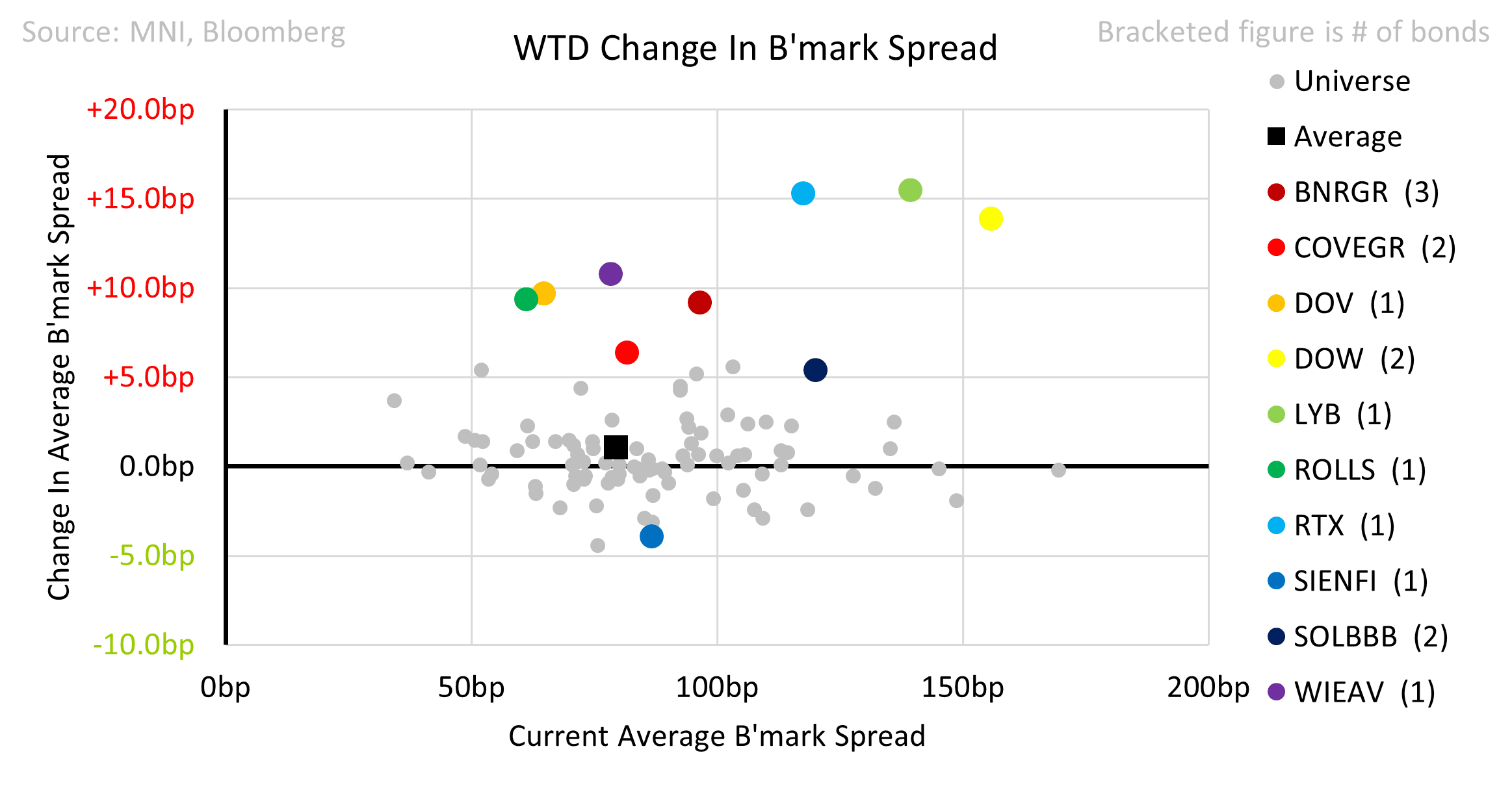

EU BASIC INDUSTRIES: Week in Review

Jul-18 13:28

- BASF cut FY25 EBITDA guidance by ~9%, which was somewhat expected.

- Brenntag EBITA missed; it cut FY guidance by ~9%.

- Solvay flagged in-line 2Q EBITDA and lowered FY25 EBITDA guidance by ~9%. It expects 2H to remain weak.

- Sandvik reported a slight EBITA miss; leverage also increased modestly.

- ABB reported a firm 2Q and confirmed FY25 guidance.

- GE Aerospace raised FY25 guidance after strong Q2 results.

- Legrand raised FY25 revenue growth guidance following 10% organic growth in Q2.

- Assa Abloy posted a margin beat and stable leverage despite soft market conditions.

- SKF reported performance in line with expectations and confirmed its Automotive spin-off is on track.

- Epiroc revenue missed expectations, but with no significant credit impact.

- 3M reported a slight beat and upgraded EBIT margin guidance.

- Atlas Copco results were soft, without really impacting the credit.

Givaudan, Norsk Hydro, Akzo Nobel, Alfa Laval, RTX, Avery Dennison, Kier, Thales, Stora Enso, Alstom, TE Connectivity, Otis, Hochtief, Amphenol, Metso, Huhtamaki, UPM-Kymmene, Westinghouse, Honeywell, MTU Aero Engines, Dow, Dover and Mohawk are due to report next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

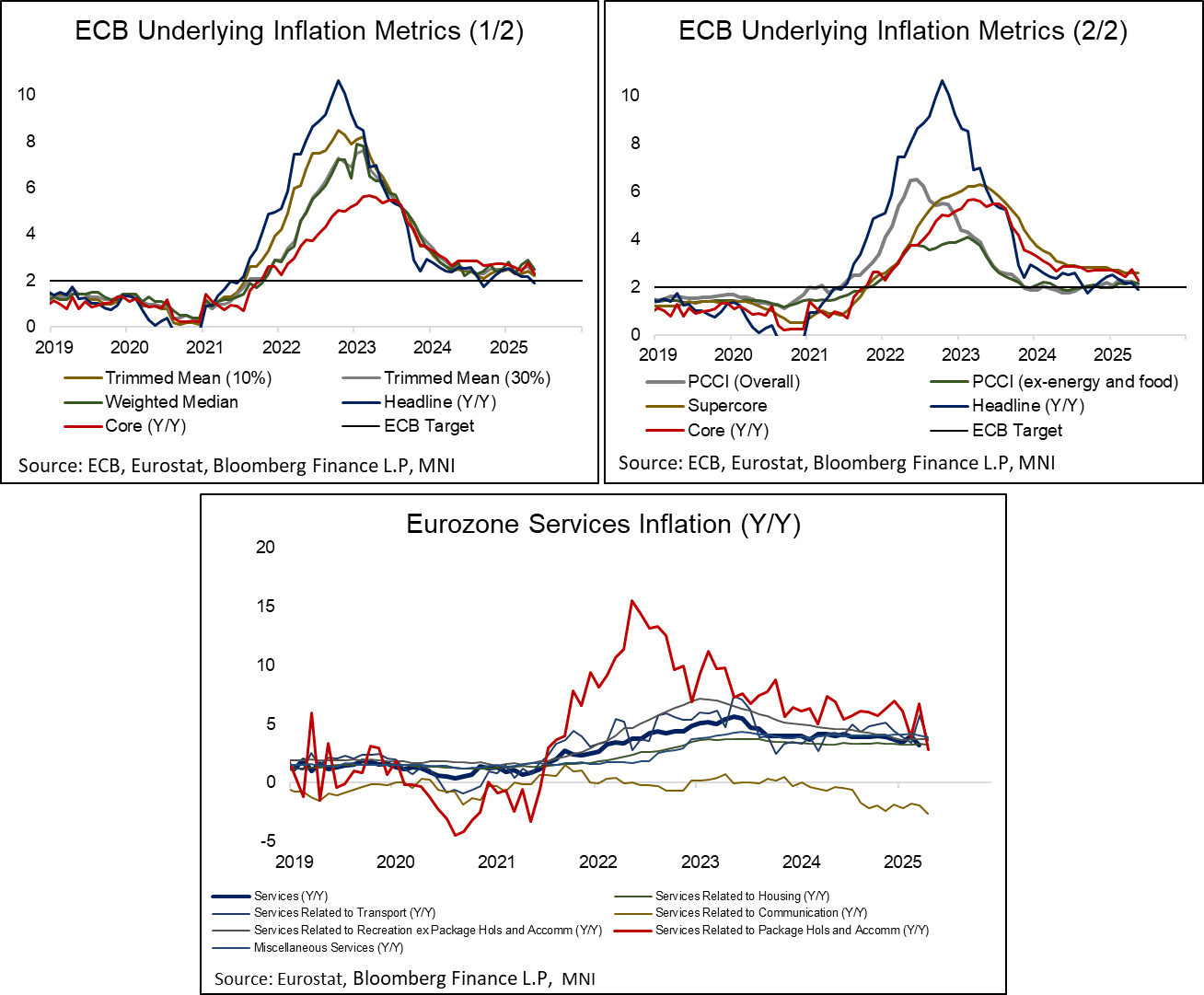

EUROPEAN INFLATION: Easter Sensitive Categories Drove May Services Disinflation

Jun-18 13:27

- As foreshadowed by country-level data, the pullback in Eurozone services inflation to 3.23% Y/Y (vs 3.98% prior) was largely a function of lower airfares, package holidays and accommodation inflation (i.e. Easter-sensitive categories).

- Despite this, the ECB has expressed broader confidence around the outlook for services inflation. In the June projections, they staff noted that “In the medium term, the decline in HICPX inflation mainly relates to services inflation as post-pandemic reopening effects unwind and the as the downward impact from monetary policy tightening continues to feed through. A faster unwinding of services inflation is seen to be hindered by declining but still elevated upward pressures from labour cost developments.” Services inflation is seen at 3.2% Y/Y in Q4 2025 and 2.5% Q/Q in Q4 2026.

- Indeed, the ECB’s underlying inflation metrics saw a broad-based softening in May, converging slowly towards the 2% level.

- Services related to package holidays and accommodation eased to 2.84% Y/Y in May (vs 6.73% prior), the lowest since 2021. Meanwhile, services related to transport (mostly airfares) fell to 3.62% Y/Y (vs 5.74% prior).

- Other services categories saw much smaller movements on the month:

- Services related to communication: -2.59% Y/Y (vs -1.92% prior),

- Services related to housing: 3.28% Y/Y (vs 3.29% prior).

- Services – miscellaneous: 3.86% Y/Y (vs 4.00% prior).

- Services related to recreation and personal care, excluding package holidays and accommodation: 3.72% Y/Y (vs 3.74% prior).

- The ECB’s seasonally adjusted data saw immaterial revisions relative to the flash release. Services prices fell 0.17% M/M (in line with flash) while non-energy industrial goods were revised down to 0.03% M/M from 0.06% initial.

EQUITIES: US Cash Opening calls

Jun-18 13:27

- SPX: 5,999.3 (+0.3%)

- DJIA: 42,284 (+0.2%/+69pts)

- NDX: 21,802.6 (+0.4%)

MNI EXCLUSIVE: Riksbank Governor Erik Thedeen speaks to MNI in an interview

Jun-18 13:11

Riksbank Governor Erik Thedeen speaks to MNI in an interview - On MNI Policy MainWire now, for more details please contact sales@marketnews.com