POWER: Weekly News Highlights MNI Power Service Part 2/2 Week 44

See below the weekly news highlights of the MNI Power Service for the week 27 - 31 October.

- Fortum advanced its outright power hedges for its power generation in the Nordics for 2025 and 2026 while achieving higher prices on the quarter.

- Vattenfall advanced its power hedges for its planned Nordic nuclear and hydropower generation for 2026-27, with hedging for 2025 unchanged on the quarter.

- Nordic spot prices could be weighed down heading into next week (3-9 November) amid the return of the 1.4GW OS3 nuke on 2 November – albeit extended from 31 October – coupled with above seasonal temperatures.

- Nordic hydro stocks rebounded slightly in week 43 to 80.8% of capacity as higher precipitation offset firm power demand and slightly lower nuclear output. However, stocks widened their deficit to 2024 to a multi-week high.

- Fingrid confirmed on Wednesday that Aurora Line interconnector between Finland and northern Sweden (SE1) is scheduled to be commissioned on 13 November.

- Svenska kraftnat reports that after a year of flow-based capacity calculations, electricity transmission in Sweden has increased by up to 51%, including 460 MW between areas 1 and 2 and 1.14GW between areas 2 and 3.

- TSOs AST and Elering are starting a feasibility study for a 1GW offshore power link between Estonia and Latvia, with technical and economic analyses to be completed by early 2026.

Orlen has secured PLN3.5bn (€830mn) in financing from Poland’s National Recovery Plan to support the development of 2.2GW of offshore wind in the Baltic Sea.

EMISSIONS

- A total of 16.8mn EUAs will be auctioned next week across four auction sessions.

- LEBA OTC physically delivered EUA volumes in September 2025 were at 163Mt, up 26% m/m and down 18.8% y/y. Meanwhile, UKA volumes were at 19.3Mt, up 35% m/m and down 31.8% y/y.

- Investment funds slightly reduced their net long positions in EU ETS futures on the ICE exchange, while remaining at the highest since early May 2021.

- Investment funds cut their net long positions in UK ETS futures on the ICE exchange as of 24 October.

- The Danish presidency of the Council of the EU is set to propose measures to prevent sectors under the EU ETS from being penalised if other sectors fail to meet their emissions targets under the proposed 2040 climate target.

- EUA prices are forecast to surge to €207 by 2034 as free allowances start phasing out from 2026 through 2034.

- BNEF said the EU ETS cap for stationary installations is expected to fully expire by 2044, with TNAC projecting to fall to around 560 million tCO2e by the mid-2030s from 1,000 million tCO2e in 2024.

- EU Central Bank President Christine Lagarde confirmed a delay to the EU ETS2 implementation is unlikely.

- The latest proposed EU ETS 2 reform could increase total allowance supply by 10% between 2027-2035 if all 600 million allowances held in the Market Stability Reserve (MSR2) are released.

- The latest UN analysis showed that the submitted NDCs from more than 60 countries would cut global emissions by only 10% by 2035 versus 2019, roughly a sixth of what is required to limit warming to 1.5C.

- The UK is set to put methane in the spotlight at the World Leaders Summit on 6–7 November and COP30.

- The UK Government has published its “Carbon Budget and Growth Delivery Plan” and the response to the Climate Change Committee’s suggestions on Wednesday.

- The EU and India have agreed to continue negotiations on CBAM following the EU minister’s official visit, aiming to finalise a deal by the end of 2025.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

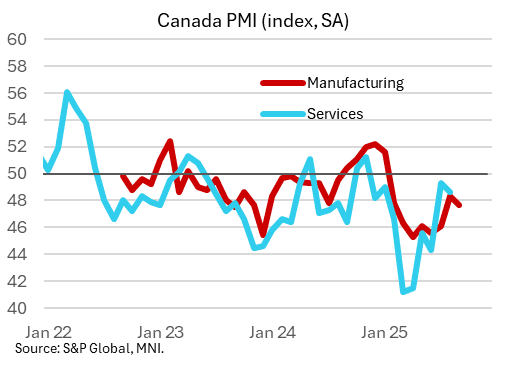

CANADA DATA: Manufacturing PMI Suggests Poor Activity, Softer Price Pressures

Canadian Manufacturing PMI softened in September, to 47.7 (no consensus) from 48.3 prior in what was an overall weak report. August had marked a 7-month high for the index, with the latest move lower keeping it below the 50 mark for an 8th consecutive month.

- The report showed poor demand, production, exports, and employment in the month, suggesting that a nascent pickup in activity over the summer (highlighted by better-than-expected GDP in July followed by anticipated flat growth in August) lacks momentum, at least in the beleaguered manufacturing sector. Per the S&P Global report:

- "Both output and new orders contracted in September, and at quicker rates than in August. Panellists continued to bemoan the adverse impact on demand of tariffs and wider economic uncertainty. Production and new orders have now fallen for eight months in a row. New export sales were again especially hard hit due to tariffs, with firms again pointing to continued weakness in sales to the United States. The lack of overall new orders and cuts to production meant firms generally chose to not replace leavers at their plants. Some firms also reported enforced layoffs. The net result was a decline in employment for an eighth successive month, although the rate of contraction was modest and the softest since February."

- While "Tariffs meanwhile remained an ongoing source of cost pressures in September and "Input prices again rose sharply", "the rate of inflation eased noticeably since August and was the second-lowest of the year so far." And importantly for the BOC's consideration, "Manufacturers struggled to pass on their higher input costs

to clients in the form of increased selling prices during the month. This was highlighted by the latest data on output charges, which increased only modestly in September and to the softest degree in nearly a year. Panellists attributed their lack of pricing power to market competition and a soft demand environment." - We get the Services/Composite PMI figures on Friday.

USDJPY TECHS: Clears Support At The 50-Day EMA

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 151.21 High Mar 28

- RES 2: 150.92 High Aug 1 and a key resistance

- RES 1: 148.84/149.96 High Sep 30 / 26 and the bull trigger

- PRICE: 146.64 @ 14:45 BST Oct 1

- SUP 1: 146.59 Intraday low

- SUP 2: 146.36 Trendline support drawn from the Apr 22 low

- SUP 3: 145.49 Low Sep 17 and a pivot support

- SUP 4: 144.23 Low Jul 7

USDJPY continues to weaken as the retracement from last week’s high print extends. The move down has resulted in a clear breach of the 50-day EMA, at 147.60. This signals scope for a deeper retracement and exposes the key short-term pivot support at 145.49, the Sep 17 low. A clear break of this level would cancel a recent bull theme. On the upside a reversal higher would refocus attention on resistance at 149.69, the Sep 26 high and a bull trigger.

MNI: US SEP FINAL MANUF PMI 52.0 (52.0 FLASH, 53.0 AUG)

- MNI: US SEP FINAL MANUF PMI 52.0 (52.0 FLASH, 53.0 AUG)