INDONESIA: Weekly Preview: The Macro, Valuation, Sentiment, Technicals Lens

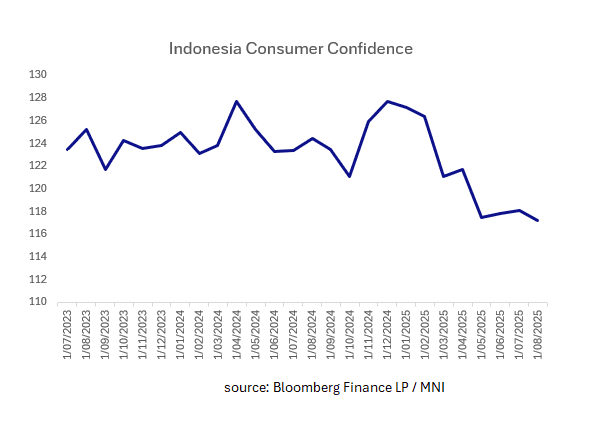

Macro: The key data release from last week was the release of the August Foreign Reserves. Unsurprisingly with the pressures on the currency, we saw a $2bn decline. Other data released was the August consumer confidence which moderated to 117.2, yet remains near all time highs. The capture of this data would have been prior to the uptick in political protests. The headline event for the week is the BI decision on Wednesday. Following a cut of 25bps at the meeting in August, the market expects the BI to remain on hold. The outlier view could be given the political protests of late, a cut could occur to promote calm.

Fig 1: Indonesia Consumer Confidence

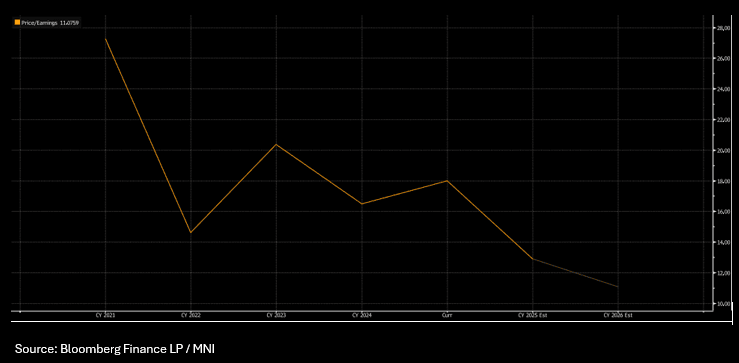

Valuations: The price/earnings for the JCI is difficult to analyze over recent years given the COVID period. At present levels of 18x, it is forecast to trend lower into the year end quite significantly; before heading lower again into 2026. The Relative Strength Index for the IDR points to the Rupiah at fair value where as the 10-Yr government bond is yield nearing 3-Yr lows. The next move for yields will be dictated by the what the BI does next. The 2-Yr bond yield has moved to 40-50bps below the base rate of 5% which may suggest bond managers are thinking that a BI cut could be a possibility.

Fig 2: Jakarta Composite Index Price to Earnings out to 2026.

Sentiment: Sentiment is very challenging in Indonesia after protests intensified last week. The protests were centered on an increase in the housing allowance for parliament members. During the protests the heavy handed behaviour of the police raised further questions as a taxi driver was killed after being hit by a police car. The protests calmed by week's end and the JCI finished the week strongly, but the issues remain.

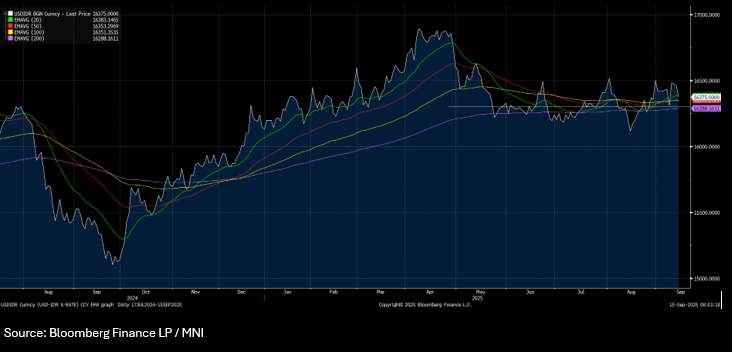

Technicals: Last week's sell off at the beginning of the week, pushed the JCI below the 20-day EMA, only for it to re-assert its position above by week's end. The Rupiah remains delicately poised as it attempts to hold below the 20-day EMA of 16,383 following BI intervention. The BI has stated that their target for USDIDR is 16,300.

Fig 3: USDIDR vs 20, 50, 100 and 200-day EMA

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (U5) Follows Fade in Treasuries

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.710 @ 15:17 BST Aug 15

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures received a boost from the US Treasury rally that followed both the recent poor NFP print as well as Tuesday’s inflation number. While this impact faded into the close of the week, 10-year futures remain toward the top end of the recent range. To the upside, next resistance is at 96.207, a Fibonacci retracement point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

FOREX: USD Index Pinned to 50-dma as Putin Shakes Hands with Trump

- USD slipped against all others Friday, with a poor set of retail sales and Uni of Michigan sentiment numbers meeting a higher-than-expected import price index to further stimulate concerns over a stagflarionary phase in the US economy. The USD Index trades either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting has reached fever pitch. Footage showing the Presidents shaking hands in Alaska has helped ease concerns over a hostile meeting, but it's the outcomes that will matter to markets - particularly as equities hold at alltime highs. Any signs of progress toward a ceasefire would be warmly received by risk sentiment - although both Trump and Putin cautioned against a optimistic outcome in comments to press.

- We noted earlier in the week the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Focus in the coming week shifts to Jackson Hole and Powell's comments on Friday. With the September meeting still in flux - any conviction toward tipping the board toward a rate cut at the next FOMC will be carefully watched, but it's a hawkish outturn that could be more consequential for markets, as OIS prices a near 90% chance of easing on September 17th.

MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- MNI: US TSY TICS NET FLOWS IN JUN +$77.8B

- US TSY TICS NET L-T FLOWS IN JUN +$150.8B