FED: Waller Continues To Advocate Measured Easing Approach (1/2)

Fed Governor Waller (permanent voter, dove) continues to advocate for measured approach to easing monetary policy in an appearance on Bloomberg TV. Notable excerpts (partly paraphrased):

- When asked about whether his view has changed from his speech entitled "Let's Get On with It" from Aug 28: "In the last six weeks, I don’t think a lot has changed. All the private sector data, including the Beige Book yesterday, is telling us the same story. The labor market is weak but growth is on the stronger side, which is a puzzle now because you cannot have a strong growing economy and zero jobs growth. Either numbers start coming back down or the labor market rebounds."

- Q: Do you continue to reduce rates as you wait to see what is going on?

- "That’s exactly what I’ve been arguing. We don’t know which way this will break. If the labor market rebounds there’s less pressure for cutting rates, if growth comes back down there’s more pressure. You don’t want to make a mistake so the way to avoid that is to go cautiously or carefully. Do a 25bp cut and wait to see what happens and then get a better idea of what to do but if you’ve already started the process you’ve provided some initial support for the labor market that you feel is necessary."

His answers throughout the interview also broadly confirmed an appearance on CNBC on Friday, although with added mention of yesterday's Beige Book. On Friday, he unsurprisingly affirmed his view that the Fed should follow through with a series of cuts in light of developing labor market weakness (saying the labor market is "not tight in any way, shape or form"). While it's clear he's among the most dovish members on the Committee, eyeing 2 more rate cuts this year, he doesn't advocate too aggressive an easing: "I'm still in the belief we need to cut rates, but we need to kind of be cautious about it."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED FUNDS FUTURES: Buying In Front End

FFX5 paper paid 96.125 on ~4.7K. Comes after FFV5 saw paper pay 95.945 on ~6.7K.

GILT PAOF RESULTS: The PAOF for the 4.375% Jan-40 Gilt was not taken up

- GBP750mln have been on offer.

- This leaves GBP34.113bln of the gilt in issue.

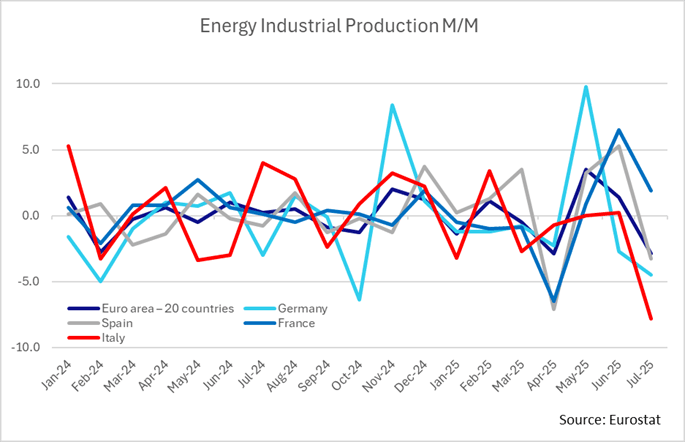

EUROZONE DATA: July IP Broadly In Line, Energy Volatility Mutes Strength

Euro area industrial production increased in July despite a return of a heavy drag from energy, with M/M readings on balance surprising positively but the Y/Y as expected. IP growth of 1.8% Y/Y is within some wide recent ranges owing in part to energy volatility.

- Euro area IP modestly undershot expectations in July with 0.3% M/M (cons 0.4) but that was easily more than offset by a large upward revision to -0.6% M/M in June (initially -1.3%).

- That was a ‘genuine’ upward revision with the Y/Y also lifted from 0.2% to 0.7%. Interestingly though, despite this upward revision the Y/Y in July was as expected at 1.8% (although note 27 replies for the M/M vs 12 for Y/Y in the Bloomberg survey).

- This 1.8% Y/Y is the only the highest since March, with the series oscillating between rates a little above 0% and below 4% in recent months.

- Broadly speaking, Germany and Italy’s growth (+1.5% and +0.4% M/M respectively) were partly offset by declines in France and Spain (-1.2% and -0.7% M/M respectively).

- Ireland’s usual volatility, which had driven previous M/M moves, calmed this month (+0.6% M/M vs -11.9% prior).

- Swings in energy IP have also had an increasingly large contribution to the headline number in recent months, with euro area energy IP contracting -2.9% M/M (vs +1.4% June). One ex-energy measure increased 0.8% M/M in July after -1.0% in June.

- Highlighting this volatility, Italy’s energy IP fell -7.8% M/M (vs +0.2% prior), Germany’s -4.5% M/M (vs -3.3% prior), and Spain’s -3.3% M/M (vs +5.3% prior). France saw an increase of +1.9% M/M (vs +6.5% prior).