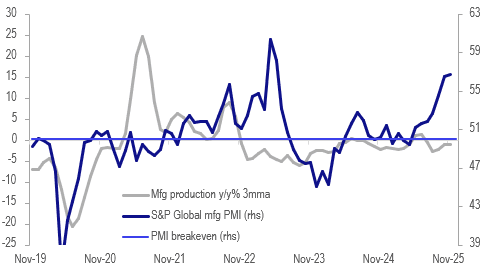

THAILAND: Weak November Manufacturing But Surveys Signal Recovery

November manufacturing production was weaker than expected falling 4.2% y/y, the sharpest contraction since August, likely impacted by recent severe weather events. The series can be volatile but the 3-month average is also negative holding at around -1% y/y. The S&P Global manufacturing PMI has signaled positive activity since May and a pickup in growth since August, which hasn’t materialized. The November PMI at 56.8 and the pickup in November business confidence signal that growth in the sector should improve.

Thailand manufacturing

- Capacity utilization was also soft in November falling to 55.5 from October’s 57.8, the lowest since April 2023. It has trended lower since US President Trump announced reciprocal tariffs in April.

- The Bank of Thailand cut rates 25bp to 1.25% in December bringing cumulative easing in 2025 to 100bp in an effort to stimulate economic growth especially in the face of baht strength which has pressured the economy. The BIS THB NEER is up 4.9% y/y while USDTHB is down 7.7% y/y.

- USDTHB is up 0.4% to 31.20 in Monday’s APAC trading after reaching 31.23 but still well below where it started December and only just off the month low at 31.01 on 24 December. It has found support from rising gold price this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

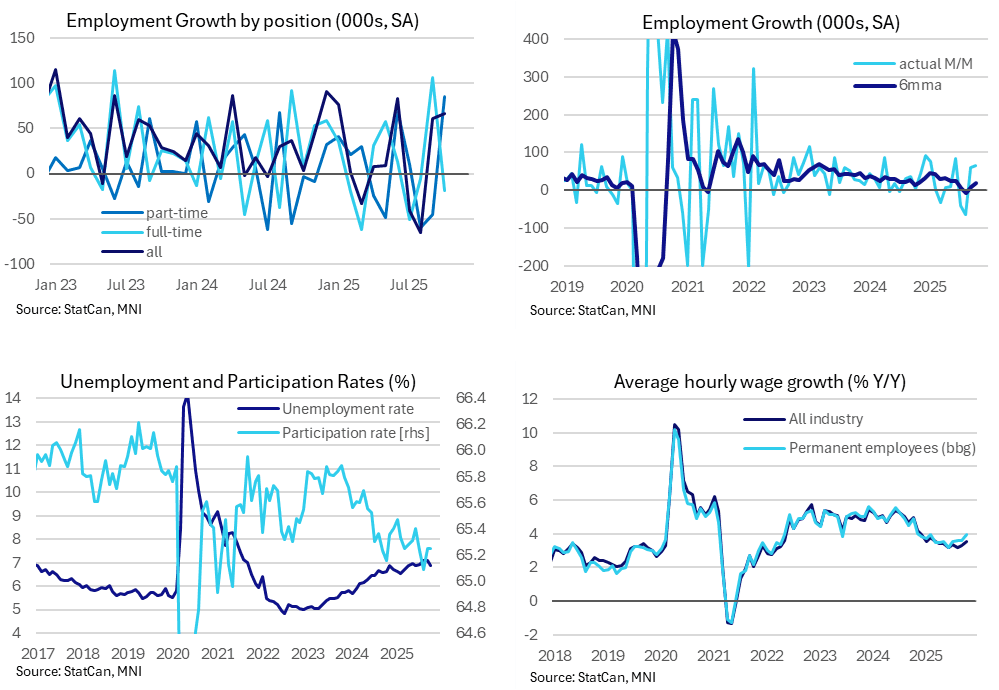

LOOK AHEAD: Canada Week Ahead: November Jobs Report In Clear Focus

- Friday’s labour force survey should help shape expectations for how long the BoC is likely to remain on hold for after signalling a pause ahead in October. The overnight rate of 2.25% is deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment."

- Employment growth is likely to slow materially in November and could decline after a far stronger than expected 67k increase in October that came entirely from part-time positions.

- The monthly changes have been volatile for some time now whilst the unemployment rate helps gives a better sense of labour market pressures.

- Bloomberg consensus currently eyes a 7.0% unemployment rate, albeit with twelve estimates for now, to lift again after a surprisingly low 6.9% in October pulled back from two months at 7.1% at what were the highest since mid-2021. Having increased through 2023 and 2024, the climb in the unemployment rate has levelled off having averaged 6.9% since late 2024.

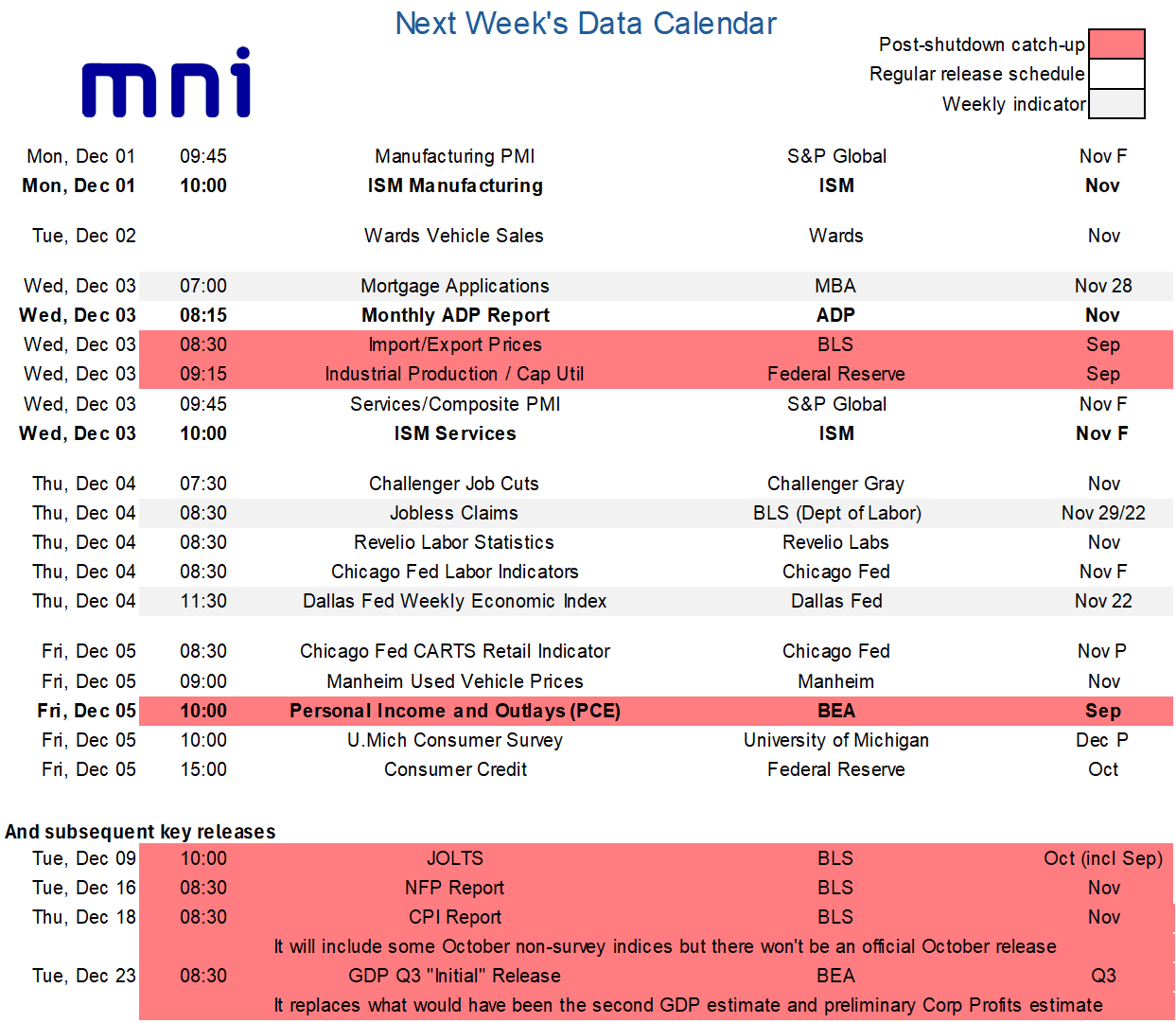

LOOK AHEAD: US Week Ahead: Last Pre-FOMC Labor Data, ISM Surveys & Delayed PCE

Next week would ordinarily have been geared towards a nonfarm payrolls report on Friday but that of course has been rescheduled for Dec 16 as the BLS continues to work its way through the shutdown-induced data backlog. Instead, expect the myriad of labor releases starting Wednesday along with ISM surveys and monthly PCE data to help finalize market expectations ahead of the Dec 9-10 FOMC meeting - we currently anticipate a hawkish cut.

- Within the labor releases, the monthly ADP employment report for November will continue to be important – with declines in recent weekly updates - but we also flag Thursday's releases for Challenger job cuts and Revelio Labs' labor statistics for November. The October Challenger report showed a sharp increase in layoffs to its highest for an October since 2003 along with tepid hiring plans over Sep-Oct combined, whilst the Revelio nonfarm payrolls estimate drew a dovish market reaction last month when it pointed to nonfarm payrolls growth of -9k in October.

- As for ISM surveys, consensus looks for little improvement in Monday’s manufacturing survey, with regional Fed surveys on balance slightly stronger on the month versus a sharp deterioration in the MNI Chicago PMI. The still early days for the services analyst survey sees a modest dip to 52.0 having oscillated between 52.0-52.5 in the previous four months. The service PMI – at 55.0 in the November flash – has been more optimistic in each of the prior six months but with varied beats each time.

- The delayed personal income and outlays report for September then rounds out the week on Friday. This week’s retail sales release will have dampened goods-related expectations for consumer spending. We’ll also watch income dynamics after they underwhelmed in the August report released two months ago, seeing the savings rate dropping to an eight-month low. Core PCE inflation estimates appears to be tracking around 0.22% M/M for September, similar to the 0.23% M/M in August and the 0.24% averaged through May-July although with some seeing scope for minor upward revisions to Aug and Jul.

CANADA: Analysts On Today’s GDP Beat And Softer Details

Details are broadly acknowledged to be weaker than the surprisingly strong Q3 GDP figure suggested, but the general takeaway is that it helps the BoC remain on hold. BoC-dated OIS agrees although there has only been a small adjustment on the day in post-Thanksgiving thinned trade, with ~8bp of cuts priced to mid-2026 vs closer to 10bp beforehand.

- BMO: “Amid the many moving parts in this report, the big bounce in headline Q3 growth is probably the most important, and should quash recession chatter for now. Even the marked upward revisions to prior years sends a clear signal that the underlying economy has been more resilient than commonly appreciated. Even so, we are not significantly changing our forward look on the economy, and will stick to an expected growth rate of 1.4% for next year (the federal budget assumed 1.2%). For the Bank of Canada, there are many mixed messages here, but the overall read is better than expected, thus more firmly putting them on the sidelines for next month's meeting.”

- CIBC: “The Canadian economy is set to swing back in the opposite direction in Q4. Even assuming a rebound in November GDP due to temporary strike impacts holding back the prior month's reading, growth is likely to stall. While we still see the BoC as on hold in December, the trend in final domestic demand isn't encouraging and exports showed little sign of recovering from the tariff-induced Q2 hit. Our forecast assumes that we see definitive progress on renewing CUSMA and a recovery in business confidence improving quarterly growth rates in 2026.”

- Desjardins: “While the headline Q3 GDP surprise will keep the Bank of Canada on the sidelines next month, the economy is clearly still in a very fragile state. Central bankers will need to remain on high alert early next year, with fiscal policy not expected to be a major contributor until at least the middle of 2026. Market participants are correctly looking through the headline Q3 increase in GDP, with yields back down to levels seen before the data release.”

- RBC: “Details behind the surprisingly large 2.6% (annualized rate) increase in Canadian Q3 GDP were mixed, with further signs of stabilization in heavily trade exposed sectors but some signs of faltering domestic demand. […] Slowing population growth will increasingly limit consumer demand and labour supply in the year ahead, but we expect per-capita GDP growth to improve and the unemployment rate to drift broadly lower next year -- and, against that backdrop, do not expect further interest rate reductions from the BoC as a base-case.”

- Scotia: “Could there be a messier set of GDP numbers? Not really. They made for fun trying to do instant coverage on the fly in chat rooms. I’m not sure that markets really understood what went on beneath the hood but they serendipitously wound up at the right conclusion regardless. CAD appreciated and Canadian bond yields moved higher across the board. The broad set of numbers needs further work but the conclusion is that they’ll keep the BoC sidelined.”

- TD: “For the Bank of Canada, the focus will be to look through the noise on trade. The 2.6% advance for the quarter may be well ahead of its 0.5% projection, but the underlying details remain disappointing. The story continues to be – slow domestic demand growth, labour market slack, and inflation that should gradually moderate in the coming months. From where we sit, these three factors should leave the Bank of Canada on the sidelines, and the policy rate at 2.25%.”