INDONESIA: What Could the New FinMin Mean for the Bond Curve

Sep-11 03:19

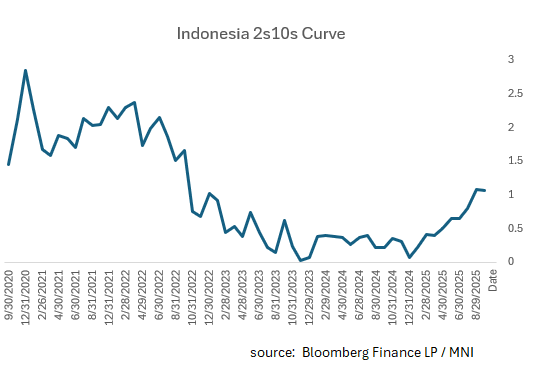

- A yield curve steepens when long-term interest rates rise faster than short-term rates, or when short-term rates fall faster than long-term rates. This typically signals expectations of strong economic growth and potentially higher future inflation, leading investors to demand higher compensation for longer-term bonds due to increased risk. Yet in Indonesia, since the start of the year, inflation has been declining as curves steepened.

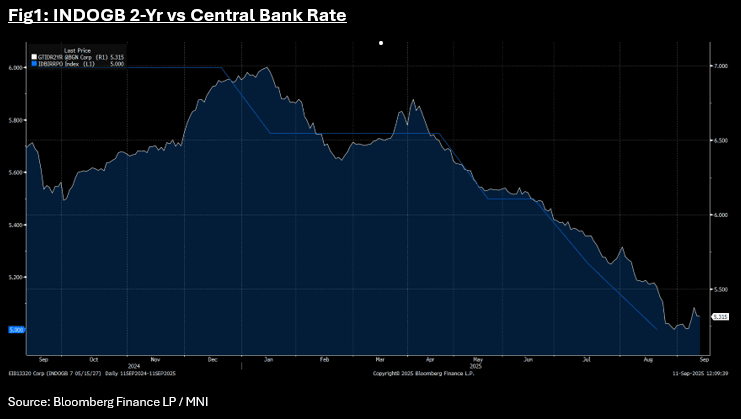

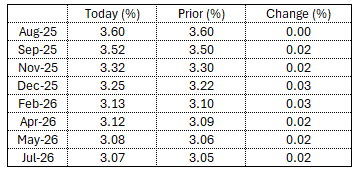

- Since the peak of 6.25% last year, the BI-Rate has been cut 125bps. It is clear that the relationship between the 2-Yr and the BI is strong, with the 2-Yr tracking lower as rates have been cut.

- The 2-Yr yield is lower by -130bps from the January highs, representing a near 1-to-1 correlation whereas the 10-Yr is lower by -85bps.

- The result has been a Bull Steepener which occurs when short-term interest rates fall faster than long-term rates

- Yet as always, we ask ourselves what happens next given the new Finance Minister's appointment and his belief that the country could grow faster than the current 5%.

- Just a few months before being named Indonesia's new finance minister, Purbaya Yudhi Sadewa, raised eyebrows in markets by calling the International Monetary Fund "stupid" for cutting its growth outlook for Southeast Asia's largest economy.

- Mr Purbaya said on Sept 8 it was “not impossible” to grow at 8 per cent and said he would target 6 per cent to 7 per cent in the shorter term, on the back of increased government and private sector participation in the economy.

- From yesterday, via BBG: "- Indonesia’s new finance minister unveiled a roughly $12 billion cash injection to stimulate lending, proving his commitment to President Prabowo Subianto’s growth agenda barely two days into the job." (see this link for more details).

- This points to a strong emphasis from the new finance minister on boosting growth.

- More broadly, what other levers does he have to pull and what should markets be wary of?

- Firstly, Central Bank independence may be challenged. The BI today is regarded as a professional Central Bank, with the tools, people and understanding of how to manage financial markets. Markets expect further cuts from the BI and will be watched closely to see if the new FinMin attempts to exert higher levels of influence over the 'independent' central bank.

- Government bond issuance / higher fiscal deficits. The new FinMin has 'committed' to the the 3% deficit target yet with the current fiscal position not too far away from that target, where does that leave room to supersize growth, especially in an 'increased government' model.

- One of these two forces may need to change from the current pace / pathway; with changes to both representing challenges to the bond market.

- Quite likely, either or bother could result in steeper curves; potentially hitting levels not seen since the COVID period.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBA Dated OIS Slightly Firmer Ahead Of Today’s RBA Decision

Aug-12 02:42

At the time of writing, RBA-dated OIS pricing is slightly firmer on the day across meetings ahead of today’s RBA Policy Decision.

- A 25bp rate cut this week is given a 97% probability, with a cumulative 59bps of easing priced by year-end (based on an effective cash rate of 3.84%).

Figure 1: RBA-Dated OIS – Current Vs. Yesterday

Source: Bloomberg Finance LP / MNI

JGBS: Treading Water Ahead Of Today's US CPI

Aug-12 02:34

At the Tokyo lunch break, JGB futures are weaker but off lows, -8 compared to the settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- (Bloomberg) "Markets remain skeptical that the Bank of Japan will raise rates soon, even as inflation proves sticky. Economists pencil in one hike by year-end, but with the GDP deflator likely to exceed 3%, homegrown inflation is showing signs of entrenchment, adding to the urgency to tighten policy."

- Cash JGBs are showing a modest sell-off across benchmarks, led by the 4-year. The benchmark 10-year yield is 0.4bp higher at 1.495% versus the cycle high of 1.616%.

- Swap rates are little changed. Swap spreads are mixed.

CHINA PRESS: China Stock Market Hit New High This Year

Aug-12 02:30

The benchmark Shanghai Composite Index hit a new high this year, reaching an intra-day peak of 3,650 on Monday, China Securities Journal reported. The turnover in the A-share market exceeded CNY1.8 trillion, with over 4,100 stocks rising and over 80 of them hit the day limit, the newspaper said.

Trending Top

Jun-25 06:23