AUSTRALIA DATA: Wages Stabilise But Private Sector Rises Moderating

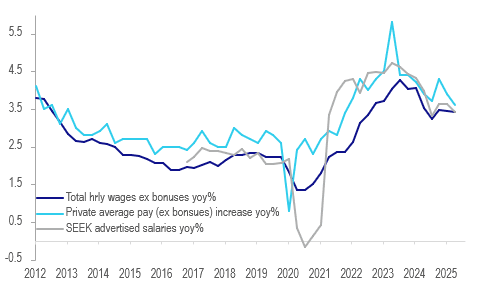

Q3 wages rose 0.8% q/q to be 3.4% higher on a year ago, in line with Q2 and Bloomberg consensus, signalling a stabilisation consistent with SEEK advertised salary data. In November, the RBA forecast 3.4% y/y for Q4 2025 before moderating to 3% by end 2026. Thus, the Q3 WPI data don’t change the outlook for monetary policy with rates likely on hold towards at least mid-2026 as it monitors price and capacity pressures.

Australia wages ex bonuses y/y%

Source: MNI - Market News/SEEK/ABS

- Private sector wage inflation moderated to 3.2% y/y (+0.7% q/q) from 3.4% in Q2 and 3.5% in Q3 2024. This is the slowest rate since Q2 2022. Private wages peaked in Q4 2023 at 4.2% and have been trending lower since.

- The proportion of private sector jobs receiving a pay increase in Q3 has been fairly stable since the end of the pandemic but the size of the rise is trending down due to the moderation in minimum/award wage increases. On July 1 they rose 3.5% down from 3.75% in 2024 and 5.75% in 2023. In Q3 2025, the share of jobs with a rise was 47% after 49% in Q3 2024 with the average increase at 3.6% down from 3.9% in Q3 2024.

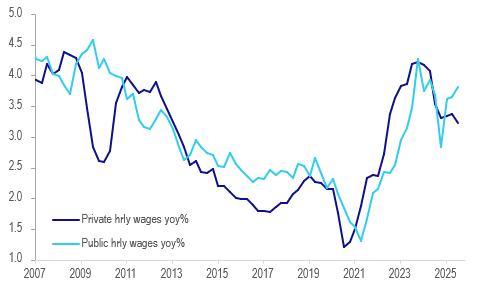

- Public sector pay also began to moderate in 2024 but has turned higher over this year. In Q3 it rose 0.9% q/q & 3.8% y/y up from 3.6% in Q2 and 3.7% in Q2 2024, the highest since Q2 2024.

- In Q3, 33% of public jobs received a pay rise (Q3 2024 30%) with the average increase at 3.1% up from Q3 2024’s 3.0%.

- The share of jobs receiving large wage gains is also moderating with 24% obtaining a rise above 4% down from 31% in Q3 2024.

Australia private vs public sector wages y/y%

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US-CHINA: Soybeans, Rare Earths Key Focus Points For US-China Talks

Headlines from US President Trump, speaking to reporters on Air Force One, crossed a short while ago. On US-China trade, Trump stated that he believes China will make a deal on Soybean purchases and that he would like to see purchases, at least, return to levels that they were at prior. Trump also stated he does not China to play rare earth games with the US (these headlines came via Rtrs).

- This is likely to set the tone for US-China talks this week, with US Treasury Secretary Scott Bessent and China Vice Premier He Lifeng will meet this week (in Malaysia) ahead of the two Presidents meeting. Soy bean purchases and rare earths will be key focus points from the US side.

- Trump added in remarks this morning, that tariff rates on China can be lowered but China has to do things for the US as well.

- This comes after Trump's Friday remarks, which helped broader risk appetite stabilize, that a 100% tariff rate on China (on top of existing tariff rates) was not sustainable.

- Other remarks by Trump stated that India would continue to pay high tariff rates if it did not restrict oil imports from Russia.

- He added tariff rates for Colombia would be announced later on Monday (US time). This follows the escalation in tensions between the two countries, as the US attempts to curb drug inflows.

LNG: European Gas Range Trading Ahead Of Winter Risks

European gas fell 1.4% to EUR 31.93 on Friday, close to the intraday low of EUR 31.78 after the high at EUR 32.37, driven by news of the prospect of a Trump-Putin meeting that may take place in Hungary. Ahead of winter and with little progress towards peace in Ukraine, prices have been within a narrow EUR 3 range this month.

- President Trump was unwilling to provide Ukraine with Tomahawk missiles due to escalation worries as well as concerns over keeping the US arsenal stocked. He also warned again that Ukraine will need to give up territory in exchange for peace.

- Ukraine hit an important southern Russian gas processing facility on the weekend which resulted in it stopping inbound flows.

- With the onset of the heating season, European inventory building has stalled at just under 83% full. With ongoing Russian attacks on Ukrainian power infrastructure, it is likely to increase its gas imports substantially which impacts the rest of Europe’s access to supplies.

- US natural gas has trended lower since 8 October but after reaching $2.893 on Friday it recovered somewhat to be up 2.1% to the key $3.00 level driven by forecasts for cooler weather towards month end. Prices are down over 9% in October.

- The January Henry Hub contract is at $4.14 almost a $1 higher than where November currently is.

- US lower-48 gas production rose 3.8% y/y on Friday but demand fell 6.8% y/y, according to BNEF data. Flows to LNG export terminals rose 2.3% w/w.

- China’s LNG imports fell 47.7% y/y in September while pipeline flows rose 2.8% y/y. China is receiving more piped Russian gas.

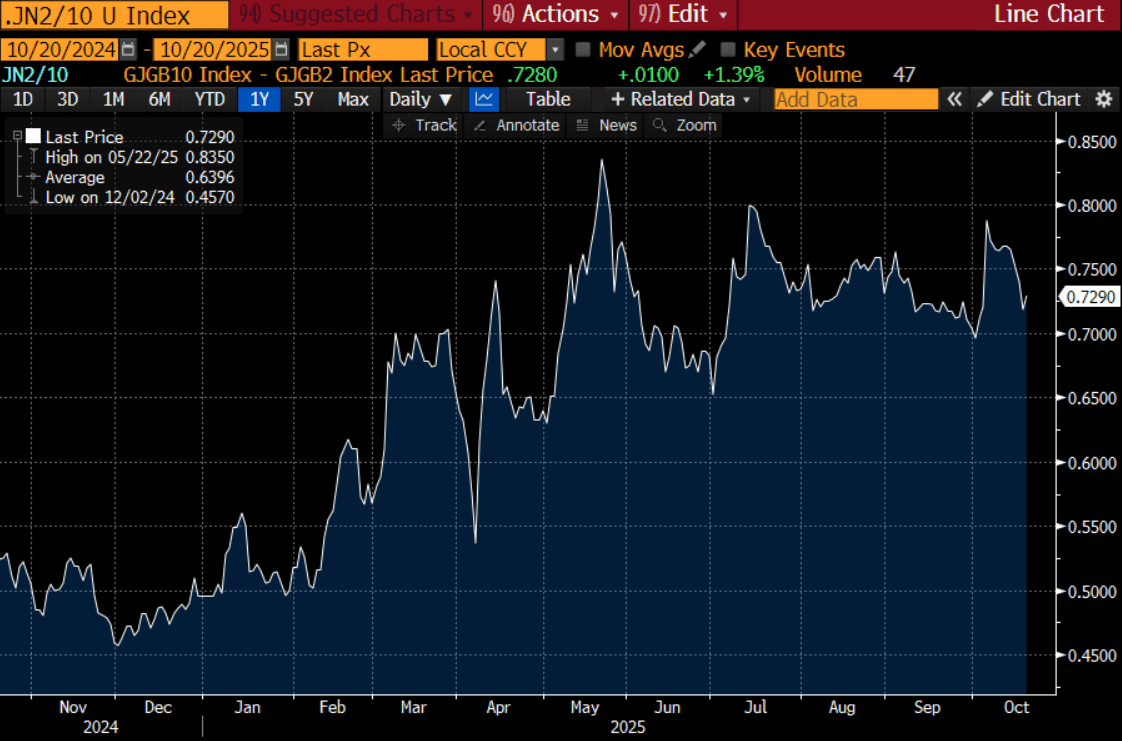

JGBS: 10Y Leads The Modest Cheapening

In Tokyo morning trade, JGB futures are weaker, -34 compared to settlement levels, and near session lows.

- Locally, the odds of Takaichi becoming the next PM sit back near 100. The Ishin party and the LDP are reportedly in the final stages of discussions around an alliance (with something potentially announced today). Such a backdrop leaves the rest of the minor parties unable to field enough votes for an alternative PM candidate. Focus will then turn to the policy outlook.

- Also note we have a speech from BoJ board member Takata at 12:50pm local time. Takata was a hawkish dissenter at the last policy meeting.

- Cash US tsys are little changed in today’s Asia-Pac session after Friday’s modest sell-off.

- Cash JGBs are weaker across benchmarks, with the 10-year leading. The benchmark 10-year yield is 2.1bps higher at 1.653%, with the 2/10 curve at 73bps. (see chart)

- Bloomberg survey of market forecasts suggests the curve will remain unchanged by the end of Q4.

- Swap rates are flat to 1bp higher.

Bloomberg Finance LP