24.1bp), Jan'26 at -29.1bp (-30.2bp), Mar'26 at -35.5bp (-36.6bp), Apr'26 at -39.6bp (-40.1bp).

- SOFR Options:

- Block, 3,750 2QF6 96.12/96.25/96.37/96.50 put condors 2.5 vs. 96.635/0.12%

- 2,000 SFRZ6 96.25/96.50 put spds vs. 97.00/97.50 call spds

- 2,000 0QZ5 96.62/96.75/96.87 put flys ref 96.76

- 2,100 SFRZ5 96.25/96.31 combos vs. 96.76

- 2,000 SFRZ5 96.25 straddles ref 96.265

- 5,500 0QF6 96.50 puts ref 96.395

- +14,000 SFRH6 96.31/96.37/96.43/96.50 put condors, 0.75 ref 96.395

- over +10,000 SFRZ5 96.12 puts, 0.5

- 1,000 SFRU6 99.00/100.00 call spds ref 96.705

- -6,500 SFRH6 96.25 puts, 2.0 ref 96.39/0.20%

- 1,500 SFRZ5 96.18/96.25/96.31 call flys ref 96.2625

- 4,000 SFRM6 96.37/97.00 risk reversals, 0.25 ref 96.58

- Block, 2,500 2QH6 97.37/97.75 call spds 1.0

- over 7,000 0QF6 96.25/96.50 put spds, 2.0-2.5

- +2,250 2QF6 96.12/96.25/96.37/96.50 put condors, 2.5 ref 96.635/0.12%

- Block, 4,000 0QF6 96.43/96.56 put spds, 2.5 vs. 96.74/0.10%

- -8,500 SFRZ6 98.00/99.00 call spds, 3.5

- +7,900 SFRH6 96.18/96.31/96.37 broken put flys, 2.0 ref 96.395

- +2,960 0QF6 96.68 puts, 7.5 ref 96.77/0.37%

- Treasury Options:

- +3,500 TYH6 114.5/115.5 1x2 call spds, 2 ref 111-31

- 4,000 TYH6 110/113.5 strangles ref 111-31.5

- +6,666 wk3 TY 111.25/111.5 put spds, 5 vs. 111-30/0.08%

- -1,500 TYF6 110.5/112.75 2x1 put spds, 54 ref 111-30/0.50%

- -2,000 TYF6/TYG6 113 call spds, 15 ref 112-03.5/0.05%

- +2,000 TYH6 111 puts, 37 vs. 112-01/0.30%

- 1,583 TUH6 103.5/103.75/104 put trees, ref 111-30

- 2,000 TYF6 112/112.5/113/114 broken call condors, 7 ref 112-03.5/0.03%

- +5,000 wk2 111.5 puts, 6

- +4,000 wk2 TY 111.75/112 put spds, 7 ref 111-31.5/0.08%

- +2,000 TYF6 114 calls, 4

- -2,100 FVF6 108/108.25/108.5/108.75 put condors, 3.5 ref 108-27

- -1,400 FVF6 108.5/109 2x1 put spds, 3.5 ref 108-29.5

- 1,650 TYF6 112.5/TYG6 111.5 put spd ref 112-02.5

- -2,850 TYG6 111/113.5 risk reversals, 4 ref 112-03.5

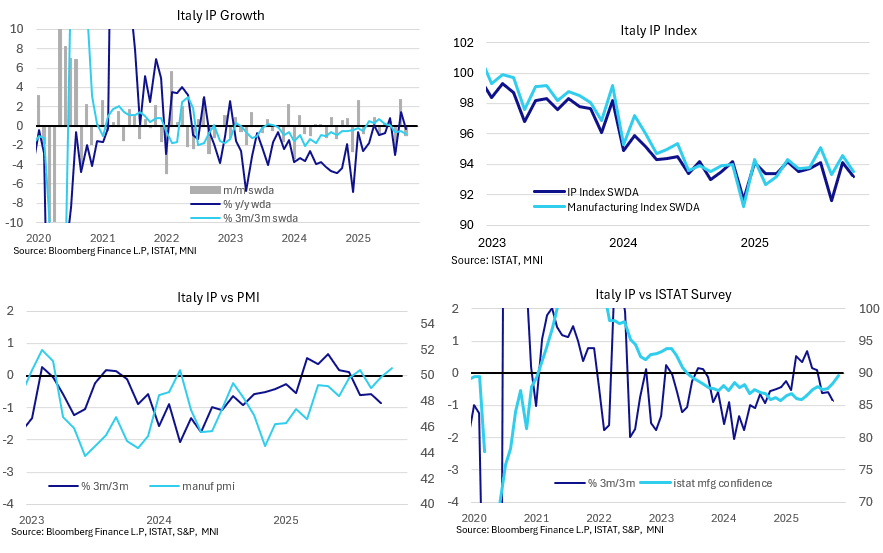

ITALY DATA: Sharper-Than-Expected IP Pullback Contrasts Broader Eurozone Moves

Italy industrial production for October slipped -1.0% M/M (-0.2% cons, 2.7% prior, revised down 0.1ppt) - with a notable downward contribution from transport equipment - for a sharper pullback than anticipated after September's strength. The release contrasts recent strength in German, French and Spanish IP, although recent improvements to Italian business sentiment at least crudely point to some firming ahead.

- The seasonally-adjusted IP index now sits below the YTD average - September's strength was mostly an unwind of August's sharp drop.

- The release points to continued weakness in Italian production, particularly manufacturing, despite some short-lived reversals. This contrasts stronger October IP in Germany, France and Spain, painting a more mixed picture for the Eurozone.

- Transport equipment saw sustained weakness, falling 2.9% M/M (vs -4.6% Sep), with the 3M/3M rate now negative at -1.2%. Most other sectors saw broad reversals of September moves or flat readings.

- Year-on-year, IP fell 0.3% SA, versus a 1.3% Y/Y increase in September (revised down 0.1ppt).

- Y/Y declines are led by manufacture of chemicals (-6.6% Y/Y), textiles (-5.0%), refined petroleum (-4.6%) and transport equipment (-3.5%)

- Y/Y increases are led by mining and quarrying (5.2%), manufacture of metals products excl. machinery (2.7%) and rubber/plastics/non-metals (2.1%).