FED: Waller Sees All Sources Suggesting Labor Market Is Weak (2/2)

Waller on Bloomberg TV when questioned on the view that equities at all-time-highs and improved financing conditions can see renewed upside risk: "If all these loose financial conditions are going to cause a boom and excess in the US we should start seeing some of that in the labor market. We’re not seeing it. There’s so much speculation on AI that it’s kind of overshadowing everything else that’s going on. My job is unemployment and price stability. I think inflation will be ok, it’s going up but some of the tariff effects will come back off. But my job is about the labor market and it’s not good."

Q: Is there any inflation out there right now that you see that you’re concerned about?

- Waller: We have various ways to trying to tease out the tariff effects. Our estimate is that inflation is running at about 2.5% and we are not seeing anything that will explode. All this tension on AI is the ignoring the fact that other stuff is softening demand. That’s why I’m not really worried about the AI stuff. If it did really cause problems in energy, when thinking about future inflation just look at core and not headline.

Q: At the end of the month you might not get the labor market report. How difficult is it and can you even provide an outlook meeting-by-meeting in this environment?

- Waller: "I have this joke that for those who think we are too data dependent you are going to find out what non-data-dependent policy looks like. We do have lots of data, lots of labor market indicators that tell us the same story- the labor market is weak. We’re getting this conflicting data about GDP. The Beige Book came out and it was not like everything is rosy and booming. There could still be inventory pull-forward in the GDP numbers and we might see it start to pull off at the end of the year. On the tax bill, there was a lot incentives for business fixed investment but that implies equally for AI and non-AI. At the end of the day you’re still deciding on AI or non-AI investment and AI is winning, so I don’t know how much of a help that will be for non-AI sectors."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED FUNDS FUTURES: Buying In Front End

FFX5 paper paid 96.125 on ~4.7K. Comes after FFV5 saw paper pay 95.945 on ~6.7K.

GILT PAOF RESULTS: The PAOF for the 4.375% Jan-40 Gilt was not taken up

- GBP750mln have been on offer.

- This leaves GBP34.113bln of the gilt in issue.

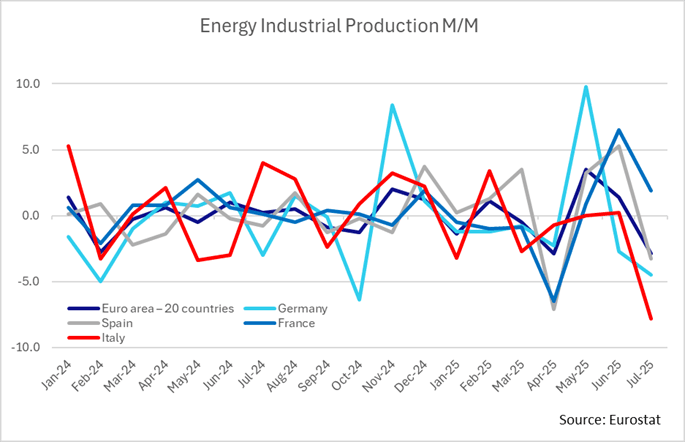

EUROZONE DATA: July IP Broadly In Line, Energy Volatility Mutes Strength

Euro area industrial production increased in July despite a return of a heavy drag from energy, with M/M readings on balance surprising positively but the Y/Y as expected. IP growth of 1.8% Y/Y is within some wide recent ranges owing in part to energy volatility.

- Euro area IP modestly undershot expectations in July with 0.3% M/M (cons 0.4) but that was easily more than offset by a large upward revision to -0.6% M/M in June (initially -1.3%).

- That was a ‘genuine’ upward revision with the Y/Y also lifted from 0.2% to 0.7%. Interestingly though, despite this upward revision the Y/Y in July was as expected at 1.8% (although note 27 replies for the M/M vs 12 for Y/Y in the Bloomberg survey).

- This 1.8% Y/Y is the only the highest since March, with the series oscillating between rates a little above 0% and below 4% in recent months.

- Broadly speaking, Germany and Italy’s growth (+1.5% and +0.4% M/M respectively) were partly offset by declines in France and Spain (-1.2% and -0.7% M/M respectively).

- Ireland’s usual volatility, which had driven previous M/M moves, calmed this month (+0.6% M/M vs -11.9% prior).

- Swings in energy IP have also had an increasingly large contribution to the headline number in recent months, with euro area energy IP contracting -2.9% M/M (vs +1.4% June). One ex-energy measure increased 0.8% M/M in July after -1.0% in June.

- Highlighting this volatility, Italy’s energy IP fell -7.8% M/M (vs +0.2% prior), Germany’s -4.5% M/M (vs -3.3% prior), and Spain’s -3.3% M/M (vs +5.3% prior). France saw an increase of +1.9% M/M (vs +6.5% prior).