US OUTLOOK/OPINION: Weather No Longer A ‘Likely But Hard To Prove’ NFP Drag

Apr-03 19:51

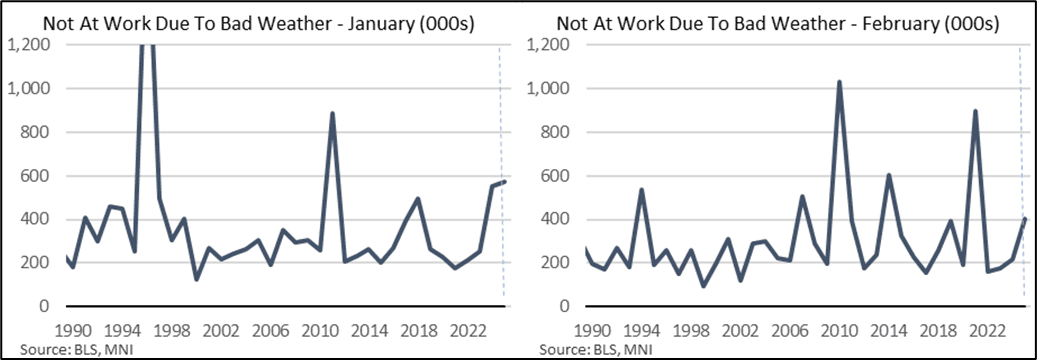

- January and February saw higher than usual weather disruption judging by the household survey question, despite the BLS in the January report saying that wildfires in Southern California and severe winter weather in much of the country "had no discernible effect on national payroll employment, hours, and earnings from the establishment survey, nor on the national unemployment rate from the household survey".

- February’s report showed 404k not at work due to bad weather, above the 216k in Feb 2024 for its highest since 2021 even if it was far from unprecedented. Notably though, it followed a more clearly larger than usual weather disruption in January, with the 573k unable to work close to the 553k in Jan 2024 but a clearer outlier historically.

- The combination saw 977k not at work over the first two months of the year, the highest since 1073k in 2021 and otherwise last higher in 2011.

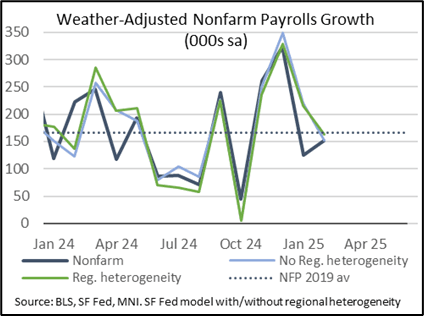

- Separately, San Francisco Fed staff estimate there was a small weather drag on February payrolls (-2k to -12k depending on model) after a heavy drag on January payrolls (-92k to -95k).

- March weather on the other hand is acknowledged to have improved relative to average.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: BLOCK: Repeat May'25/Midcurve 10Y Call Spread

Mar-04 19:49

- -16,000 TYK5 112.5 calls, 41 (47 earlier) vs. 111-09/0.20% vs. +17,500 wk4 TY 114 calls, 8 (9 earlier)

COMMODITIES: WTI Edges Lower, Henry Hub At 26-Month High, Gold Extends Gains

Mar-04 19:43

- Crude markets extended their decline earlier today, before paring most of the losses later in the session. Downside pressure came from confirmation that OPEC plans to return barrels to the market, coupled with the disruption to trade and potential hit to global economic growth from Trump’s tariff policy.

- WTI Apr 25 is down by 0.1% at $68.3/bbl.

- OPEC has signalled that it will proceed with its planned output hike of 138k b/d in April amid healthy market fundamentals and positive market outlook.

- The current bearish trend condition in WTI futures remains intact and this week’s fresh short-term cycle low reinforces current conditions.

- Support at $67.75, the Dec 20 ‘24 low, was pierced earlier today, with next support seen at $66.41, the Dec 6 ‘24 low.

- Meanwhile, Henry Hub climbed to its highest close since Dec 2022, driven by near record LNG feedgas flows, forecasts of higher demand next week, and concerns that flows from Canada could be disrupted by the looming trade war.

- US Natgas Apr 25 rose by 5.3% to $4.34/mmbtu.

- Spot gold is up by 0.7% to $2,914/oz, aided by broad dollar weakness as stagflationary concerns in the US gain traction.

- Next immediate resistance in gold comes at $2,920, which has been pierced. Above here, a stronger rally would refocus attention on the next objective at $2,962.2, a Fibonacci projection.

US STOCKS: Late Equities Roundup: Chip Stocks Spur late Bounce, Nasdaq Leads

Mar-04 19:39

- Stocks are mixed in later trade, S&P Eminis managing to claw their way off January lows, while the Nasdaq is in the green led by semiconductor stocks. Little has changed regarding underlying risk sentiment, however, global markets still concerned over the impact of 25% US import tariffs against Canada & Mexico, 20% on China, not to mention agriculture products starting April 2.

- Currently, the DJIA trades down 314.99 points (-0.73%) at 42874.67, S&P E-Minis down 20.25 points (-0.35%) at 5840.0 (vs. 5744.00 low), Nasdaq up 101.8 points (0.6%) at 18450.86.

- Information Technology and Communication Services sectors led gainers in the second half, semiconductor makers buoyed the Tech sector: Super Micro Computer +10.20%, Enphase Energy +8.61%, First Solar +4.14% and NVIDIA +3.00%.

- Interactive media and entertainment shares buoyed the Communication Services sector with Match Group +3.38%, Warner Bros Discovery +2.90% and Alphabet +2.89%.

- Financial and Consumer Staples sectors lead the decline in late trade: banks and services led laggers in the former with Citigroup -5.07%, Ameriprise Financial -5.01%, Discover Financial Services- 4.95%, Capital One Financial Corp-4.87% and Bank of America -4.72%.

- Meanwhile, Target -3.10%, Coca-Cola -2.56%, Estee Lauder Cos -2.54% and Philip Morris International -2.46% weighed on the Consumer Staples sector.

- Earnings expected after the close include: Crowdstrike Holdings, Ross Stores, Foot Locker, Campbell's, Abercrombie & Fitch, Brown-Forman Corp, Marvell Technology and Victoria's Secret.