OIL: White House on Potential New Russia Sanctions

“WHITE HOUSE OFFICIAL: TRUMP HAS MADE NO NEW DECISIONS REGARDING NEW RUSSIAN SANCTIONS AT THIS TIME” RTRS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OAT: Modest Widening Vs. Bunds, Sell-Side Remain Cautious

OAT/Bunds 0.5bp wider at 74bp after registering a multi-month low of ~71.5bp on Thursday.

- Softer European equities and risks to PM Lecornu’s deficit target (4.7%) present widening impulses as National Assembly discussions on the revenue side of the Budget resume this week.

- Passage of the Budget presents the clearest risk to the 70bp mark in the coming weeks, although ongoing structural fiscal issues and political risks continue to limit the scope for spread tightening and promote a degree of caution within the sell-side (only modest scope for spread tightening noted across sell-side notes we have read).

- Goldman Sachs: The market will put more weight on near-term political stability than on the more medium-term cost of the pension freeze, which, given the risks already embedded in OATs, is the right judgement in our view. That said, while recent news is constructive, we note that the budget process is still uncertain, with votes on other parts of the bill to come and the 2026 deficit bottom line still unclear. We thus expect some volatility in the spread in coming weeks but maintain our 70bp forecast for 10-Year OAT/Bund by year-end.

- J.P.Morgan: Despite our base case of the 2026 budget getting eventually approved with no government crisis, we find no political risk premia priced in current level of French spreads as quite optimistic. At the same time, we do not find outright underweights in France attractive as under our base case of French budget approval we do expect 10-Year France-Germany to settle around 70bp, close to current levels. We have been partly hedging our overweight carry exposure with underweights in France to partly express our cautious stance on France and partly to hedge carry exposure against risk-offs coming from global factors.

- Societe Generale: Our view on France remains broadly unchanged from September. The challenge lies in timing, given political unpredictability. We expect stable to wider spreads next year, depending on how political stress evolve. Attention will shift to the 2027 presidential elections from 2H26

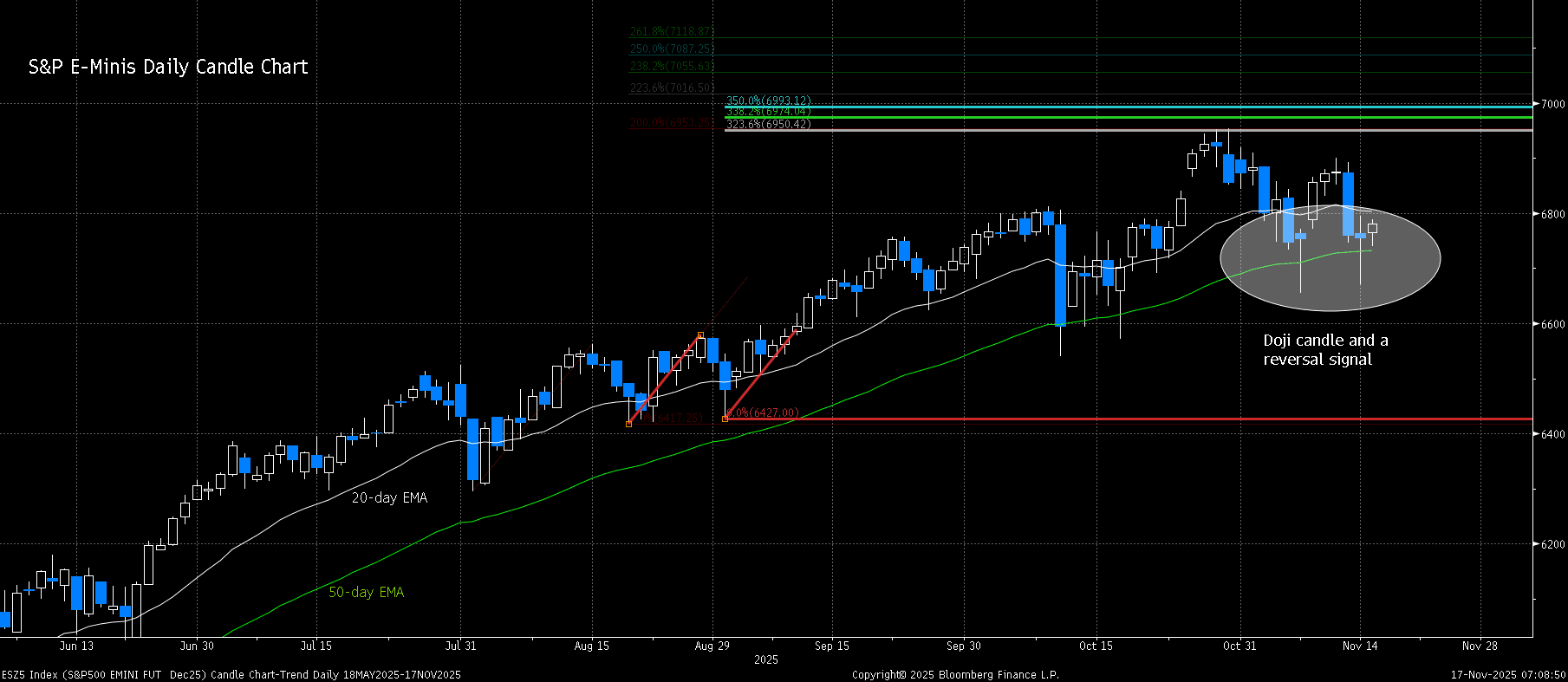

EQUITY TECHS: E-MINI S&P: (Z5) Doji Reversal Candle

- RES 4: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6953.75 High Oct 30 and bull trigger

- RES 2: 6900.50 High Nov 12

- RES 1: 6804.35 20-day EMA

- PRICE: 6750.00 @ 14:35 GMT Nov 17

- SUP 1: 6670.50 Low Nov 14

- SUP 2: 6655.50 Low Nov 7 & key short-term support

- SUP 3: 6571.25 Low Oct 17

- SUP 4: 6540.25 Low Oct 10 and a key support

The trend condition in S&P E-Minis remains bullish and the latest selloff appears corrective - for now. Support at the 50-day EMA, at 6730.32, has been pierced, however, price is once again trading above the average. The next key support to watch is 6655.50, the Nov 7 low. Friday’s price pattern is a doji candle - a reversal signal. Initial firm resistance to watch is 6900.50, the Nov 12 high. A breach of this level would be bullish.

FED: Vice Chair Jefferson: Need To Proceed Slowly On Rates

Fed Vice Chair Jefferson's speech Monday is here. The key quotes are below - he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- But his increasingly cautious tone is echoing the broader Committee; on Nov 7 he said "it makes sense to proceed slowly as we approach the neutral rate", this time he says there is a "need to proceed slowly as we approach the neutral rate."

- Today he says: "I supported last month's decision to reduce our policy rate by 1/4 percentage point. That step was appropriate because I see the balance of risks as having shifted in recent months as downside risks to employment have increased. The current policy stance is still somewhat restrictive, but we have moved it closer to its neutral level that neither restricts nor stimulates the economy. The evolving balance of risks underscores the need to proceed slowly as we approach the neutral rate."

- "Heading into our next meeting, it remains unclear how much official data we will see before then. With respect to the path of the policy rate going forward, I will continue to determine policy based on the incoming data, the evolving outlook, and the balance of risks. I always take a meeting-by-meeting approach. This is an especially prudent approach at this time."