EU UTILITIES: Week in Review

May-02 12:50

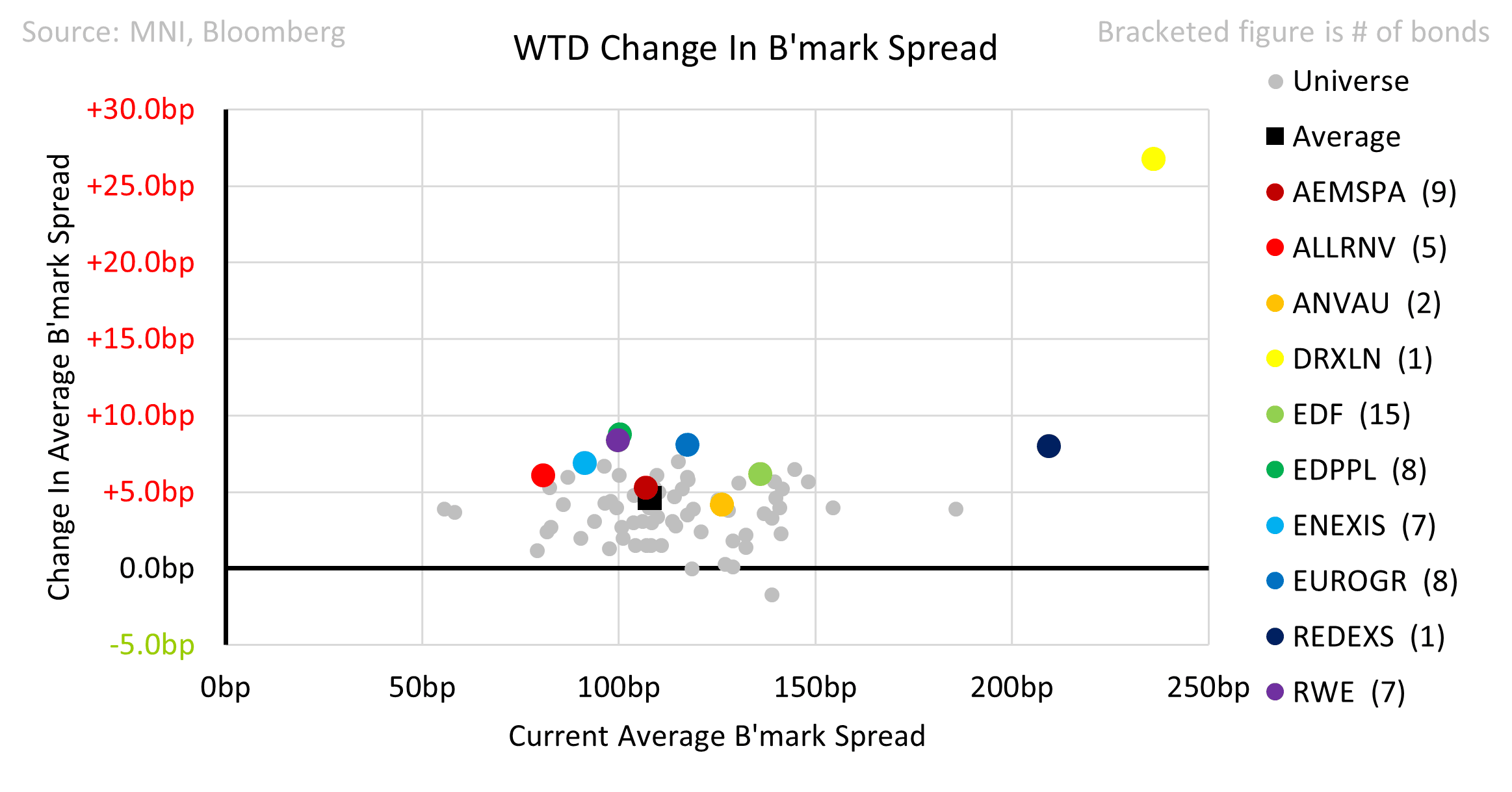

- Spreads performed in-line with the index at +5bp.

- Fortum results showed normalising EBITDA which was still well ahead of consensus. Leverage hit 0x net, which should be trough levels.

- Redeia reported modest EBITDA growth. Guidance was in-line with its strategic plan.

- Vattenfall numbers showed credit metrics normalising from strong levels. Its FFO/ND target was adjusted from 22-27% to above 25%.

- Ausnet priced a 10Y 10bp through our FV.

- Alliander brought 8Y and 10Y deals 5 and 2bp inside our FV.

- EDF printed 7Y, 12Y and 20Y paper 5, 3 and 8bp wide to our FV.

- Ellevio mandated a new 10Y Green.

Next week has earnings scheduled from Duke, Veolia, Orsted, Italgas, Snam, REN, Enel and EDP.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA: Call spread vs put spread

Apr-02 12:50

SFIZ5 96.20/96.30cs vs 95.75/95.65ps, bought the cs for 2 in 2.5k.

FINLAND AUCTION PREVIEW: ORI Operation Tomorrow

Apr-02 12:46

Finland has announced it will be looking to sell up to a combined E400mln of the following at its ORI operation tomorrow, April 3:

- the 0.50% Sep-27 RFGB (ISIN: FI4000278551)

- the 2.625% Jul-42 RFGB (ISIN: FI4000046545)

US DATA: ADP Beats In Solid Report, Usual NFP Correlation Caveats Aside

Apr-02 12:44

- ADP employment growth was stronger than expected in March at 155k (cons 120k) after a marginally upward revised 84k (initial 77k) in February.

- It leaves an average monthly 142k increase in Q1 and with the latest increase above the average 144k in 2024, offering a reasonably solid report along with other hard data vs weaker soft data.

- Correlation with private payrolls growth remains a concern. In latest vintages for both releases, ADP undershot by -56k in Feb, overshot by 105k in Jan and undershot by -111k in Dec. That said, the private payrolls series has admittedly been the more volatile series in recent months.

- Bloomberg consensus for private payrolls currently stands at 135k.

- With that standard caveat aside, there was an impressive bounce in seasonally adjusted hiring from smallest firms, with those with 1-19 employees adding 42k jobs after a rare 4k decline in Feb (revised from the -17k initially, a first monthly decline since Dec 2023).

- There’s no clear trend by firm size when comparing the Q1 average job growth to that of 2024. The smallest (1-19) and largest (500+) employees have both seen a moderation in hiring (average 22k vs 39k and 54k vs 67k respectively) but all other sized firms have seen an acceleration in hiring.

- On the pay front, median annual pay eased to a new recent low for job changers at 6.5% Y/Y (from 6.8% in Feb and through September’s 6.6% for the lowest since early 2021.

- Job stayers meanwhile eased a tenth to a joint recent low of 4.6% Y/Y (otherwise lowest since mid-2021) with the combination seeing a joint low for the pay premium at 1.9pps.