EMISSIONS: Weekly News Highlights MNI Power Service Part 2/2 Week 49

Dec-05 14:01

See below the weekly news highlights of the MNI Power Service for the week 1 - 5 December.

EMISSIONS

- A total of 20.2mn EUAs will be auctioned next week across five auction sessions.

- EUA Dec25 options implied volatility fell to an all-time low on 4 Dec, with put open interest rising and calls declining, signalling stable expectations for price swings and caution over downside risks.

- UKA Dec25 options implied volatility as of 4 Dec fell to the lowest level since mid-November, while the call-put volatility skew turned positive for the first time since early November, reflecting stable expectations for volatility and near-term upside risks.

- Investment funds sharply increased net long positions in EU ETS futures on the ICE exchange to a new record high, according to the latest CoT data as of 28 November.

- Investment funds raise their net long positions in UK ETS futures on the ICE exchange as of 28 November to a four-week high.

- Rabobank raised its Q4 2025 EUAs forecast to €78.25/tCO2e from €75/tCO2e published in October, citing strengthened sentiment in the EU ETS and improved demand from industrial and power sector.

- GMK Centre said that EUAs could reach €85/tCO2e in 2026, €100/tCO2e in 2027 and €158/tCO2e in 2030.

- BNEF forecasted that EUAs would reach €158/tCO2e in 2030 if the EU were to expand the EU ETS aviation scope to cover all international departures from the region.

- BNEF forecasted that the EU ETS 2 price will peak at €121/t in 2032, considering the one-year delay, compared with the forecasted peak of €126/t in 2031 under the original start date of 2027.

- The EU ETS cap in 2026, excluding aviation, will be cut by 8.7% year-on-year, exceeding the annual reduction of 4.3% previously set for 2024-2027 in the ETS Directive.

- EEX EUAs secondary market traded volumes in November 2025 fell 16% on the year but rose 116% on the month.

- LEBA OTC physically delivered EUAs volumes in October 2025 were at 186Mt, up 14% m/m and down 10% y/y. Meanwhile, UKA volumes were at 53.4Mt, up 176% m/m and up 70% y/y.

- European power sector emissions are forecast to fall by around 7% on the month in December, weighed on by stronger renewables and hydropower generation.

- Centre for Climate and Energy Analyses projected that EU CBAM revenues in 2030 will reach €5–9bn, and €16–31bn under the extended scope.

- ICE published the 2026 UK ETS auction calendar late on Monday with total volumes dropping by 7% on the year. ICE is set to auction a total of 51,863,000 UKAs in 2026 across 25 auctions.

- The UK ETS Authority has set Phase II to run from 2031–2040 and confirmed that banking of allowances between Phases I and II will be permitted.

- The UK ETS Authority has set the 2026 civil-penalty carbon price at £49.41/tCO2e, a 18% discount to current UKAs Dec26 prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bear Steepening Alongside Tsys

Nov-05 13:57

Gilts take cues from Tsys, which have softened in the wake of the ADP employment report and guidance from the U.S. Treasury re: future coupon issuance increases.

- Gilt futures trade to lowest levels of the day, breaking Monday’s lows.

- Still, bears don’t challenge initial support at the October 27 low (93.15). The bullish technical theme remains intact.

- Yields now 0.5-3.0bp higher, curve steeper.

- Medium-term uptrend support (drawn off the August ’23 low) remains intact in the 2s10s curve.

- A reminder that we flagged risks of steepening around a dovish outcome at tomorrow’s BoE decision.

FOREX: Dollar Maintains Supportive Tone Following Data/Refunding

Nov-05 13:52

- In the aftermath of both the ADP data and the US refunding announcement, pressure on treasuries has provided a supportive tone to the greenback, helping the USD index consolidate gains near recovery highs.

- The higher yields have most notably assisted USDJPY to the best levels of the session, now extending its bounce from the overnight lows to over 100 pips, trading just shy of 154.00. We highlighted yesterday that the pair stalled for a third time around the 154.45 level overnight - a potentially bearish short-term signal against the underlying bullish trend that has been in place in recent weeks.

- This area will remain in focus heading into the ISM services release later today. Above here, attention would be on 154.80, the Feb 12 high.

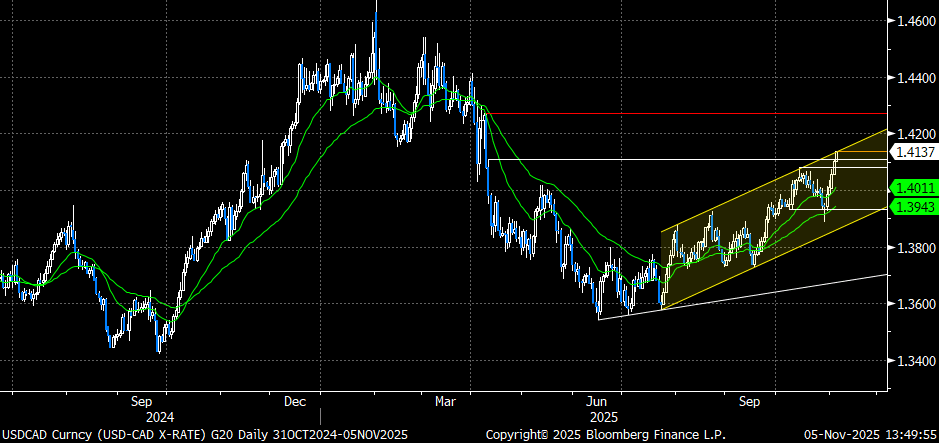

- Associated moderate pressure on the likes of EURUSD and GBPUSD, although both pairs remain off recent cycle lows, while USDCAD continues to pressure the top of the bullish channel drawn from the Jul 23 low and shown below:

EURIBOR OPTIONS: Large outright Call buyer

Nov-05 13:51

ERU6 98.50c, bought for 3.25 in 13.5k.