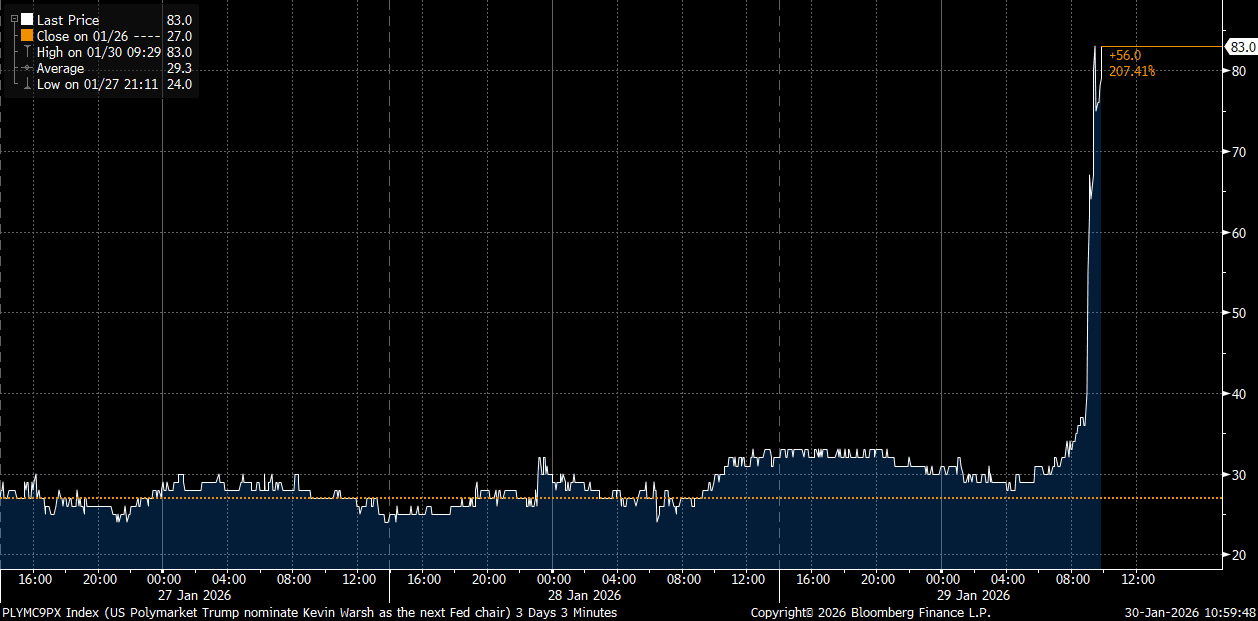

US: Warsh Fed Chair Odds Surge Per Polymarket, US Tsy Yields Firm

Follow the earlier headlines from US President Trump that the new Fed Chair would be announced Friday morning US time, we have seen a sharp push higher in odds for former Fed Governor Warsh to be announced for the position, per Polymarket. The chart below shows the intra day odds for Warsh, which have spiked this morning. Other finalists for the position in terms of Rick Rieder, Kevin Hassett and Christopher Waller have all got quite depressed odds at this stage. Rieder is under 10, the others close to flat.

- Via BBG Trump stated: “A lot of people think this is somebody that could’ve been there a few years ago,” Trump says, referring to the person he nominated." This may support the move for firmer odds for Warsh, given that he was considered for the Fed Chair position in Trump's first term as President.

- Also note; "Trump met 2day with his two finalists for Fed Reserve chair -- and is leaning toward KEVIN WARSH to replace Jerome Powell, I'm told. Nothing is official I'm told. But 1 source close to Trump says Warsh basically has the wink & the nod. KEVIN HASSETT is out. RICK RIEDER was also at the WH today & is the other finalist." via X Rachael Bade, a Washignton based journalist.

- Warsh at face value will likely be seen as a more hawkish choice, given his views on inflation etc. Trump is clearly pushing for easier policy settings.

- US Tsy yields are firmer by around 0.5-3.5bps across the curve in latest trade, with the back end leading. The 10yr at 4.26%, remains close to the mid-point of its recent 4.20-4.30% range. The USD is higher, up 0.30% for the BBDXY to 1181, with gains fairly uniform against the G10.

Fig 1: Warsh Fed Chair Odds Surge - Per Polymarket

Source: Polymarket/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PRECIOUS METALS: Profit Taking, Holidays & Exchange Measures Moving Prices

Gold was little changed on Tuesday while silver rallied again but didn’t regain all of Monday’s losses. The December FOMC minutes signalled that the Fed may want to watch and wait before easing further. Holiday-impacted thin trading volumes and profit taking into year-end are creating significant volatility especially for silver which is a materially smaller market.

- The December FOMC minutes showed that most members expect to cut rates further “if inflation declined” after the meeting’s decision to ease 25bp. However, a number of members thought it “would likely be appropriate to keep the target range unchanged for some time after a lowering of the range”.

- Both metals are flashing overbought but with around two US rate cuts priced in by end 2026, strong physical demand for silver and safe haven flows continuing driven by geopolitical, global trade and Fed independence uncertainties precious metals may stay strong next year. PBoC buying has supported bullion and its purchases are likely to continue.

- Gold is currently trading around $4342.0/oz and so far on Wednesday has been in a narrow range of $4329.4/4346.69. On Tuesday it rose 0.2% to $4350.3 to be up 2.4% in December and around 65% higher in 2025.

- Silver is correcting again during today’s APAC session after rising 5.8% on Tuesday to $76.295/oz following Monday’s 9.1% decline. The white metal is currently around $74.60 as it trends lower. It is up close to 170% this year.

- The CME decision to increase the cash held to back precious metals futures positions was a “normal review of market volatility”, according to DJ. Positions were liquidated on Monday where the cash wasn’t available to meet the new requirements and could still be impacting market moves. China has also taken measures to reduce speculation in silver.

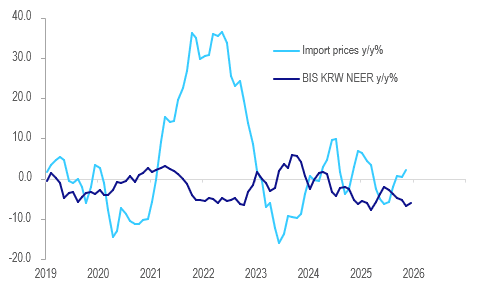

SOUTH KOREA: Inflation Remains Above BoK Target As Imported Inflation Rising

December CPI inflation printed in line with consensus with headline rising 0.3% m/m to 2.3% y/y down from November’s 2.4%. Core held at 2.0% y/y, around where it has been for most of 2025. 2025 headline inflation moderated 0.2pp to 2.1%, just above the Bank of Korea’s 2.0% goal. With inflation remaining above target and import price inflation creeping up while mortgage debt is growing due to rising house prices, the central bank is likely to leave rates at 2.5% for now, where they have been since May.

- The moderation in headline was driven by lower food inflation which moderated to 3.6% y/y from 4.7% in November, which should reassure the BoK given its concern over rising living costs. Transportation inflation remained elevated though at 3.2% y/y unchanged from October. Other categories were little changed except miscellaneous goods & services which may have been impacted by higher global gold & silver prices.

- The BIS KRW NEER is down 5.9% y/y in December after recording six consecutive monthly declines. The weaker currency is pushing imported inflation higher which rose 2.2% y/y in November up from 0.5%. It has risen each month since July, in line with the fall in the NEER.

- The next BoK decision is on 15 January.

South Korea import prices vs BIS KRW NEER y/y%

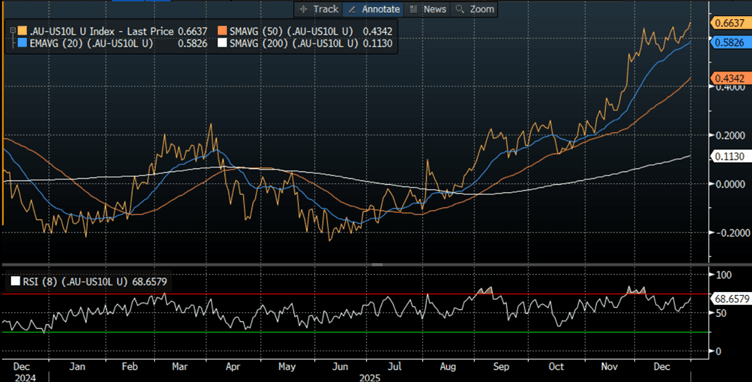

AUSSIE BONDS: Modestly Cheaper, AU-US 10Y Diff At Fresh High

ACGBs (YM -3.0 & XM -3.0) are modestly cheaper in today’s pre-holiday shortened session.

- Cash US tsys showed little reaction to the FOMC minutes release for the December meeting yesterday. The key paragraph from the December FOMC meeting minutes (link here) indicates (as did the meeting Dot Plot) a sizeable minority of members seeing no further easing through end-2026, but a base case among a solid if narrow majority that further limited cuts would ensue if the data cooperate.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at +65bps, a fresh cycle high.

- The bills strip is cheaper, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 108% by June and 163% by December 2026.

- By the end of January, Australians should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Bloomberg Finance LP