US COMMUNICATIONS: Warner Bros Discovery: Board Advises To Reject PSKY Offer

Key Points from Board’s Recommendation:

• Equity Backstop: The equity portion is supported by a revocable trust, not directly by the Ellison family.

• Regulatory Consideration: Board expects all proposed transactions to secure U.S. and foreign approvals; differences in regulatory risk are deemed immaterial.

• Incremental Costs: WBD shareholders would face an estimated $1.66/share in additional costs, including:

• $2.8B NFLX termination fee

• $1.5B financing costs from not completing the planned debt exchange

• Offer Flexibility: PSKY can amend or terminate its proposal at any time prior to closing; it is not a binding merger agreement

• Synergy Concerns: PSKY’s projected $9B synergies from combining Paramount/Skydance with WBD are viewed as operationally ambitious and potentially detrimental to Hollywood.

• The Board projects gross leverage of 6.8x under the PSKY deal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Nov17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2100(E1.4bln)

- GBP/USD: $1.3100(Gbp541mln)

- EUR/GBP: Gbp0.8830(E513mln)

- USD/JPY: Y155.00($1.1bln)

- USD/CAD: C$1.4000($510mln)

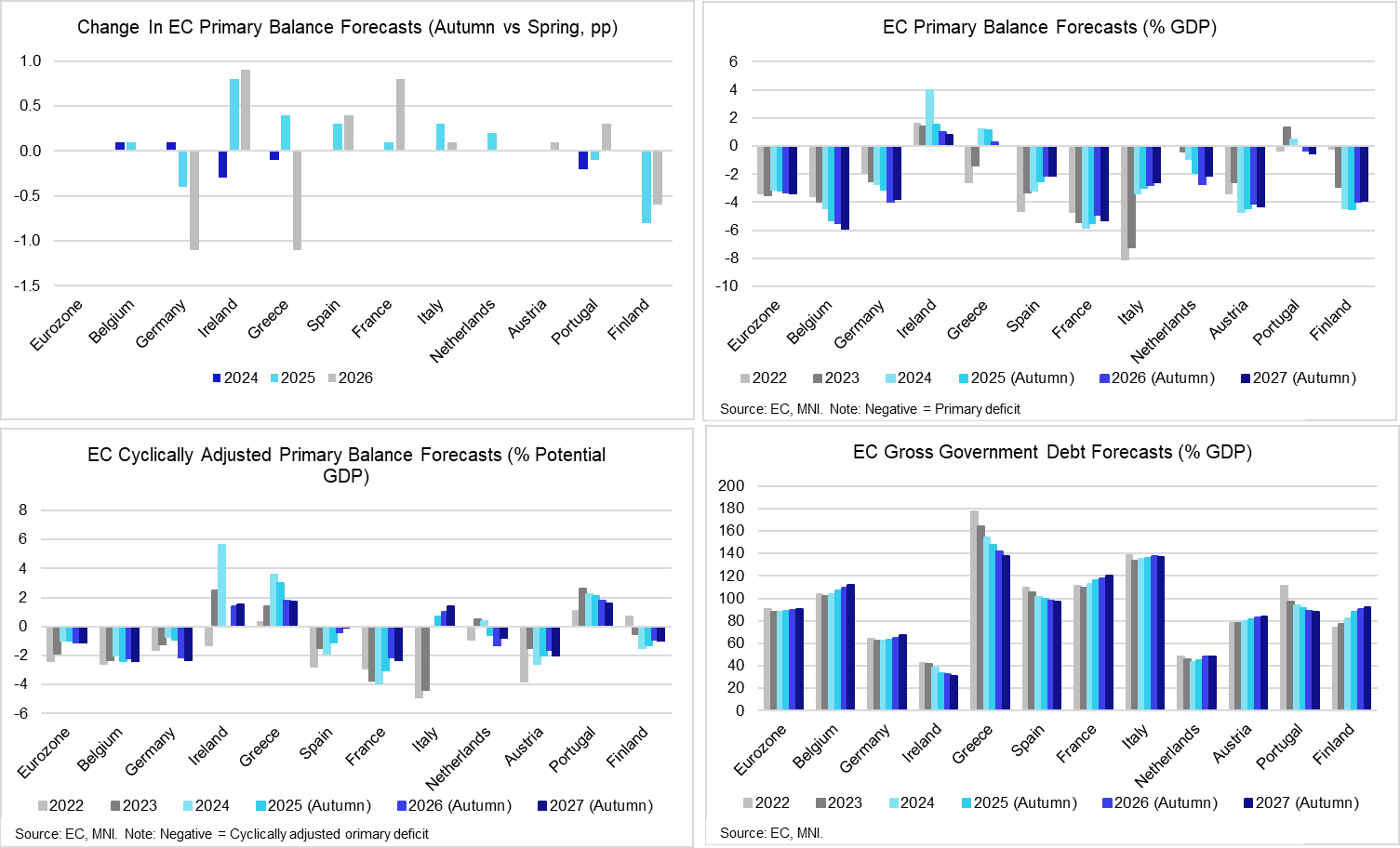

MACRO OUTLOOK: EC May Be Overoptimistic On German Fiscal Ramp-up

The EC’s Autumn projections are the first to account for the anticipated expansion of German fiscal spending. The EC projects the German budget deficit at 3.1% GDP in 2025, 4.0% in 2026 and 3.8% in 2027. In the Spring, the EC projected the 2025 German deficit at 2.7% and 2026 at 2.9%. On a cyclically adjusted primary basis (to better account for actual fiscal impulses), the EC projects a 1.2pp impulse (versus potential GDP) in 2026 and a 0.2pp impulse in 2027. The 2026 impulse is the joint largest across the largest 11 Eurozone countries.

- The 2025 deficit projection of 3.1% seems quite large, particularly with the 4Q rolling deficit at just 2.2% as of Q2 2025. Monthly federal fiscal data also hasn’t pointed to a substantial ramp up of fiscal easing yet. This data will be updated on Thursday, allowing us to better gauge current trends.

- Looking at the fiscal projections more broadly, cross-country trends highlight diverging outlooks between countries formerly classed as the “periphery” and other Eurozone peers. These trends have been reflected in market pricing across the last few years, through narrower XXX/Bund spreads.

- Between 2025-2027, debt/GDP is expected to fall in Ireland (-1.8pp), Greece (-9.6pp), Spain (-2.9pp) and Portugal (-3.1pp). Italian debt/GDP is expected to rise 0.8pp in the next two years, but this represents a 1.5pp rise in 2026 partially offset by a 0.7pp fall in 2027.

- For the Eurozone as a whole, primary balance projections are unchanged relative to the Spring. Bloc-wide debt/GDP is expected to hover around 90% through 2027.

- Full EC forecasts can be found here: https://economy-finance.ec.europa.eu/document/download/34538512-fff6-451a-8bbc-4c8d60e4d132_en?filename=ip327_en.pdf

OUTLOOK: Price Signal Summary - Corrective Cycle In Gilts

- In the FI space, a strong sell-off in Bund futures last week reinforces the current bearish condition and the contract is trading closer to its cycle lows. Price has pierced 128.52, the 76.4% retracement of the Sep 25 - Oct 17 bull leg. A clear break of this handle would signal scope for an extension towards 128.25, the Oct 7 low. Key short-term resistance is seen at 129.40, last Thursday’s high. Clearance of this hurdle would signal a reversal. First resistance is 128.80, the Nov 10 low.

- Gilt futures gapped sharply lower on Friday. For now, a move down is considered corrective and the next key support to watch lies at 91.82, the Sep 11 high and a former key breakout level. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. First resistance to watch is 92.85, the Nov 14 high. On the downside, a break of 91.82, the Sep 11 high, would strengthen a bear theme.