MALAYSIA: Weekly Preview: The Macro, Valuation, Sentiment, Technicals Lens

Macro: the major data release last week was the PPI. Malaysia’s Producer Price Index (PPI) for local production fell 3.8% year-on-year in July 2025, easing from the 4.2% decline recorded in June, according to the Department of Statistics Malaysia (DOSM). The softer contraction was largely driven by continued weaknesses in the Mining and Manufacturing sectors. The Mining index fell 8.7% (June: -8.0%), dragged down by lower prices in the extraction of crude petroleum (-9.8%) and natural gas (-4.7%). Meanwhile, the Manufacturing sector declined 4.0% (June: -4.3%), reflecting sharper falls in the manufacture of coke & refined petroleum products (-15.7%) and computer, electronic & optical products (-7.6%). The key events for the week ahead will be tomorrow's S&P Global Malaysia PMI Manufacturing and Thursday's Central Bank decision. The PMIs have been consistently in contraction for 3 years and it is difficult to forecast any significant changes to that momentum. The Central Bank meets Thursday and whilst some market commentators are suggesting that a rate cut is in the pipeline, market consensus and pricing suggests it may not be this meeting. Data continues to be mixed in Malaysia with Industrial production higher, PMIs continuing to contract and the resultant GDP outcome, moderately lower than forecast. Despite this, we think that the BNM will remain patient and likely deliver one further cut at later meetings, remaining on hold this week.

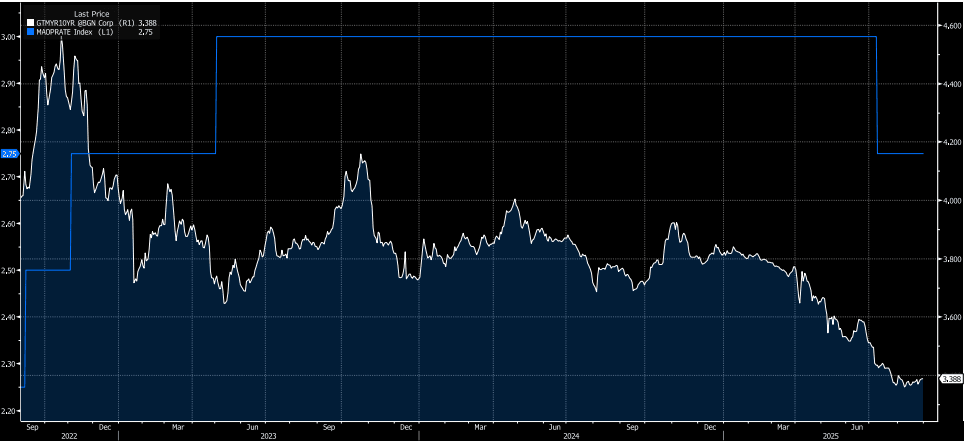

Valuations: The relationship between the 3 year MGS and the Central Bank rate has been reasonably stable at approximately ~80bps differential over the last two years. There has been no dramatic shift in this relationship of late suggesting any view on interest rate cuts is balanced. P/Es for the FTSE Bursa Malaysia KLCI has moderated of late and current forecasts suggest a further moderation is possible. At 14.80 x, it is in line with averages over recent years suggesting that at this stage, it is not overvalued.

Fig1: MGS 3-Year Government Bond Yield vs BNM Central Bank Rate

Source: Bloomberg Finance L.P./MNI

Sentiment: bid to cover on longer dated issuance has been fairly stable, with bid to cover's on shorter issuance much higher. This could point to some domestic bond investors are positioning for a rate cut. Sentiment for the equity market remains good with returns over the last month positive, though at the bottom end of the range for regional peers. For rates, if the BNM remains on hold, the market will be looking for signs that the door is open for a cut later in the year.

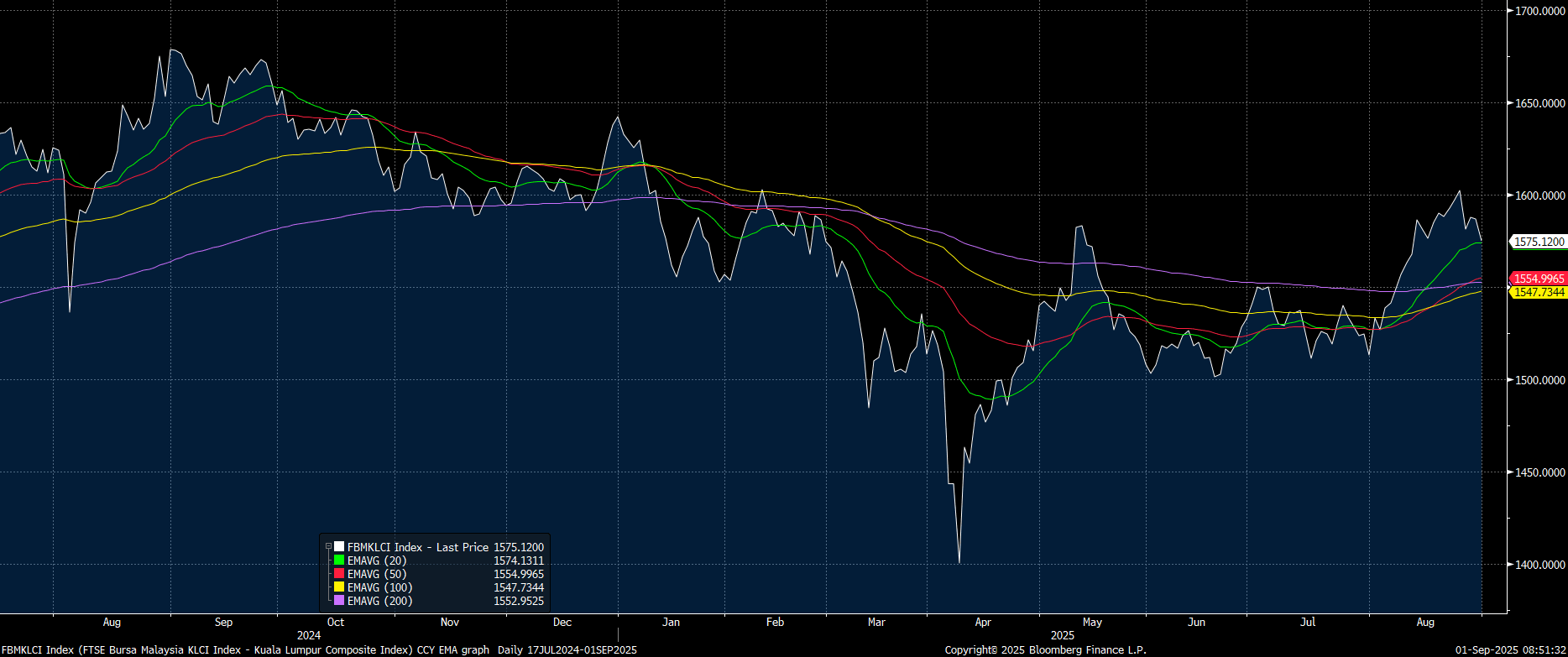

Technicals: the FTSE Bursa Malay KLCI index had a weak finish to August and now at 1,575 sits atop the 20-day EMA of 1,574. A break below could see further falls towards the 50-day EMA of 1,554. There is no major government bond issuance this week.

Fig 2: FTSE Bursa Malay KLCI vs 20, 50, 100 and 200 day EMA

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (U5) NFP Tips Prices Sharply Higher

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 138.63 @ 17:23 GMT Aug 1

- SUP 1: 137.32 - Low Jul 25

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs rallied sharply alongside global bond markets Friday, piercing mid-week resistance in the process. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal. A return lower would signal scope for an extension towards 136.57, a Fibonacci projection.

USDCAD TECHS: Slips Sharply on USD Downdraft

- RES 4: 1.4111 Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3794 @ 17:42 BST Aug 1

- SUP 1: 1.3716/3557 20-day EMA / Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A short-term bullish corrective phase in USDCAD remains in play despite sharp weakness Friday. On the recent run higher, price traded through the 50-day EMA at 1.3739 and this has been followed by a break of resistance at 1.3798, the Jun 23 high. Clearance of 1.3798 represents an important short-term bullish development, signalling scope for a stronger recovery. Sights are on 1.3920 next, the May 21 high. On the downside, initial firm support to watch lies at 1.3716, the 20-day EMA.

MACRO ANALYSIS: MNI US Macro Weekly: Poor Payrolls Trumps Patient Powell

- We have published and e-mailed to subscribers the MNI US Macro Weekly offering succinct MNI analysis across the range of macro developments over the past week.

- Please find the full report here.

Executive Summary

- The second half of the week has seen some significant moves in markets from first a patient Fed Chair Powell not giving a nod to a September rate cut before a weak payrolls report with huge downward revisions materially altered recent trends.

- Nonfarm payrolls growth underwhelmed at 73k in July but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector. Outside of April 2020, that’s the largest two-month downward revision in at least forty-five years.

- We caution though that whilst jobs growth has soured sharply, it’s doing so along with a significant slowing in labor supply under immigration curbs.

- As such, the unemployment rate may have technically ticked up to a new cycle high of 4.248% (above 4.244% in May) but it continues to roughly plateau in the 4.0-4.25% range seen since last July. The median FOMC forecast from the June SEP had the unemployment rate increasing to an average 4.5% in 4Q25 as part of forecast with two rate cuts in 2025 so further deterioration would be expected.

- A note on the latest initial jobless claims data, which are back at 2019 averages, a period when the unemployment rate averaged 3.7%.

- The weak report prompted an extraordinary response from President Trump, directing his team to fire BLS Commissioner Erika McEntarfer. It’s a broadening out of criticism beyond the Fed’s Powell and its Board.

- Speaking after payrolls, Atlanta Fed’s Bostic (in a non-voting role this year) said he hasn’t changed his view that there should be just one rate cut this year.

- Elsewhere in a major week for data, core PCE inflation exceeded latest Fed tracking in June at 2.8% Y/Y, whilst away from any tariff impact, market-based services inflation printed 3.3% Y/Y. Various inflation metrics showed a continued stabilization at above 2% target rates.

- The Q2 GDP advance release meanwhile beat analyst expectations with 3.0% annualized although it was close to Atlanta Fed GDPNow expectations. PDFP moderated further to 1.2% annualized for its weakest since 4Q22 although could have been worse.

- As a precursor to next week’s ISM Services report, the Manufacturing counterpart was weak across the board in July. Prices paid pulled back from recent highs, new orders chalked up a sixth consecutive month firmly in contraction territory and the employment index fell to its lowest since mid-2020.

- Yields have tumbled after the weak payrolls report. A September cut is mostly priced now vs 50/50 before the release, with a cumulative 59bp by year-end and five cuts in total from current levels.