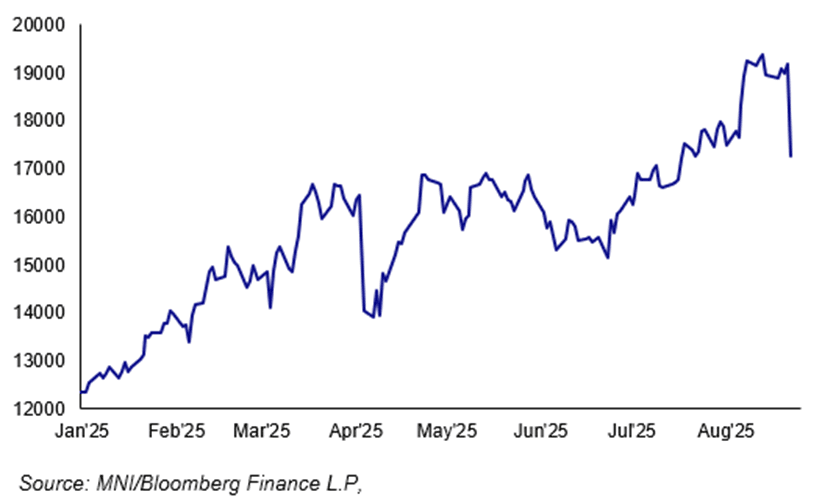

POLAND: Warsaw Banking Index Sinks Over 10% Following Bank-Tax Plan

Aug-22 15:25

- The Warsaw Banking Index has ended the session over 10% lower compared to Thursday’s close after the Finance Ministry announced a plan to increase corporate income taxes for lenders. The broad-based WIG Index ended the day around 4% lower. The proposal is seen reducing scope for dividends, and is expected to reduce the Polish financial industry’s appeal compared to its foreign peers.

- As a reminder, the Finance Ministry proposed to boost the corporate tax rate for banks to 30% next year, from the current 19%, and then lower it to 26% in 2027 and 23% in 2028. At the moment, it is unclear why this option was chosen over the previously proposed windfall tax, but it is part of broader fiscal consolidation efforts which will also include hikes to certain sin taxes and measures to improve tax collection.

Figure 1: Warsaw Stock Exchange Banking Index

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Early Equities Roundup: New Highs for SPX Eminis, Tech Stocks Stall

Jul-23 15:21

- Stocks are firmer early Wednesday, SPX eminis just off new all-time highs (6376.75), supported by a mix of Industrials, Health Care and Energy sector shares - risk sentiment buoyed after Pres Trump announced a sweeping trade deal with Japan late Tuesday.

- Currently, the DJIA trades up 185.94 points (0.42%) at 44688.76, S&P E-Minis up 13.75 points (0.22%) at 6360.75, Nasdaq up 18.5 points (0.1%) at 20908.89.

- Leading gainers in the first half buoyed by better than expected earnings: Lamb Weston Holdings +20.40%, GE Vernova +14.31%, Thermo Fisher Scientific +13.17%, Lennox International +9.69%, TE Connectivity +8.94%, Moderna +8.65%, Baker Hughes +7.96%, Vistra +6.85% and General Dynamics +6.31%.

- Technology sector shares primarily led decliners in the first half: Fiserv -17.68%, Enphase Energy -13.48%, Texas Instruments -12.40%, Microchip Technology -7.33%, ON Semiconductor -7.17% and Teledyne Technologies -5.13%. Other laggers outside of Tech included: Otis Worldwide -11.20%, NectEra Energy -4.40%, Albemarle -4.10 and Hasbro -4.04%

- Earnings expected after today's close: T-Mobile US, Mattel, Chipotle Mexican Grill, Molina Healthcare, CSX Corp, O'Reilly Automotive, Tesla, ServiceNow, Crown Castle, United Rentals, Rollins, QuantumScape, Alphabet, Alaska Air, Las Vegas Sands, Viking Therapeutics, IBM, and Valero Energy Corp.

FED: US TSY 17W AUCTION: NON-COMP BIDS $573 MLN FROM $65.000 BLN TOTAL

Jul-23 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $573 MLN FROM $65.000 BLN TOTAL

FOREX: Deutsche Bank Continue to Favour EURCAD Topside

Jul-23 14:46

- Deutsche Bank have noted that while at first glance, there seems to be a lot going right for Canada, a closer look takes a lot of the gloss away. This leaves them with a bearish near-term bias and continuing to favour EUR/CAD topside, which is up ~1.5% since recommending the position in their FX blueprint. They focus on the following fundamentals:

- The recent employment print was certainly strong, but it follows a string of weakness that still leaves Canada’s unemployment 2%pts above the trough – the worst in G10. Separately, both the Ivey PMI and BoC business survey suggest GDP growth could slip to zero.

- The BoC survey finds the uncertainty around tariffs is delaying capex plans and affecting corporate margins since passing on the cost is tough. Tariff uncertainty is also visible in the goods trade balance, which slumped to the largest deficit in decades and in net terms, portfolio flows have worked against CAD.

- The Carney government is indeed planning to spend more on defence and other capex. But it's targeting substantial cuts to operational spending (7.5%+ per year) to fund some of that. The fall budget will contain important detail.

- Overall, DB believe this points in the direction of further BoC easing and it's notable how little is priced (less than 25bps to the trough).