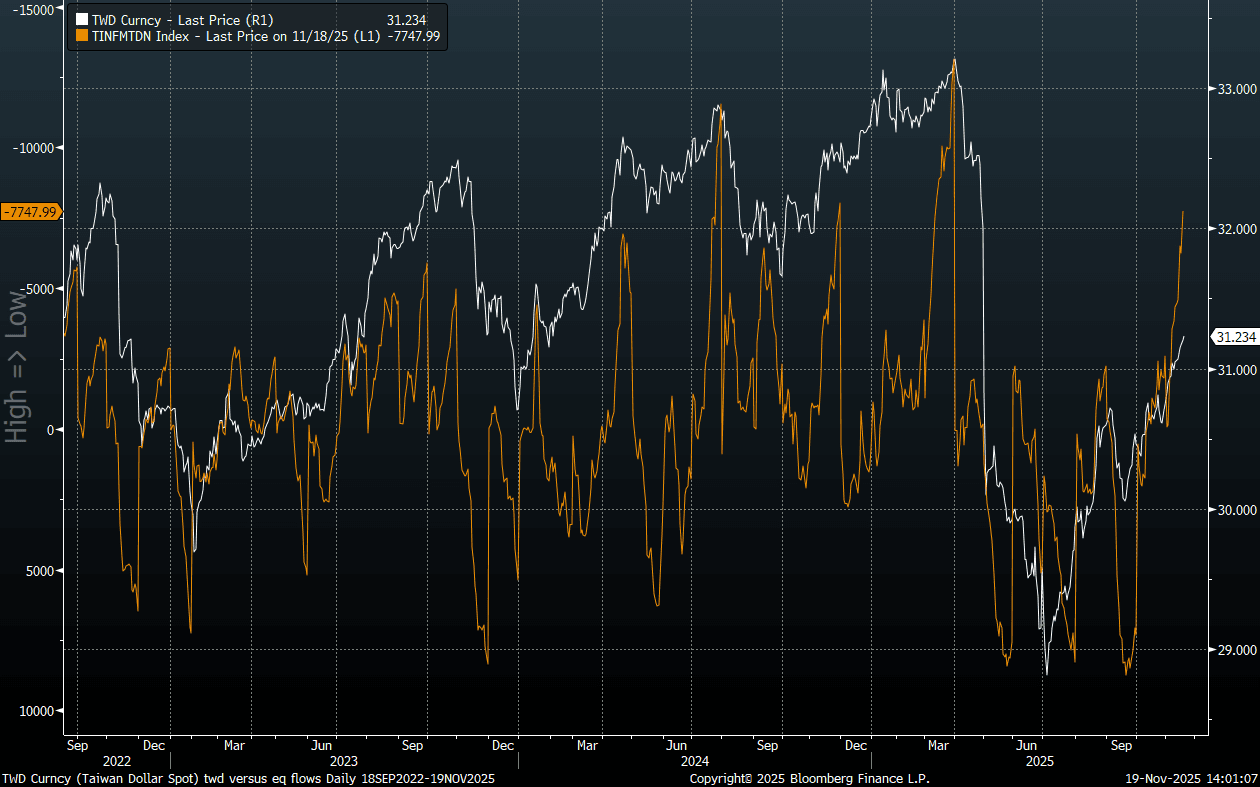

TWD: Wary Of USD/TWD Overbought Signals, But Tech Equity Sentiment Remains Weak

Spot USD/TWD remains in an uptrend, the pair last around 31.20/25, close to session highs. We continue to close the gap with the break down levels from late April/early May, where we went from 32.00 to under 30.00 in very short order. Key EMAs are mostly drifting higher (20-day near 30.96), while the 200-day is steadier, last near 30.85. The RSI (14) continues to push into overbought territory, last 77.41, but in the near term there seems few fundamental catalysts to evoke a turnaround, as markets await Nvidia results early tomorrow.

- Local equities remain under pressure, with upticks faded. The Taiex is under the 50-day EMA support point (off a further 0.55% today), and the last time we were meaningfully below this support point was in May of this year.

- Offshore investors continue to sell local stocks, now up to 7.75bn in outflows so far in Oct. The chart below plots these flow trends, which are inverted on the chart (the orange line) against spot USD/TWD.

- We are getting close to previous extremes from a monthly outflow standpoint, but it remains to be seen if we can see a positive catalyst that slows outflows/or turns momentum back positive.

- Outside of tomorrow's Nvidia result, note we also data on Oct export orders, which are expected to remain strong at +28%y/y (30.5% was the Sep outcome).

Fig 1: USD/TWD Spot & Monthly Offshore Equity Inflows (Inverted)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: HSI Nears the 50-day EMA as China US Tensions Simmer

- Friday's losses did not follow into Monday with major bourses delivering solid gains, with some trading through key technical levels.

- The Hang Seng lost -2.5% on Friday and has regained that today, trending above the 50-day EMA . At 25,877 above now is the 20-day EMA of 26,137 which it has trended above for most of the period from May. China stocks had a day of data releases and GDP moderated as expected, whilst Industrial Production surprised to the upside following on from better than expected exports reported last week. The CSI 300 has rebounded also though only by +0.80% as it tries to break back above the 20-day EMA. Easing trade tensions supported China's stocks as US President Trump said that 'much higher tariffs threatened wouldn't be sustainable', as a new round of talks between the two countries is about to start.

- The NIKKEI was the star yet again today roaring up +2.9% reaching another new all time high of 48,956. The cooling of the US China tensions added to the news that the LDP is likely to sign a new coalition deal with the Innovation Party, with pro-stimulus candidate Sanae Takaichi now on track to be the next Prime Minister.

- Not to be outdone by its neighbour in Japan, the KOSPI is up +1.43% to reach yet another new high of 3,801 today.

- Having suffered at the hands of US trade tensions with focus on its purchase of Russian oil, the NIFTY 50 continues its turnaround story up 200pts in morning trading to reach a new all time high of 25,913.

JPY: USD/JPY Off Highs, Policy Details Awaited From New Coalition

USD/JPY sits off earlier highs (151.20), last near 150.70/75, up only slightly versus end Friday levels. We remain above the 20-day EMA, while Friday lows were at 149.38. We have to get back above 152.60 to challenge recent highs. Such a move could draw fresh verbal FX jawboning, particularly if it isn't accompanied by a sharp rise in US-JP yield differentials. Fallout from Takaichi, who is set to become the new PM, is limited so far. Headlines from hawkish BoJ board member Takata are also providing some modest support this afternoon.

- Local focus is on digesting the formed coalition between the LDP and Ishin, which should deliver the PM position to LDP leader Takaichi. Takaichi is generally seen as a negative for the yen, local bonds (given her pro growth/monetary lose comments in the past), while being positive for equities. Still, earlier comments from Takaichi and her advisors indicated they didn't intend to excessively weaken the yen, which along with Takaichi odds of being PM being elevated at the end of last week, may be limiting yen fallout so far today.

- Ishin stated: "*YOSHIMURA: DON'T HAVE TIMELINE ON ZERO CONSUMPTION TAX ON FOOD" - BBG, so it may take a little time for fresh policies to emerge.

- BoJ's Takata stated that now is the time to adjust policy rates further and the inflation target is more or less achieved. Takata voted for a rate hike at the last policy meeting but this wasn't the majority viewpoint. At this stage, only 6bps with of hike risks are priced by the market for the end Oct meeting.

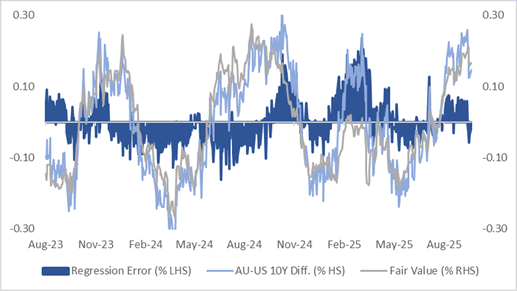

AUSSIE BONDS: Cheaper But Narrow Ranges On Data-Light Day

ACGBs (YM -5.0 & XM -5.5) are weaker after holding in tight ranges in today’s data-light session.

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at +13bps. At +13bps, the differential has narrowed from recent wides but remains in the top half of the ±30bps range that has prevailed since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is -2bps versus fair value.

- The bills strip is -3 to -6.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in November is given a 72% probability, with a cumulative 24bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The local data calendar is fairly quiet through the course of this week, with October's preliminary PMIs out on Friday, with the RBA's Bullock also speaking that day.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI