ENERGY: What to Watch: US Rig Counts, ICE Oil COT

Oct-03 07:24

- The latest Baker Hughes rig count data is due for release at 13:00ET. The US oil rig count last week recovered to 424 but the gas rig count edged lower again to 117.

- The ICE commitments of traders reports are scheduled for release after the close today at 18:30BST. During the shutdown of the federal government, Commitments of Traders Reports will not be published. Managed Money net long crude oil positions edged lower in the week to Sep. 23 with a dip in both Brent and WTI. ICE Gasoil net longs dropped slightly from highs.

| Release | Type | Release date | Release Time |

| ICE COT report | weekly | 3-Oct-25 | 18:30 BST |

| Baker Hughes rig count | weekly | 3-Oct-25 | 13:00 ET |

| ICE Gasoil Oct Options Expiry | monthly | 3-Oct-25 | |

| OPEC+8 Meeting re Nov. output | monthly | 5-Oct-25 | |

| Saudi OSPs for Nov | monthly | 5-Oct-25? | |

| API oil data | weekly | 7-Oct-25 | 16:30 ET |

| EIA Short Term Energy Outlook | monthly | 7-Oct-25 | 12:00 ET |

| EIA weekly oil | weekly | 8-Oct-25 | 10:30 ET |

| Genscape crude ARA inventories | weekly | 8-Oct-25 | 09:00 BST |

| BTC Azeri loadings for Nov | monthly | 8-Oct-25 | |

| EIA weekly gas | weekly | 9-Oct-25 | 10:30 ET |

| Insights product ARA inventories | weekly | 9-Oct-25 | |

| Singapore oil product stockpile | weekly | 9-Oct-25 | 08:00 BST |

| Nymex CFTC report | weekly | 10-Oct-25? | 15:30 ET |

| ICE COT report | weekly | 10-Oct-25 | 18:30 BST |

| Baker Hughes rig count | weekly | 10-Oct-25 | 13:00 ET |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: New 14yrs high for the German 30yr Yield

Sep-03 07:24

- A new 14yrs high for the German 30yr Yield, highest since July 2011.

- Next upside level is at 3.45%, and this would equate to 111.16 in UBU5 Today.

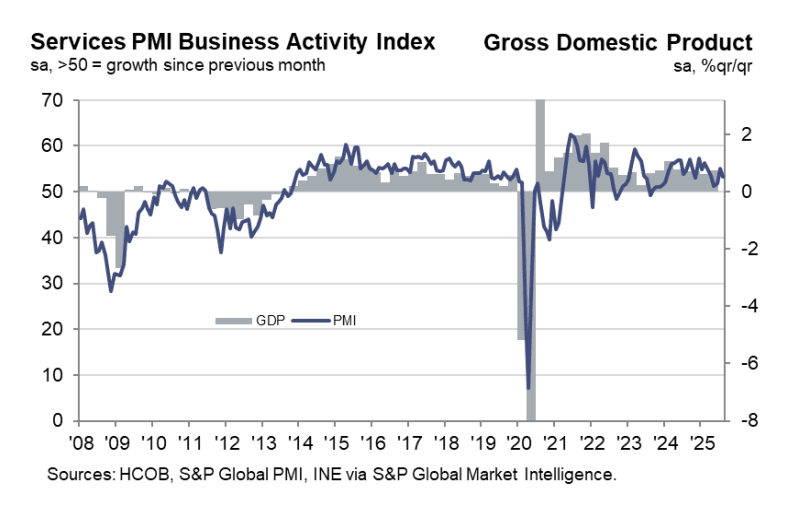

SPAIN DATA: August Services/Composite PMIs: Weaker Than Exp, But Still Solid

Sep-03 07:22

The Spanish services PMI was weaker-than-expected at 53.2 (vs 54.5 cons, 55.1 prior), somewhat disappointing after a stronger-than-expected manufacturing reading on Monday. That left the composite PMI at 53.7 (vs 54.9 cons, 54.7 prior). The composite PMI has nonetheless been above 50 for 24 consecutive months now, underscoring Spain’s position as the Eurozone growth outperformer post Covid.

Details of the PMI were solid from an activity standpoint, but its worth noting another acceleration in inflationary pressures amongst services firms.

Key notes from the release:

- “Higher activity was again principally linked to a rise in new business”…“ Some firms pointed to the release of previously delayed contract agreements as a reason for increased new work. Improved product and service provision also helped to support the marked rise in sales volumes”.

- “Firms were suitably encouraged to take on additional staff in August, largely in response to higher workloads overall”….“ Employment levels have now risen on a continuous basis for just under three years, although growth in August was noticeably slower than July’s four-month high”

- “Prices data showed a pick-up in inflationary pressures. Input prices overall rose to the greatest degree since February with firms pointing to higher supplier charges in general”.

- “Service providers took advantage of a positive demand environment by passing on their increased input costs to clients wherever possible. This helped to underpin the steepest rise in selling prices since April 2024”.

GILTS: Still Under Pressure

Sep-03 07:18

A negative open for gilts despite the recovery from worst levels in Bunds, as weakness in T-notes weighs.

- Futures break yesterday’s low (89.60). Fibonacci support is nearby (89.46), with bears remaining in technical control.

- Yields 2-3bp higher across the curve, steepening theme intact.

- 10s closed at 4.80% yesterday, seeing the first print above that level since late March. January highs (4.921%) present the next upside target there.

- 30s trade through yesterday’s fresh multi-decade high.

- That comes as ongoing fiscal worry, some questions surrounding the future of Chancellor Reeves and the potential Budget date (26 November touted) dominate locally.

- Final UK services PMI data is due today.

- Elsewhere, BoE’s Bailey, Lombardelli, Taylor & Greene will appear in front of the Treasury Select Committee. We will provide a little more on that in due course.

- Note that BoE’s Breeden will speak this morning, although the setting of the address (a “money & payments” conference) may limit scope for comments on monetary policy.