POWER: Weekly News Highlights MNI Power Service Part 1/2 Week 44

See below the weekly news highlights of the MNI Power Service for the week 27 - 31 October.

POWER

- Total power EU LEBA volumes rebounded sharply in September from August to 509.69TWh – the highest since November 2024. The deficit to volumes traded the EEX exchange widened to its highest since June 2025.

- European gas-fired power generation is forecast to rise by almost 10% on the year in 2025 according to the IEA.

- German gas-fired power generation is on track to rise well above 2024 levels and the five-year average in October, replacing hard-coal and lignite output.

- RWE eyes installing an 850MW hydrogen-compatible combined cycle power plant at the former RWE power station site in Voerde, Germany.

- Germany’s new network reform – NEST – is expected to enter into force by the end of this year and will apply to electricity grids from 2029 and gas networks from 2028.

- French hydropower reserves in calendar week 43 increased by 3.7 percentage points to 68% of capacity, sharply narrowing the deficit to the five-year average.

- France’s economy ministry declined to provide a timeline for the publication of the third multi-year energy programme (PPE) but stresses the roadmap remained a top priority.

- UK gas-fired output in October is set to reach around 9.8GW, its highest since March 2025, but remains down 29% year-on-year as wind generation nearly doubles to an average of about 8.4GW.

- The UK government on Monday unveiled the CfD budget allocation for AR7, reducing support for offshore wind developments. The UK plans to allocate an overall budget for offshore wind and floating offshore wind projects of £1.08bln. The budget has been criticized by market participants for being too low.

- The Netherlands Enterprise Agency (RVO) received no applications for the construction and operation of a new 1GW offshore wind farm at the Nederwiek I-A site in the North Sea.

- Swiss hydropower reserves in calendar week 43 slowed the pace of the decline, dropping by 1.5 percentage points to 78.2% of capacity. Stocks widened the deficit to the five-year average and to the same week in 2024.

- Italian hydropower reserves in calendar week 43 remained relatively unchanged the week to drop by just 0.01TWh to 2.69TWh of capacity. Stocks widened their deficit to the 5-year average.

- Iberdrola, Endesa, and Naturgy have requested to extend operations at Spain’s Almaraz nuclear plant, seeking to keep its two units online until June 2030 from 2027–28 currently scheduled.

- Spanish hydropower reserves in calendar week 43 declined by 0.5 percentage points to 51.6% of capacity, narrowing the surplus to the five-year average and last year’s level.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

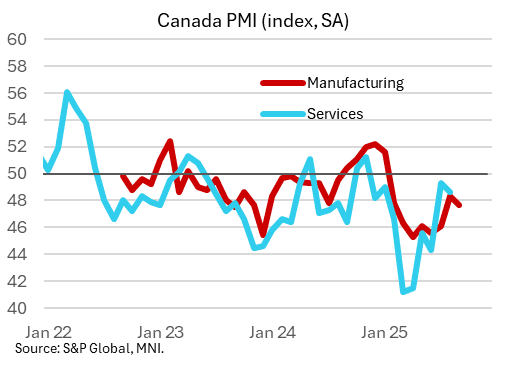

CANADA DATA: Manufacturing PMI Suggests Poor Activity, Softer Price Pressures

Canadian Manufacturing PMI softened in September, to 47.7 (no consensus) from 48.3 prior in what was an overall weak report. August had marked a 7-month high for the index, with the latest move lower keeping it below the 50 mark for an 8th consecutive month.

- The report showed poor demand, production, exports, and employment in the month, suggesting that a nascent pickup in activity over the summer (highlighted by better-than-expected GDP in July followed by anticipated flat growth in August) lacks momentum, at least in the beleaguered manufacturing sector. Per the S&P Global report:

- "Both output and new orders contracted in September, and at quicker rates than in August. Panellists continued to bemoan the adverse impact on demand of tariffs and wider economic uncertainty. Production and new orders have now fallen for eight months in a row. New export sales were again especially hard hit due to tariffs, with firms again pointing to continued weakness in sales to the United States. The lack of overall new orders and cuts to production meant firms generally chose to not replace leavers at their plants. Some firms also reported enforced layoffs. The net result was a decline in employment for an eighth successive month, although the rate of contraction was modest and the softest since February."

- While "Tariffs meanwhile remained an ongoing source of cost pressures in September and "Input prices again rose sharply", "the rate of inflation eased noticeably since August and was the second-lowest of the year so far." And importantly for the BOC's consideration, "Manufacturers struggled to pass on their higher input costs

to clients in the form of increased selling prices during the month. This was highlighted by the latest data on output charges, which increased only modestly in September and to the softest degree in nearly a year. Panellists attributed their lack of pricing power to market competition and a soft demand environment." - We get the Services/Composite PMI figures on Friday.

USDJPY TECHS: Clears Support At The 50-Day EMA

- RES 4: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 3: 151.21 High Mar 28

- RES 2: 150.92 High Aug 1 and a key resistance

- RES 1: 148.84/149.96 High Sep 30 / 26 and the bull trigger

- PRICE: 146.64 @ 14:45 BST Oct 1

- SUP 1: 146.59 Intraday low

- SUP 2: 146.36 Trendline support drawn from the Apr 22 low

- SUP 3: 145.49 Low Sep 17 and a pivot support

- SUP 4: 144.23 Low Jul 7

USDJPY continues to weaken as the retracement from last week’s high print extends. The move down has resulted in a clear breach of the 50-day EMA, at 147.60. This signals scope for a deeper retracement and exposes the key short-term pivot support at 145.49, the Sep 17 low. A clear break of this level would cancel a recent bull theme. On the upside a reversal higher would refocus attention on resistance at 149.69, the Sep 26 high and a bull trigger.

MNI: US SEP FINAL MANUF PMI 52.0 (52.0 FLASH, 53.0 AUG)

- MNI: US SEP FINAL MANUF PMI 52.0 (52.0 FLASH, 53.0 AUG)